Month: April 2022

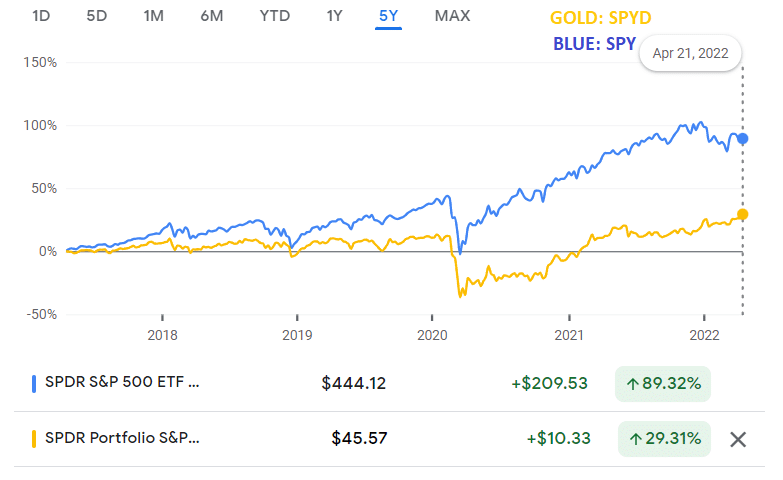

SPY vs SPYG vs SPYD vs SPYV: Head-To-Head ETF Comparison

How to Calculate Your Roth IRA and 401k Paychecks

Saving for retirement is a big deal. Every one of us needs some way to survive when we age out of the workforce and retire. Some lucky few can start successful ventures and save more money than they can ever spend, but most of us need to be a little slower and more deliberate with it.

We rely on a 401(k), an IRA, or multiple accounts to fund retirement. The trouble is, it’s pretty challenging to determine just how much you’ll have to live on when you retire. There are many moving parts and different factors to consider.

Moreover, if you search online, much of what you’ll find is about saving for retirement, not how to calculate what you’ll have as a payout when you finally retire.

How can you estimate what your retirement paychecks will be?

Let’s get started.

Age of Retirement

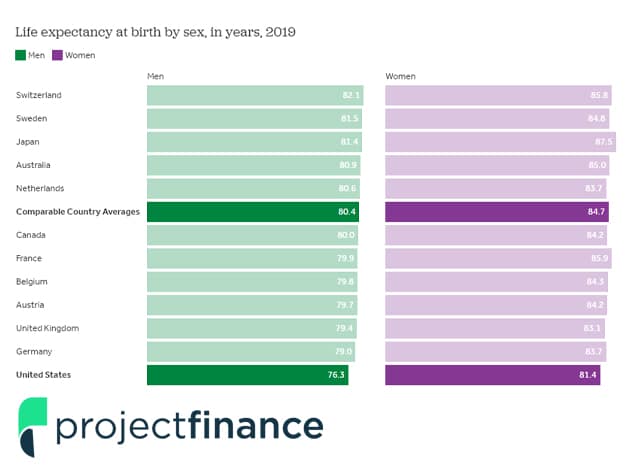

The average retirement age varies by location, culture, and income level. The one commonality is the age of 60. With an average life expectancy of about 78 in America today, this gives you a solid two decades to enjoy the twilight of your life. Of course, some people don’t retire until 65 or even 70.

The commonality is the age of required disbursements from investments.

Both IRAs and 401(k)s allow you to start taking payments from them when you hit a certain age.

That age, as of current laws, is 59 ½.

Why the half-year, and not just 59 or 60? Who knows!

There’s probably a reason buried in the depths of time, but if there is, it’s not easy to find.

Additionally, those accounts require you to start taking payments at age 72.

On top of that, some people qualify for early disbursements, starting at age 55. Specifically, if you leave your job once you turn 55, you may be able to take payments from that job’s 401(k) plan without penalty. Like a 401(k) you own or an IRA, other accounts do not allow this exception.

The age of retirement makes a big difference in your payment calculation. The longer you want to live off your investments, the longer those investments need to last. Ideally, you will have enough principal stashed away to live solely on interest payments, but that’s not always possible. More on that later.

The other reason age of retirement matters is market volatility. The longer you want to live on your retirement funds, the more likely you’ll have to cope with a downturn. Investment accounts take advantage of the fact that, over decades, the markets always rise. In the short term, however, volatility can affect interest rates and monetary value, and significant market volatility can have a significant impact, like a global pandemic affecting the world markets.

Additional Investments and Payments

An IRA and a 401(k) are not the only possible investments you can have for your retirement; they’re just two of the most common.

When calculating your eventual retirement paycheck, remember to consider additional income streams.

Two, in particular, are relatively common.

The first is a pension.

A 401(k) is technically a form of pension, but a “traditional” pension operates a little differently. These tend to be most common in major companies and government organizations, and they’re slowly growing less common over time.

