Month: November 2021

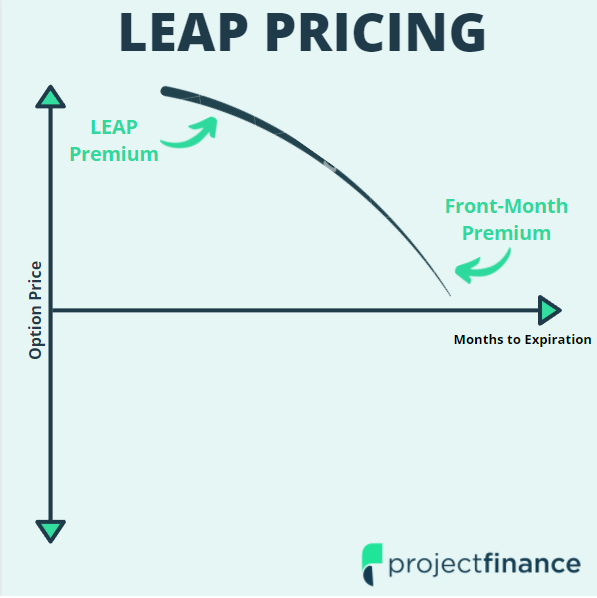

Long-Term Equity Anticipation Securities (LEAPS) Explained

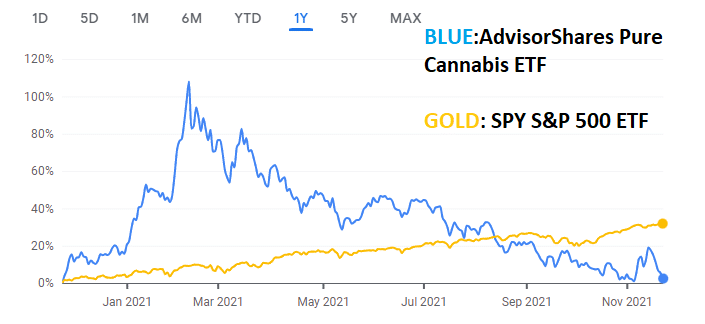

PSDN: AdvisorShares Poseidon Cannabis ETF Explained

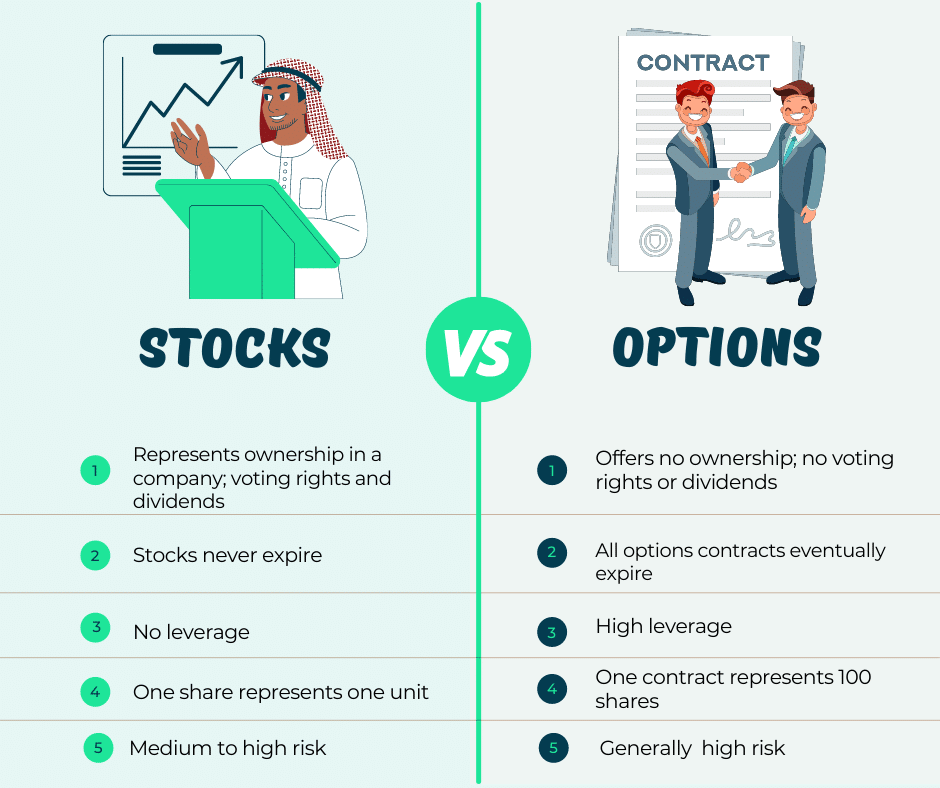

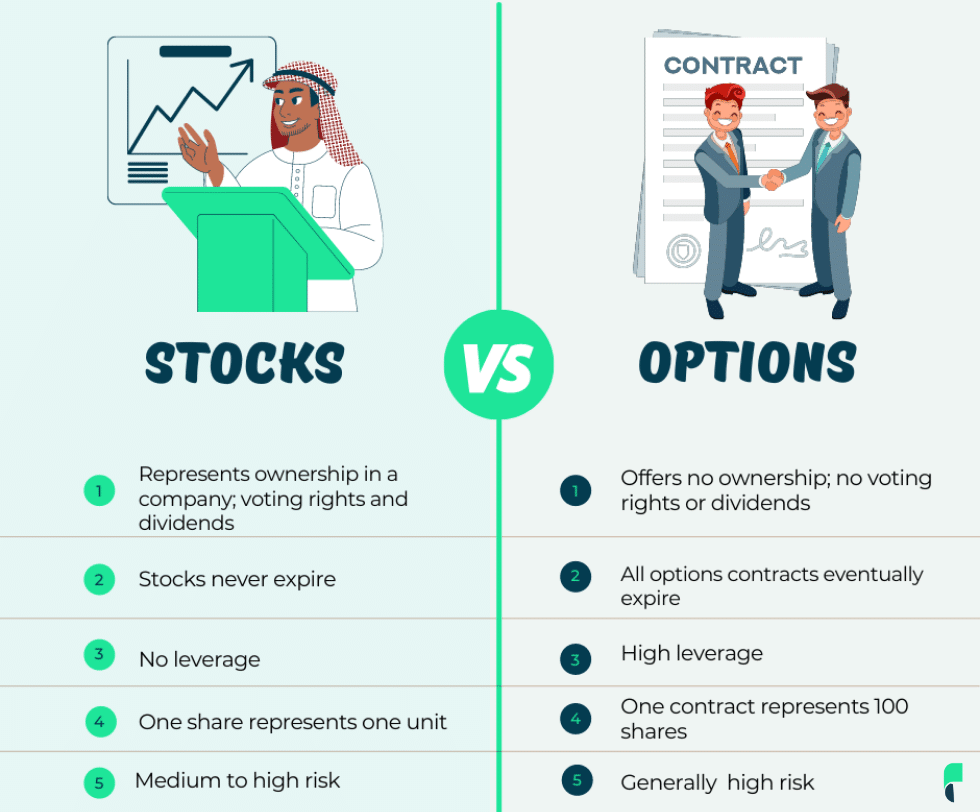

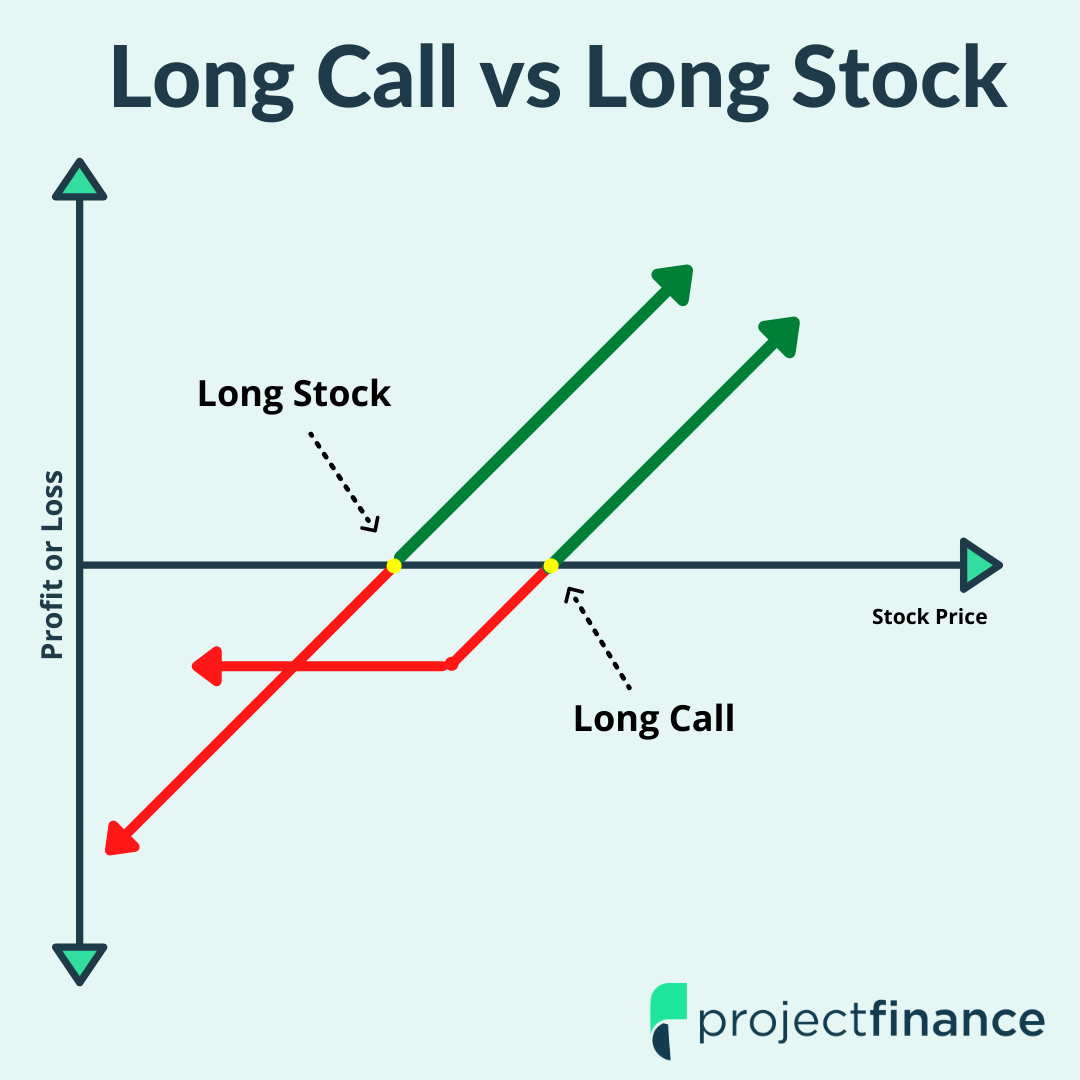