If you have one, you will likely have a fixed payment from a company pension, though you may have the option to cash it out or roll it over to another account so the company doesn’t need to deal with it anymore.

The second is Social Security. Throughout your life and your career, you pay taxes. Some of those taxes go to the government to spend as they will, some go to state governments, etc. Some of it, however, goes towards the Social Security fund. Everyone who works in America pays into Social Security, and everyone who worked in America long enough to earn enough credits is entitled to Social Security when they retire.

Social Security payments typically begin at age 62 and are usually calculated to be roughly 40% of your income level when working. Alternatively, you can delay taking your payments until age 70 to increase the amount you get each year.

Keep these two sources of retirement income in mind. Calculating your desired total retirement income requires considering all of your income streams, not just those from your primary accounts.

401(k) vs. IRA

In the title, we mention 401(k)s and IRAs as the two investment vehicles we will calculate.

Is there any significant difference between them in retirement?

The answer is not really.

There are a lot of differences between IRAs and 401(k)s, but they’re all relevant to investing in them, not taking money from them. Once you reach retirement age, taking money from either of them – or even rolling them together – is acceptable. Either way, you have a principal invested in the markets, which earns interest based on its investment package. You take money from it as required once you retire. How much? Well, that’s the question.

Roth vs. Traditional

One concern is whether your 401(k) or IRA is a Roth account or a traditional account.

This decision has tax implications which can be relevant to calculating your paycheck in retirement.

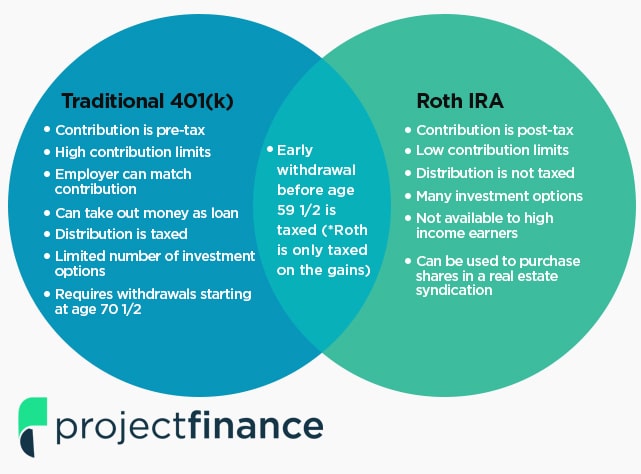

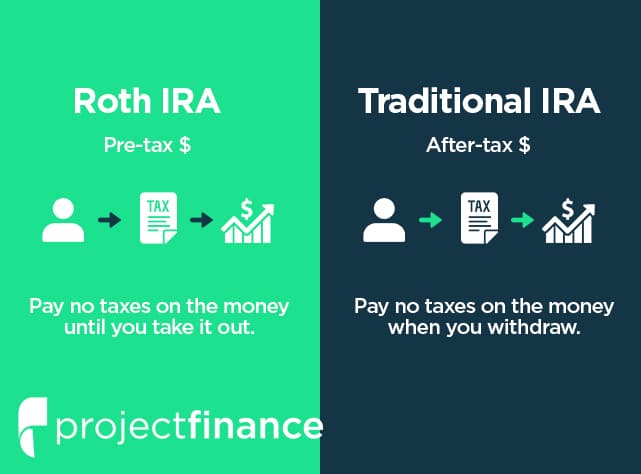

With a traditional account, the money contributed to the account is tax-free. When you file your taxes annually, you count the money you put into your investments as a deduction, effectively reducing your overall income and allowing you to invest that money without paying taxes.

The government always gets its due. When you retire and start withdrawing money from a traditional IRA or 401(k), that money you pull is a paycheck and is taxed as income. You may have to pay income tax on that paycheck, calculated based on your income tax bracket with that new income in retirement. The amount of taxes you’ll have to pay depends on your retirement account type and varies from state to state.

Roth accounts work in the exact opposite way. With a Roth account, the money you contribute comes from your money after paying income taxes on your contributions and is not considered a deduction on your taxes when you earn that money and invest it. However, since you already paid taxes on that money, you don’t have to pay taxes on the disbursements you take when you retire.

There are ways to roll a traditional account into a Roth account, but they get into more complicated tax strategies that we’re not going to discuss today. If you have a traditional IRA or 401(k), you have to consider income taxes as an additional drain on your retirement paycheck, whereas if you have Roth accounts, you do not.

There’s one other vital factor to consider: the required minimum withdrawal from your accounts. You must take a distribution every year with a traditional retirement account once you hit age 72. With a Roth, you don’t need to take any money out of it. The only requirement is that when you die, your dependents or beneficiary of your inheritance must take the distribution.

How Payouts Work

Once you reach a certain age, you can begin taking distributions from your retirement accounts. Once you reach an even later age, you will be required to do so. As mentioned above, the earliest age you can take money out of a retirement account without penalty is 55 in specific circumstances, or 59 and a half for most people. Once you hit 72, you’ll be required to take payments.