5 Ways Stocks Differ From Options

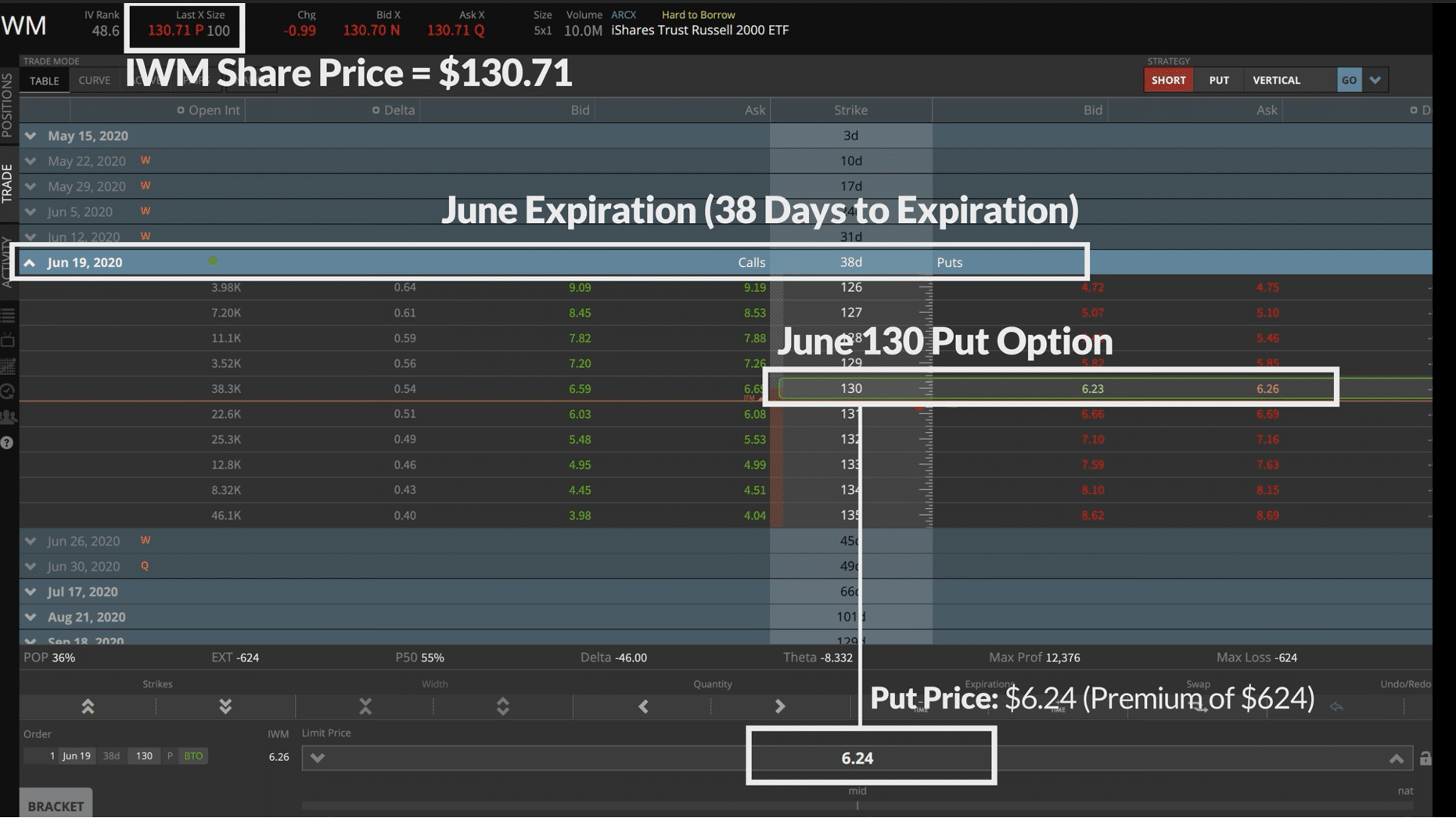

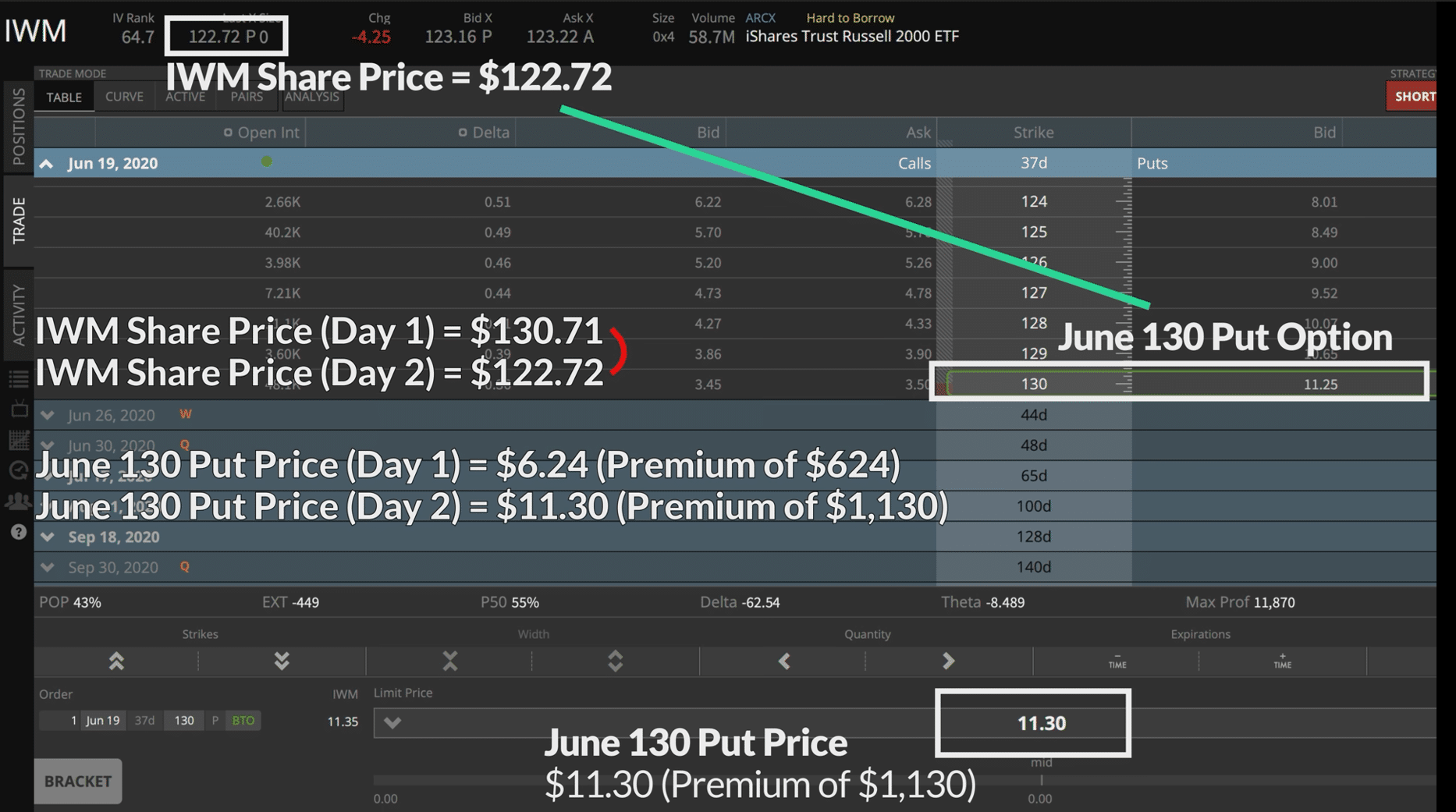