Note: This can change. The age used to be 70 and a half, but it was changed in 2019 under the Setting Every Community Up for Retirement Enhancement (SECURE) Act. It’s possible that, if you’re not already at retirement age, that age can change by the time you reach it. All of these numbers are subject to change based on the whims of the government.

The amount you must take out of your account each year is called the RMD, or Required Minimum Distribution. You can, at any time, take more out of your accounts if you wish, though this is usually a bad idea if it’s not strictly necessary, so we’ll discuss it more in a moment.

To quote the IRS:

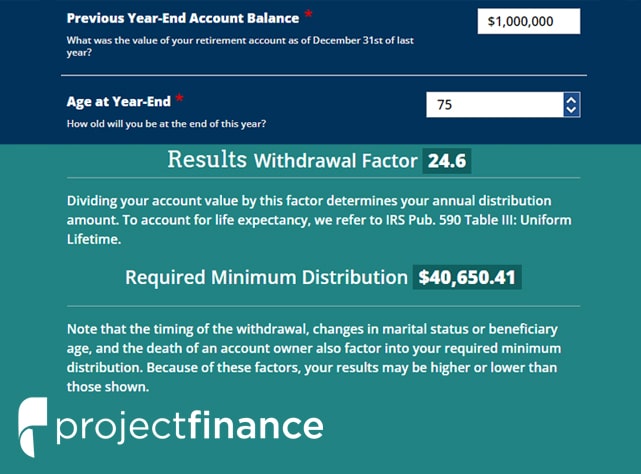

“The required minimum distribution for any year is the account balance as of the end of the immediately preceding calendar year divided by a distribution period from the IRS’s ‘Uniform Lifetime Table.'”

If you thought that table would be simple, here’s the IRS page for it. This page is over 38,000 words long, so settle in for some serious reading.

Luckily, you can use a simple calculator to estimate how much you will need to take out. The IRS provides one here. For example, if your retirement account has one million dollars in it when you turn 75, you must withdraw $40,650.41 from the account that year. These funds work out to be a monthly income from your account of $3,387.53, though it will be subject to whatever the income tax rate will be when you retire.

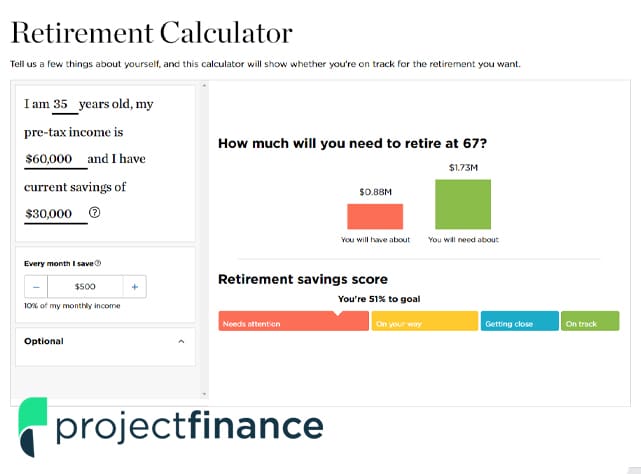

Assuming you have a flat one million in your retirement account is excellent for simple math calculations, but it’s unrealistic. To calculate how much you’ll have in your account at any given age, you will want to use a retirement calculator like this one. By filling in information about your contributions and your investment vehicles, you can estimate how much you’ll be getting paid in your retirement.

The truth is, the amount you earn in retirement will vary by too many factors to offer a simple answer.

You can also always withdraw more than the minimum to maintain a standard of living you’re comfortable with.

The Dangers of Drawing on Principal

Before we wrap up, one thing to mention is the difference between principal and interest in a retirement account.

The goal of every good retirement plan is to have enough money set aside to live entirely off the interest it provides or near enough as it makes no difference. A sufficiently large investment, placed in a series of investments with high rates of return, will earn enough money each year to cover the minimum disbursement plus any extra you want to withdraw.

If you tap into the principal of the investment, however, your overall total investment value declines.

That gives you less leeway for future payments, but it makes the amount you earn from interest even lower. If you don’t take a lower amount of distribution to compensate, you can enter a cycle of ever-decreasing funds until you, eventually, run out of money.

It’s impossible to say with certainty the threshold for this. You may notice that we’ve given very few numbers throughout this post.

That’s because everyone’s situation will be different. It will vary depending on factors like:

- Your life expectancy

- Where your money is invested and what the rate of return is

- Market performance, which is impossible to predict, especially decades into the future

- Chances to the tax and legal code that may make the situation better or worse for you

- Your cost of living and how much money you will need to maintain your standard of living

- Any medical conditions that will require ongoing treatment and the expenses associated with it

There are too many factors to consider. You can use calculators to estimate the minimum required distribution, but it’s an estimate. You can never know for sure until you’re actually at the moment of taking the money, at which point it’s too late to plan.