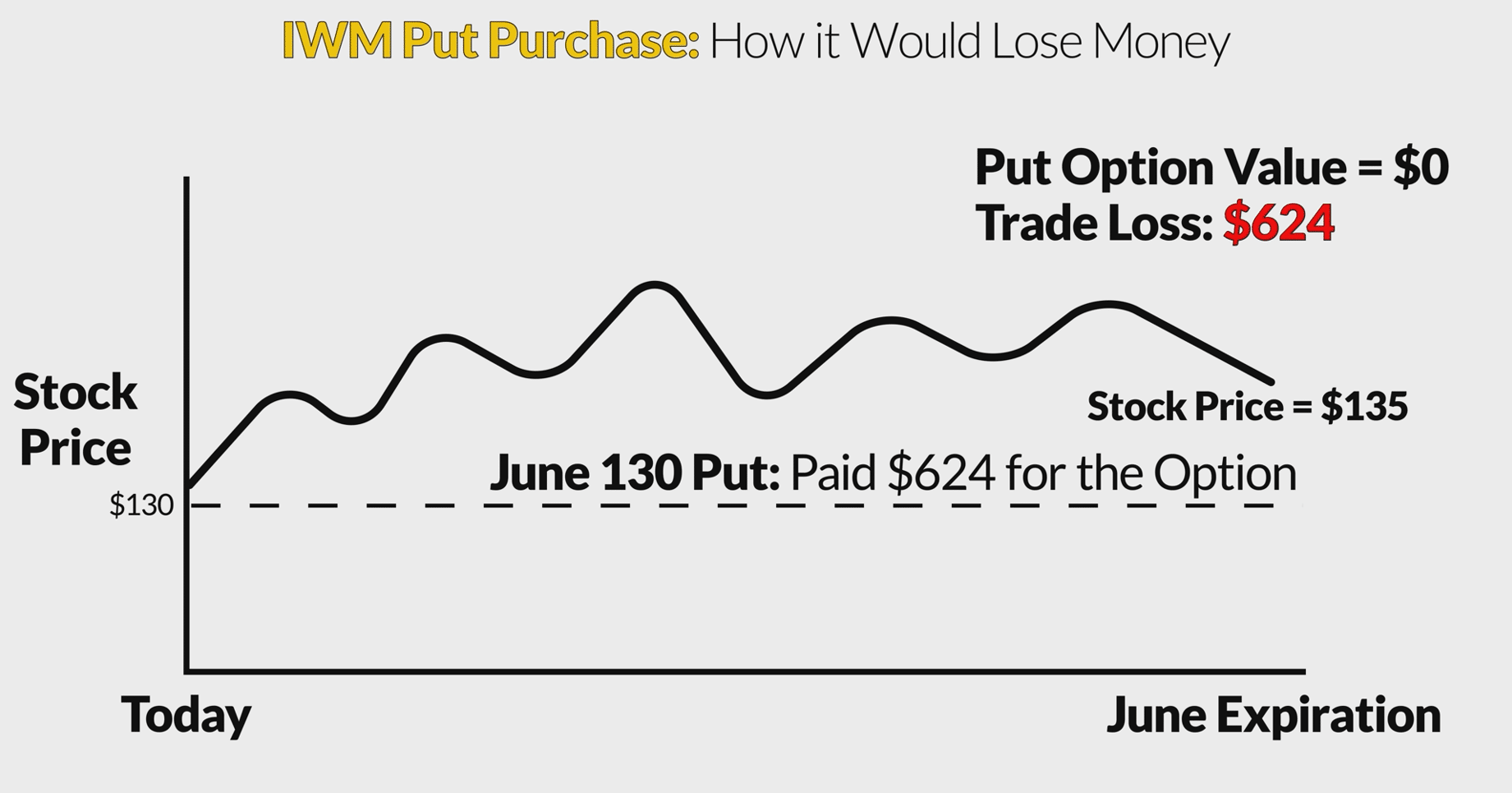

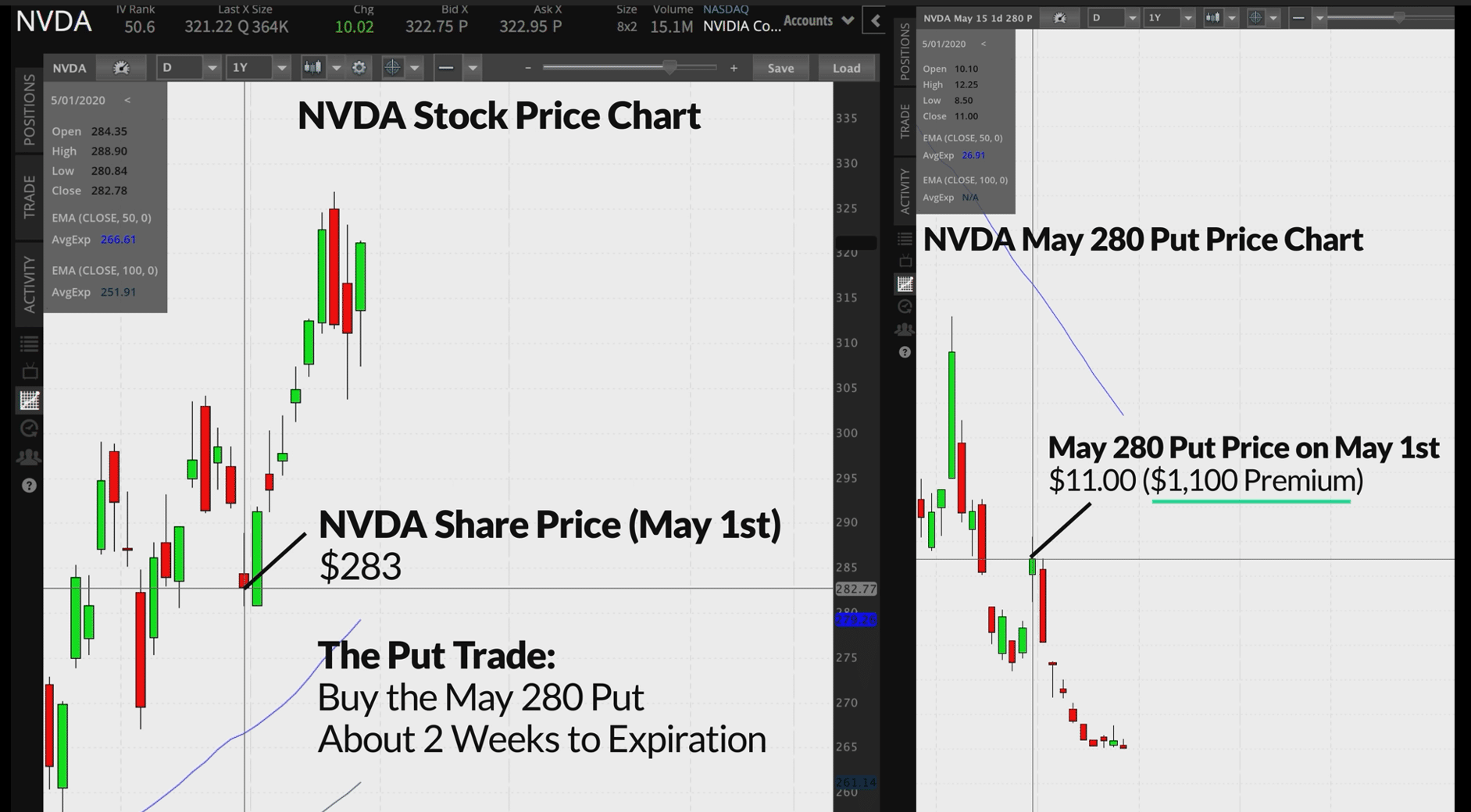

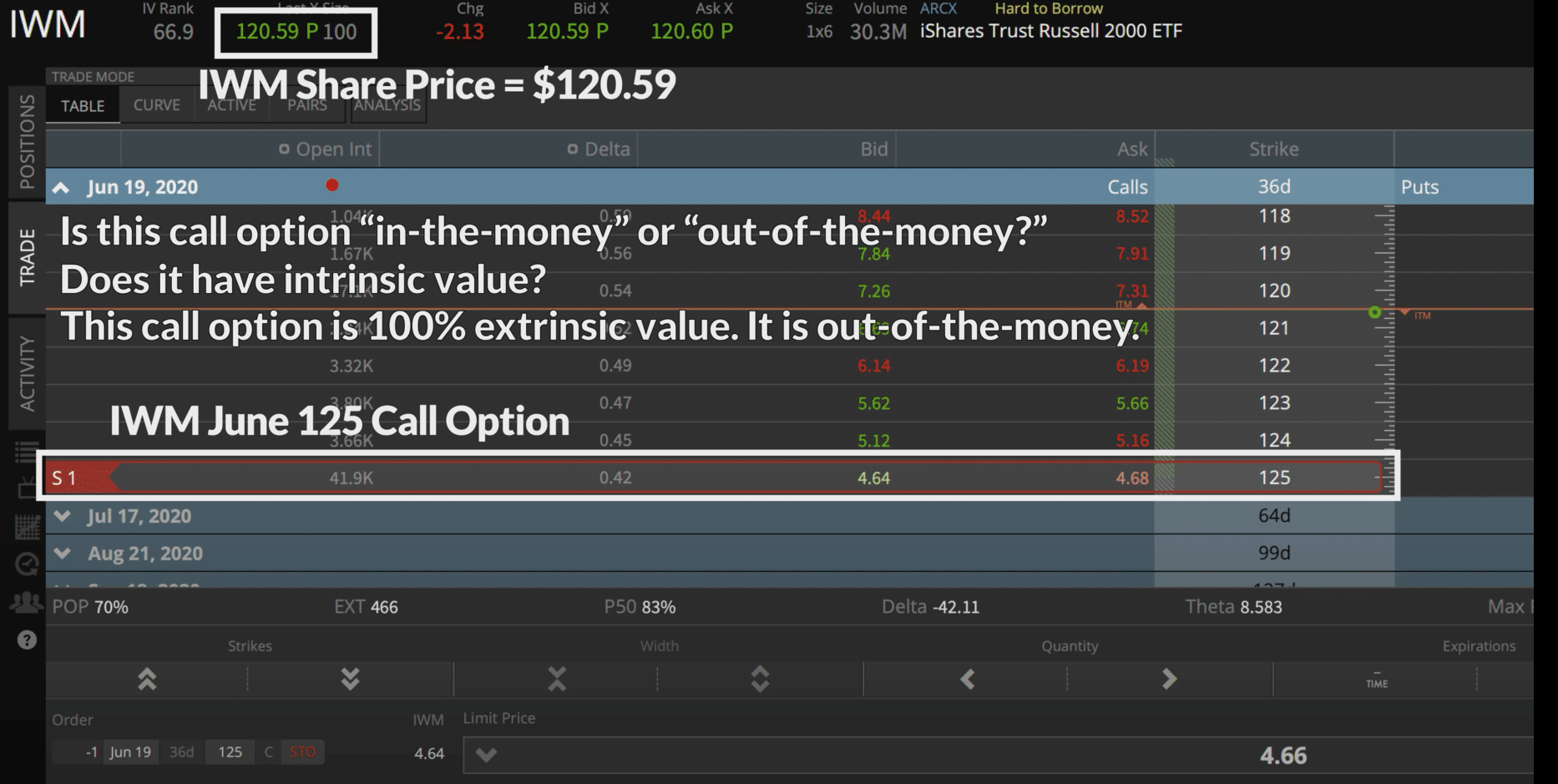