It’s always best to start investing as early as possible and invest as much as possible as soon as possible. The more you have in your investments, and the longer they have to grow, the less likely you will need to worry about it when you retire.

FAQ: How Much Cash Should Retirees Keep on Hand?

Saving is something many of us do throughout our careers. These savings are often divided between long-term and liquid investments, the latter of which can help pay for immediate expenses.

General financial advice is to have 3-6 months’ worth of expenses tucked away in savings. The more liquid these funds are, the easier they can be withdrawn for emergencies. These funds can be used to pay for immediate needs, such as vehicles and sudden medical expenses. Alternatively, you can use these funds to cover the ongoing costs of living in the event of a loss of income, giving you leeway to find a new job.

Does this advice still hold once you reach retirement age? Probably not.

- In retirement, your income drops and stabilizes; you begin to get payouts from your retirement accounts, social security, and similar sources.

- More importantly, in retirement you no longer have penalties for withdrawing money from your retirement accounts beyond the loss of principal for the still-accumulating growth.

Meanwhile, other expenses can start to ramp up. Medical bills grow more common and more significant as we get older and our bodies wear.

Is having a 3–6-month emergency fund still relevant in this period of our lives? Should you have more cash on hand or less when you can pull from your retirement accounts as needed?

What Does Cash Mean?

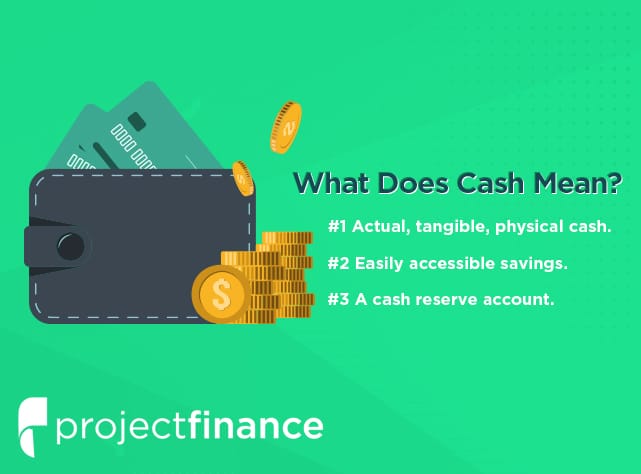

Before we dig too deep, let’s take a moment to discuss what “in cash” means. As a retiree, you want to have money accessible when you need it.

Three forms of “cash” get tossed around interchangeably, but they have slightly different implications.

- The first is actual physical cash. Most of the time, no one is advocating keeping cold, hard cash on hand. You may want some physical cash for everyday expenses, particularly if you travel to places where businesses may less commonly accept cards, but that’s pretty minimal these days. Keeping physical cash around was more of a habit for those who lived through the Great Depression, where investments bottomed out. Today, hoarding physical cash can even be risky; plenty of vendors no longer accept cash, preferring to handle everything digitally.

- The second is easily accessible savings. A savings account can have money pulled from it whenever you like and is often tied to a debit card for immediate purchasing power. This definition of cash is what most often what people talk about when they mention cash; it’s liquid, not tucked away in an account which you can only access indirectly, and it’s not there to linger and earn interest.

- The third is a cash reserve account. Cash reserve investments are generally tied to a currency’s value. These accounts can have interest rates ranging from near-nothing (keeping your dollar value 1:1 with the value of a dollar) or rising in times of economic hardship. Federal reserve rates have sometimes been as high as 5%, offering modest growth while the money is still reasonably accessible.

For today’s post, we’re looking primarily at #2, though #1 also qualifies. The idea is to draw a line between investments that earn interest and cash on hand. You can spend these funds immediately on anything from living expenses, medical bills, and leisure purchases.

Do You Still Need an Emergency Fund?

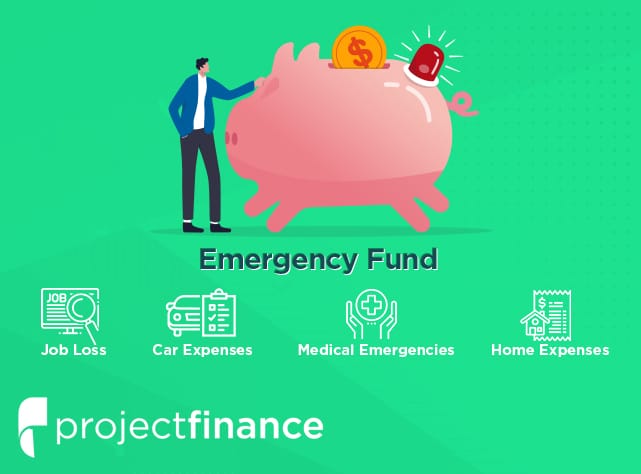

The point of an emergency fund is two-fold.

- First, it serves as insulation against hardship. If you lose your income or have a sudden considerable expense, you need to cover it without defaulting on other payments or letting unfortunate events cascade. Losing a job can quickly shift into losing a vehicle or housing if you don’t have funds to keep paying those bills while you search for new income.

- The other purpose of an emergency fund is to have money on hand that you can tap into without touching your long-term investments. Before retirement age, if you want to tap into your assets, you can take out a loan against them (and kick the financial hardship can down the road until you have to repay it), or take an early withdrawal and pay a penalty fee for doing so.

Once you reach retirement age, though, do you still need that protection? You don’t need to take a loan against your retirement accounts; you can pull money from them with no penalty. Does it not, then, serve as an emergency fund itself?

Yes. You still want to avoid pulling from your long-term investments for a straightforward reason: growth.

You know by now that the point of long-term investing is to build up as much money as possible in your portfolio so that interest can compound. The more money you have, the more interest makes that money grow. The more interest makes money grow, the more money you have. It feeds back on itself.

When you pull money from your long-term investments, you lose that compounding growth. When you’re pulling out your income in retirement, the idea is for your investment to remain stable for as long as possible; you only pull from interest, so your core investment stays the same, and thus the interest stays the same.

The trouble happens in two ways.

- Firstly: tapping into the principal reduces the core amount of money that is earning interest. This reduces the amount of interest, further reducing your regular income. Tapping into your principal can start a dangerous loop, forcing you to reduce your investments until you eventually drain your account.

- Secondly: what happens if an economic downturn hits, as it did in 2008, or temporarily in 2020 due to Covid? Interest rates and growth plummeted during these periods. However, you need to keep paying your bills and cost of living. If you’re relying on your investments to pay your way, you have to tap into your principal. If you keep cash around, on the other hand, you can use these funds instead and ride out the financial hardship without worrying about making your investment position worse.

How Much Cash Should You Keep On Hand?

It’s impossible to give general numbers as to how much cash you should keep on hand in retirement. It all comes down to an examination of your expenses. Someone living in a home they own in a rural area in Tennessee will have significantly different costs from someone living in the Bay Area in a rented unit.

To calculate how much cash you should keep on hand, you first need to have a solid idea of your monthly expenses. Maybe you’re spending $3,000 per month on typical living expenses. Perhaps that number is closer to $10,000 for other people. Keep in mind that this number is likely to rise over time. The cost of living keeps going up in 2022, and everything from energy to food to medical care is most likely going to grow more costly.

The second thing you need to know is what other sources of income you may have. Even though you’re retired, you may have additional income streams.

Income can come in a few forms:

- If you’ve worked a career that has accrued a pension, that pension will pay out once you retire, with a fixed amount each year. Pensions are less common than they used to be, but they aren’t entirely gone quite yet.

- Social Security. As a government-managed and public program, social security is a basic income for anyone of retirement age. Some people don’t qualify for social security income – exceptions include a variety of relatively narrow categories of people – but it still provides a consistent, if low, income for most retirees. There’s some doubt whether social security will still be available in a few more decades, but if you’re retiring now, you should have it.

- Supplementary income. Many retirees pick up hobbies they can monetize (for example, selling handicrafts online) or pick up a part-time job to have both preoccupation and income. You should count this income as well.

Now that you know how much it costs to live and how much you’re pulling in from various non-investment sources of income, what category do you fall in?

- Under-covered. This scenario is by far the most common position. Your expenses are higher than your income. These expenses are paid with disbursements from your investments.

- Your income and expenses balance out, so you can leave your investments alone.

- Over-covered. You make more than enough from your non-investment sources; you don’t need to worry about running out of money right away.

Generally, it would help to calculate your necessary cash on hand based on the discrepancy between income and expenses.

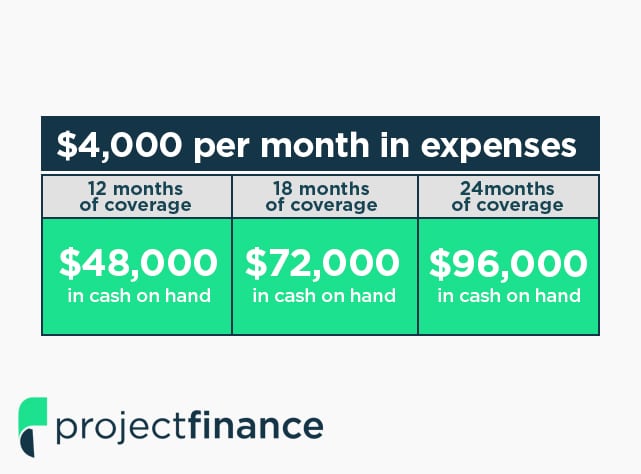

For example, suppose that your costs of living sum up to $7,500 per month. Your income covers a little under half of your expenses, leaving $4,000 per month to come from somewhere else, typically your investments.

Let’s say you have $2,000 per month in a pension, $1,000 per month in social security, and $500 per month in part-time income.