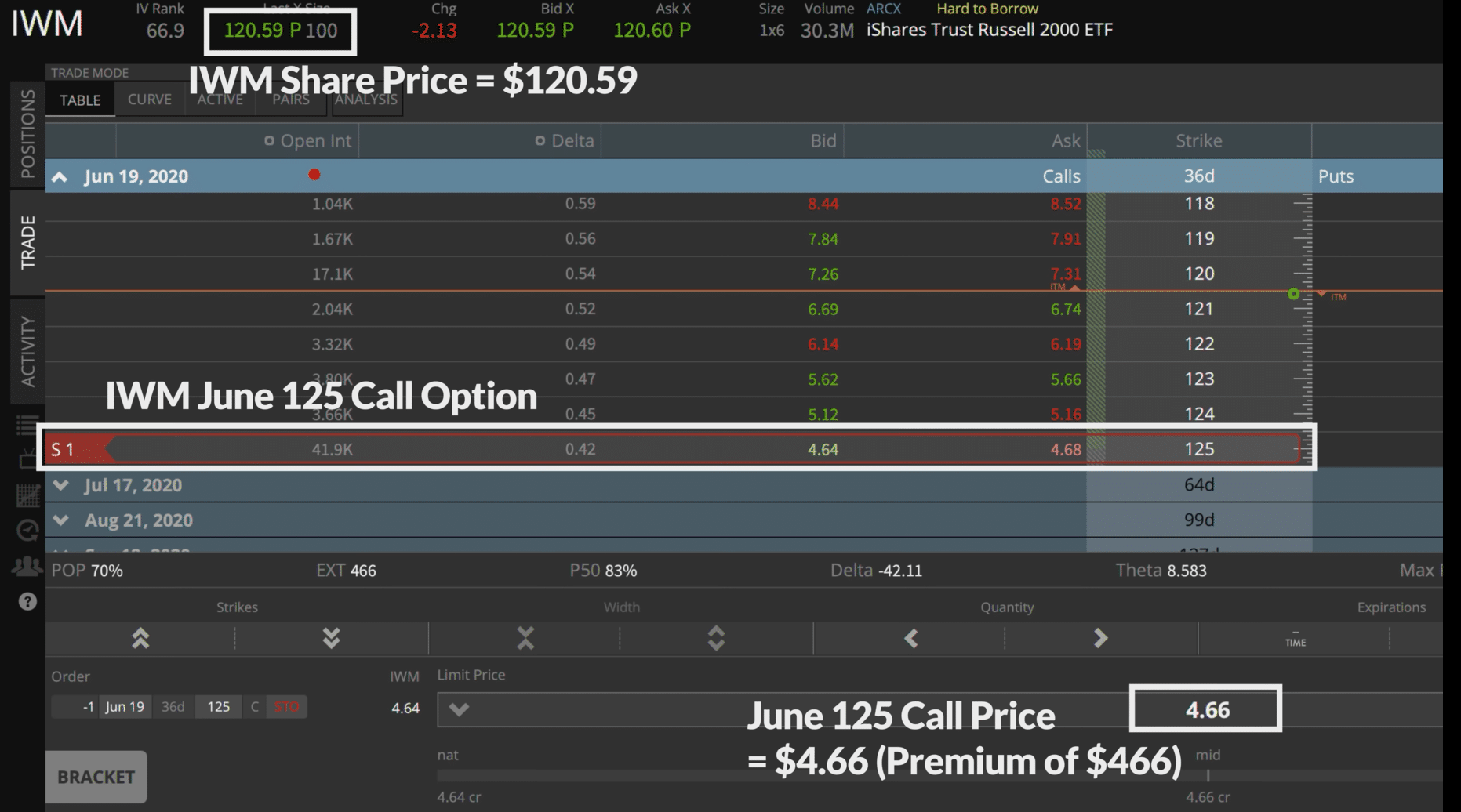

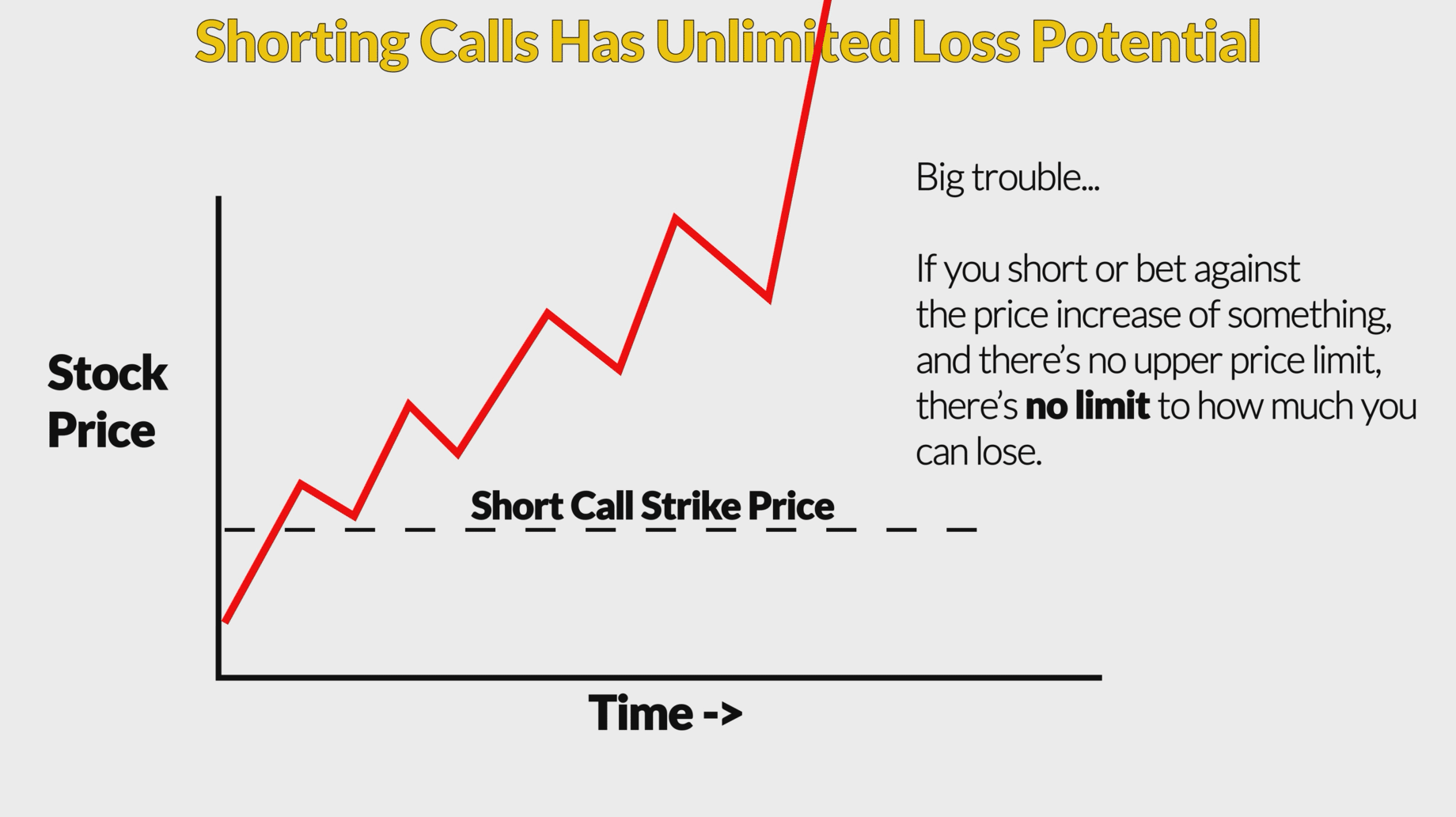

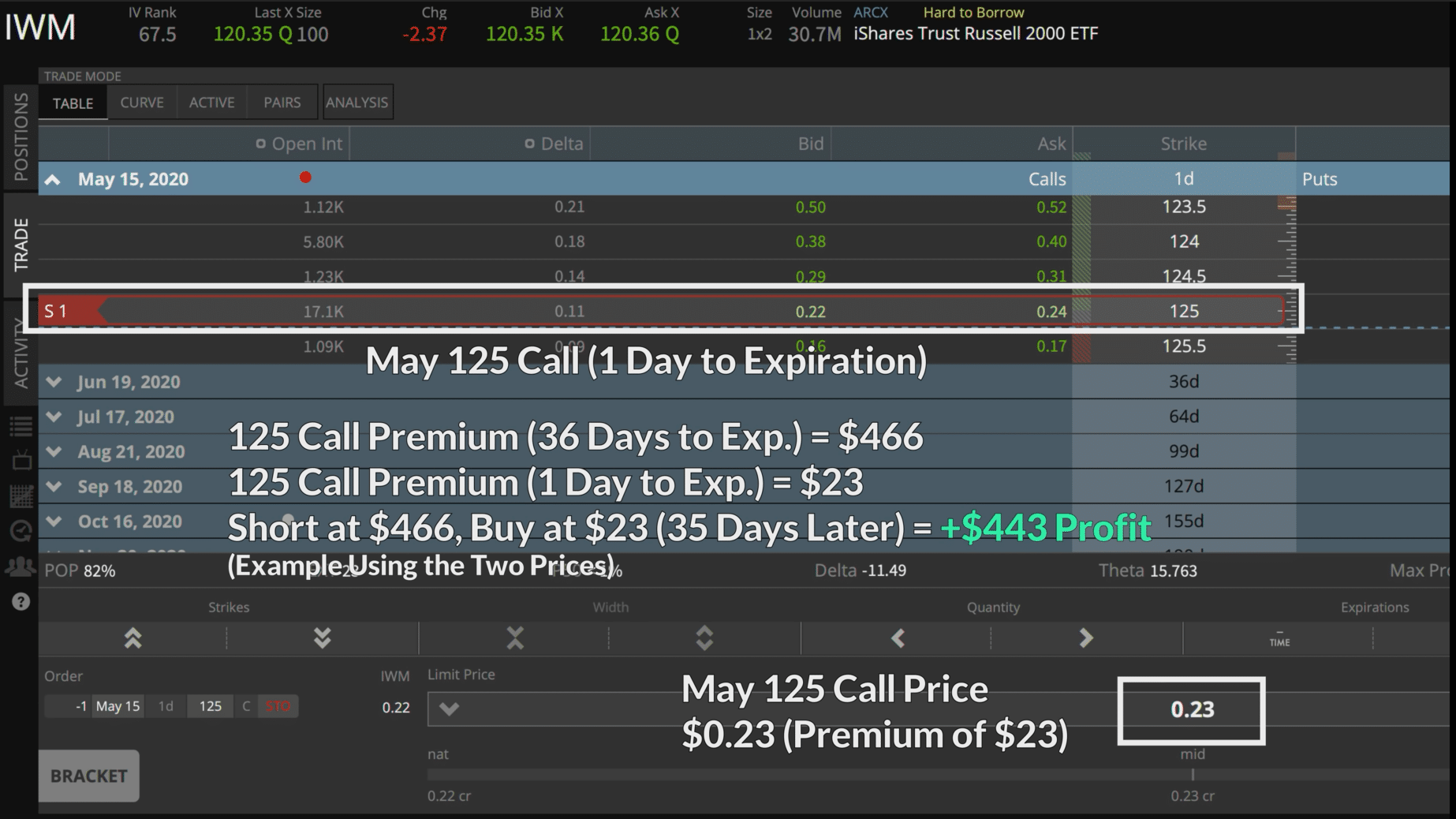

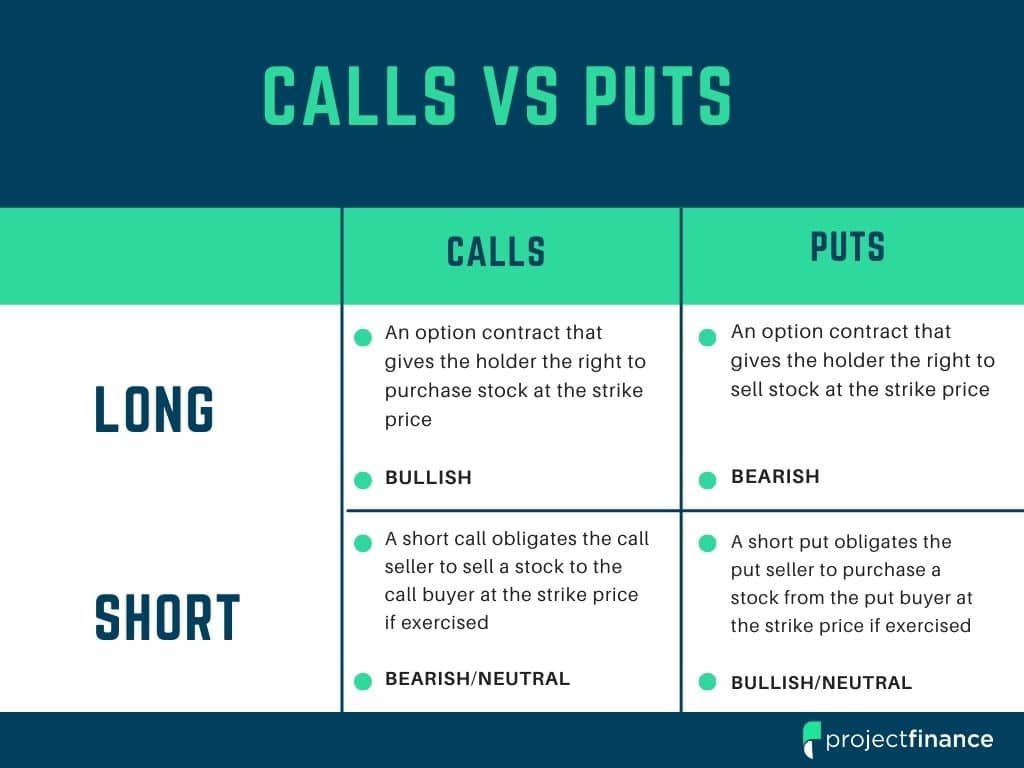

Calls vs Puts in Options Trading Explained: The Ultimate Guide

")