To calculate your emergency fund, decide how many months you want to be covered. Pre-retirement, the general recommendation is 6-12 months. In retirement, opinions differ. Some financial advisors say 12-18 months, while others say 24+ months.

Consider this: the larger your cash on hand, the more insulated you will be from economic hardship by adjusting your investments. The markets can take between 6 and 18 months (or sometimes longer) to recover from a downturn, so you want at least that much set aside to pay expenses to avoid tapping into your investments which you’d be selling for a low value.

Moreover, different investment portfolios may take more or less time to recover. An investment made of half stocks and half bonds, for example, can take up to 40 months to fully recover from a downturn.

In our example, with $4,000 per month in expenses not covered by a stable income, you would want:

- Twelve months of coverage, or $48,000 in cash on hand.

- Eighteen months of coverage, or $72,000 in cash on hand.

- Twenty-four months of coverage, or $96,000 in cash on hand.

So, somewhere between $50,000 and $100,000 is the right number in this hypothetical scenario. Your numbers will vary quite a bit depending on your unique living situation.

Just because you retired doesn’t mean you want to cash out all of your investments. Long-term investments can continue to grow as long as you have the luxury to let them. You never know how long you’re going to live after retirement or what unexpected expenses mar arise.

You want your investments to stay as large and as stable as possible for as long as possible and only tap into them in the case of an unavoidable emergency.

Remember, as well, that you may have other sources of funds in an emergency. You may be able to leverage a home equity line of credit, the funds in a Health Savings Account, or other credit lines if you need them before tapping into your retirement accounts.

Using Your Best Judgment

No one can predict what the markets will do. Over the long run, historically, they’ve gone up. Once you hit retirement age, you can no longer rely on long-term recovery from short-term downturns. To avoid financial hardship, it would help if you found the right balance of income and savings from various sources to insulate yourself from downturns.

Everyone’s financial situation is unique. The best you can do is create a plan based on what you know and make the best judgment about your future. It may be worth talking to a financial advisor directly, considering all of the unique factors in your life.

Are you close to retiring, or have you already retired? What is your primary intention for wanting to keep cash on hand? Do you have any questions for us on maintaining your retirement funds and maintaining an emergency cushion that you can access quickly? Please share with us in the comments section, and we’ll get back to you with a thoughtful answer to point you in the right direction!

Can You Contribute to Multiple 401(k) Accounts Simultaneously?

The humble 401(k) is among the most popular forms of retirement account. It is typically employer-sponsored and often includes employer matching (to a point), allowing retirement funds to ramp up faster than other investment vehicles simply due to the additional influx of cash.

“Before 1974, a few U.S. employers had been giving their staff the option of receiving cash in lieu of an employer-paid contribution to their tax-qualified retirement plan accounts. The U.S. Congress banned new plans of this type in 1974, pending further study. After that study was completed, Congress reauthorized such plans, provided they satisfied certain special requirements. Congress did this by enacting Internal Revenue Code Section 401(k) as part of the Revenue Act. This occurred on November 6, 1978.” – Wikipedia.

Though this form of retirement plan didn’t become popular until the 80s, it is now one of the most common plans available due to its benefits for employers and employees. Most companies that offer retirement benefits do so through a 401(k) plan today.

In the past, careers were stable. You could get a job and reasonably expect to work for that company for decades and possibly keep that same career to your retirement. Retirement parties were a common sight.

Today, company loyalty is at an all-time low, with many people job-hopping every 2-3 years. Companies often fail to provide avenues for advancement or raises, even to counteract the cost of living, so changing companies is often seen as the only way to progress in a career.

There are a ton of repercussions to this shift in employment culture, but one that many people overlook is the retirement plan. If you’re hired on to a company that offers a 401(k), and you work for them for three years, great! You have three years of contributions to your retirement account.

What happens if you leave the company and go to another that also offers a 401(k) plan? Chances are they’re with various brokerages or use different asset distributions. They open a new 401(k) for you, but your old one still exists.

Can you have two 401(k) plans legally? Can you contribute to both of them? Are there any salient details you should know?

Let’s dig in and find out.

Are There Legal Restrictions on Multiple 401(k)s?

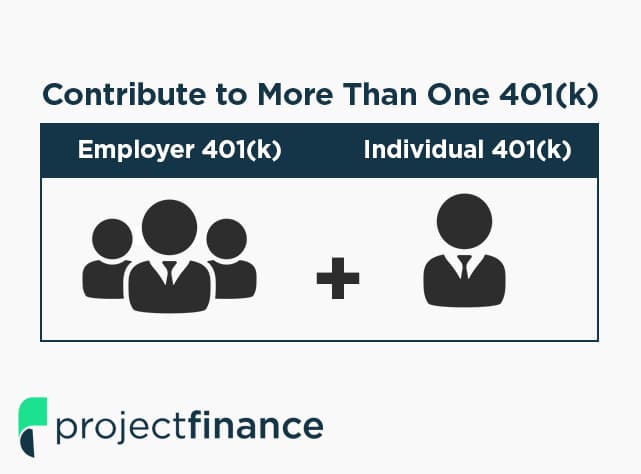

First of all, there’s no legal restriction against having multiple 401(k) accounts. You can have multiple 401(k) accounts from W-2 employers, or you can have both an employer-sponsored 401(k) and an individual 401(k) as suits your needs.

It’s pretty typical for people to have more than one 401(k). There are no laws or regulations against it. If you change jobs, you can keep your old 401(k), roll it over into your new account, consolidate it, or even take a payout.

However, there is one restriction: your old 401(k) needs to have at least $5,000 in it to maintain it. If it has less than that amount of money, the employer is entitled to shuffle that money around, often rolling it into an IRA. If your old 401(k) has less than $1,000, they will cash it out and send you a check.

The other limitation is that you cannot contribute to an old 401(k) from an employer you no longer work with. You can’t tell your new employer to contribute to your old account, nor can you contribute to it; after all, your old employer has no real incentive to help you with your retirement; they’re not allowed to do anything with those funds other than continue to manage them.

How to Contribute to More Than One 401(k)

So, wait. If you can’t contribute to an old employer’s 401(k), how can you contribute to more than one 401(k)? There are two options.

The first is having an employer 401(k) and an individual 401(k).

Individual 401(k)s are only available to people who have their own companies or are self-employed. Individuals with self-employment income and people who have C corps, S corps, or LLCs and no employees can create their 401(k) plans.

The individual 401(k) is unique in that the contribution limits are higher because you can “match” your contributions as both the employee and the business owner; you can “match” your contributions. This strategy isn’t “free” money the way an actual employer match is – since you’re contributing both sides, rather than one side coming from a company – but it effectively allows you to have a much higher contribution limit than a standard 401(k).

The second option is to have more than one job.

If you work two jobs, and both of them offer 401(k) plans to their employees, you are free to have both. In some cases, this can be a good idea because it allows you to access different asset mixes and funds and accrue more employer matching above the contribution limits.

What are The 401(k) Contribution Limits?

There are two relevant 401(k) contribution limits you need to know.

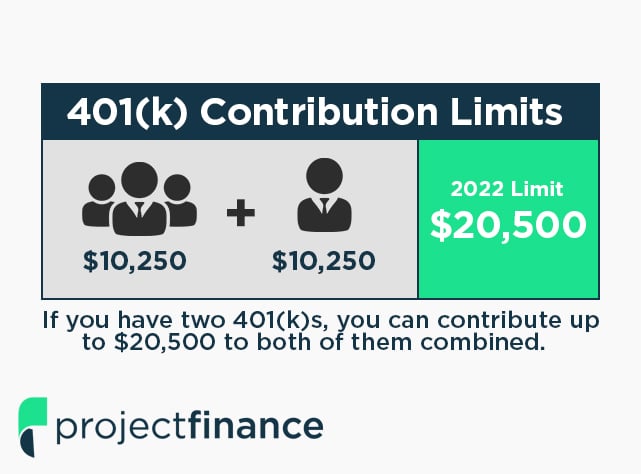

The first is the individual contribution limit. This contribution limit is a limitation that applies to all 401(k)s. In 2022, that limit is $20,500.

A 50/50 split means each 401(k) would support up to $10,250 and not a penny more. So, if you have one 401(k), you can contribute up to $20,500 to it. If you have two 401(k)s, you can contribute up to $20,500 to all accounts combined.

The distribution can vary. If you want to put $20,000 in one 401(k) and $500 in the other, you can do so. It would be best if you simply made sure neither employer over-funds your accounts through automatic contributions. If you over-contribute, you may be subject to additional taxes on the excess, and you’ll be required to remove the extra contributions, paying the 10% early withdrawal penalty. In general, over-contributing is penalized and isn’t worth trying to do.

There’s a second contribution limit, though, and it’s the most exciting. It’s the employer contribution limit. This limit, as of 2022, is $61,000.

There’s one quirk, however. This limitation is calculated per employer rather than per employee.

In other words, both of your employers can potentially contribute up to $61,000 to your 401(k)s. If you work two jobs and have two employers, and all three of you max out your contributions, that’s $20,500 + $61,000 + $61,000.

Employer contributions are usually based on a percentage of the employee’s salary and contributions, carefully calculated to be as minimal as possible while still compelling to the employee. Very few companies will max out contributions for most of their employees. However, that’s a more social and political discussion than a legal one.

If you’re using an individual 401(k) as a self-employed person with a day job, you can contribute to both the employer and employee side of your individual 401(k).

Imagine a scenario such as this:

- You work a W-2 job with 401(k) matching, dollar for dollar, up to your contribution limit.

- You have a lucrative LLC on the side.

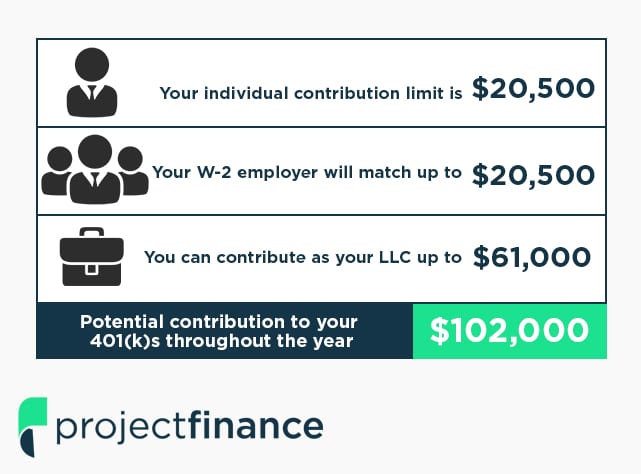

You have three relevant values here:

- You can contribute as your LLC by up to $61,000.

- Your individual contribution limit is $20,500.

- Your W-2 employer will match up to $20,500.

That means you can potentially have $102,000 added to your 401(k)s throughout the year.

If your W-2 employer wanted, they could even contribute more, up to that $61,000 amount, though it’s relatively unlikely to happen.

This practice is perfectly legal; you simply need the funds to supply the account from your LLC.

Remember, too: if you’re over 49 years old, you can add “catch-up contributions” on top of your other contributions; the limits are higher for older people to better take advantage of a limited number of years of compounding interest.

Before we continue, there’s one more quirk you should be aware of: employee vesting. When you sign up for a retirement plan with an employer, they will usually have a clause about “vesting” in the employer contributions.

Vesting is partial ownership of the money the employer invests in your account. If an employer has, say, 20% per year vesting, it will take five years for you to be entitled to the total amount the employer has contributed.

This contribution limit is essentially a way for an employer to avoid paying into an employee’s account, only to have that employee leave after 1-2 years and take the money with them. While most of the time, this wouldn’t be valuable to do anyway, some specific businesses and industries have excellent retirement benefits. Thus, vesting rules prevent it. It would be beneficial to do so.

In practice, what this means is that if you leave an employer before you are fully vested in their 401(k) contributions, they can keep some percentage of the money – the percentage you weren’t invested in. This limitation can be a rude awakening if you roll over an old 401(k), only to find that some portion of the value doesn’t come with you.

What to Do with Multiple 401(k)s

Suppose you find yourself in a situation where you have more than one 401(k). What should you do? What’s the correct move financially?

The truth is, there’s no one correct answer. Your best bet is to talk to a financial advisor directly. However, we can offer some general advice and scenarios.

If you left a job with a 401(k) and you started a new career with a 401(k), you generally want to do something with the old 401(k). There are several reasons for this.

- If the value is too low, under $1,000, the employer will cash out the old 401(k) in your name, and you will be subject to a penalty for early withdrawal.

- If your old 401(k) value is under $5,000, the employer is not required to keep a handle on it and can force you to roll it over or otherwise claim it.

- Since IRAs and 401(k)s are different accounts, they are subject to additional rules, asset mixes, and management practices. If you leave the retirement account alone, your employer will likely roll it over into an IRA for you to manage on your own. After all, the employer doesn’t want to manage your money when you no longer work for them.

- If the old employer goes bankrupt or collapses, it can be challenging to track down and claim the money in the old account, especially years after the fact. Of course, you’re entitled to it, but getting ahold of it can be challenging and frustrating.

Generally, the best option is to roll over your old 401(k) into your new one, so your interest keeps compounding. There are occasionally good reasons to leave your old 401(k) in place, such as taking advantage of limited investment vehicles. Again, though, talk to a financial advisor about your specific situation.

Remember that you can’t contribute to a 401(k) managed by an employer you no longer work for. While they may be required to keep managing the money if it’s over $5,000, they are not required to allow you to pay into the account.

On the other hand, if you have two 401(k)s because you’re self-employed, you can use the contributions from the employer site to invest more than you “should” be able to invest. Careful management of employer matching with your W-2 job, plus maximizing your contributions as an LLC, can be a compelling way to save more for retirement.

Summing Up

To sum things up in brief:

- Yes, you can have more than one 401(k) account.

- Yes, you can contribute to more than one 401(k) account if you actively work for two employers (even if one of those employers is yourself).

- Your individual contribution limit is shared across all 401(k) accounts, and you will be subject to taxes and penalties if you over-contribute.

Depending on your specific situation, there are a few potential benefits to having more than one 401(k). Still, you would do best to talk to a financial advisor directly about your particular circumstances to get the best advice.

Do you have multiple 401k accounts, or are you thinking of opening one? Are you worried about hitting contribution limits? Have you had trouble rolling over your 401ks, or are you worried you’re doing something incorrectly? Please share with us in the comments below, and we’ll do our best to point you in the right direction!