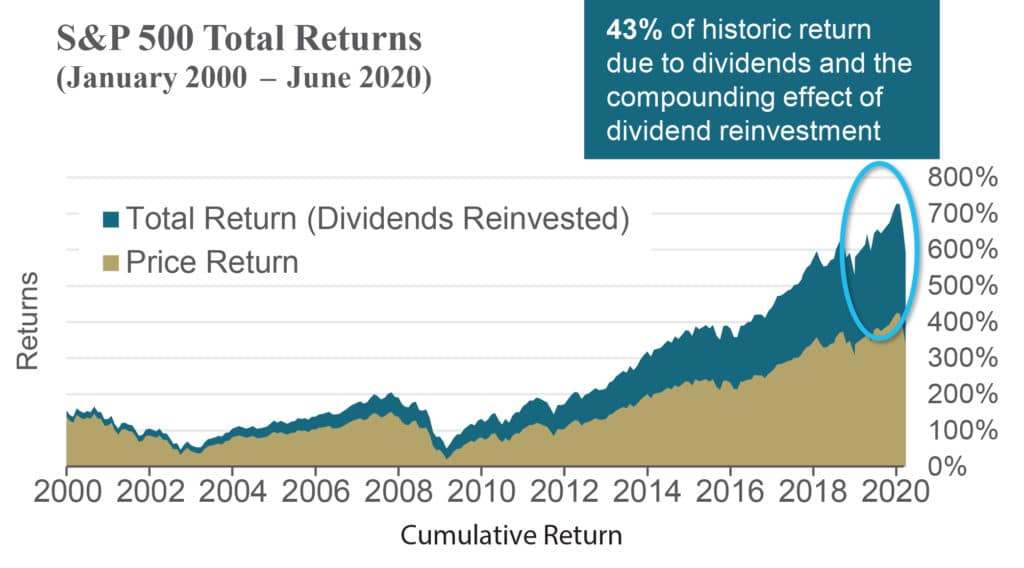

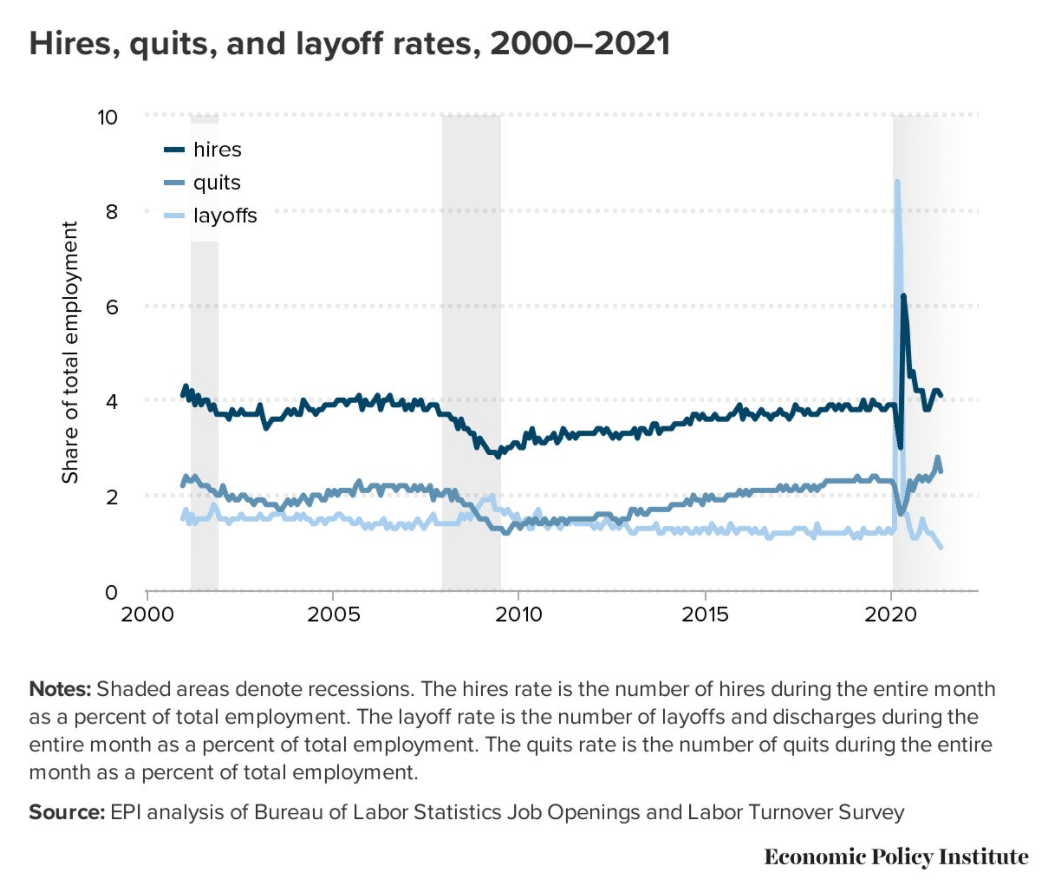

The Great Resignation, Entrepreneurship and Stocks

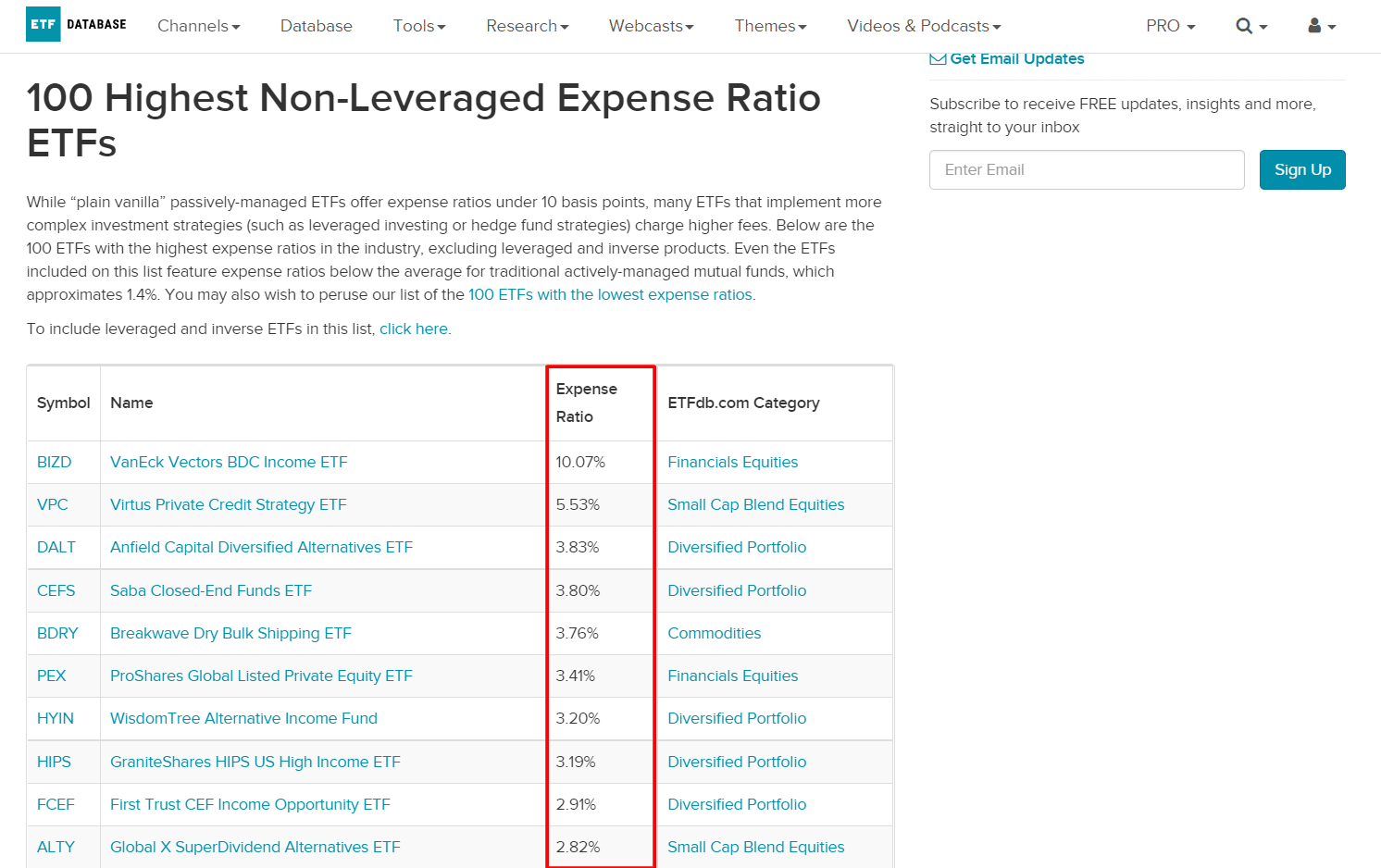

ETFs Explained: Investing Basics

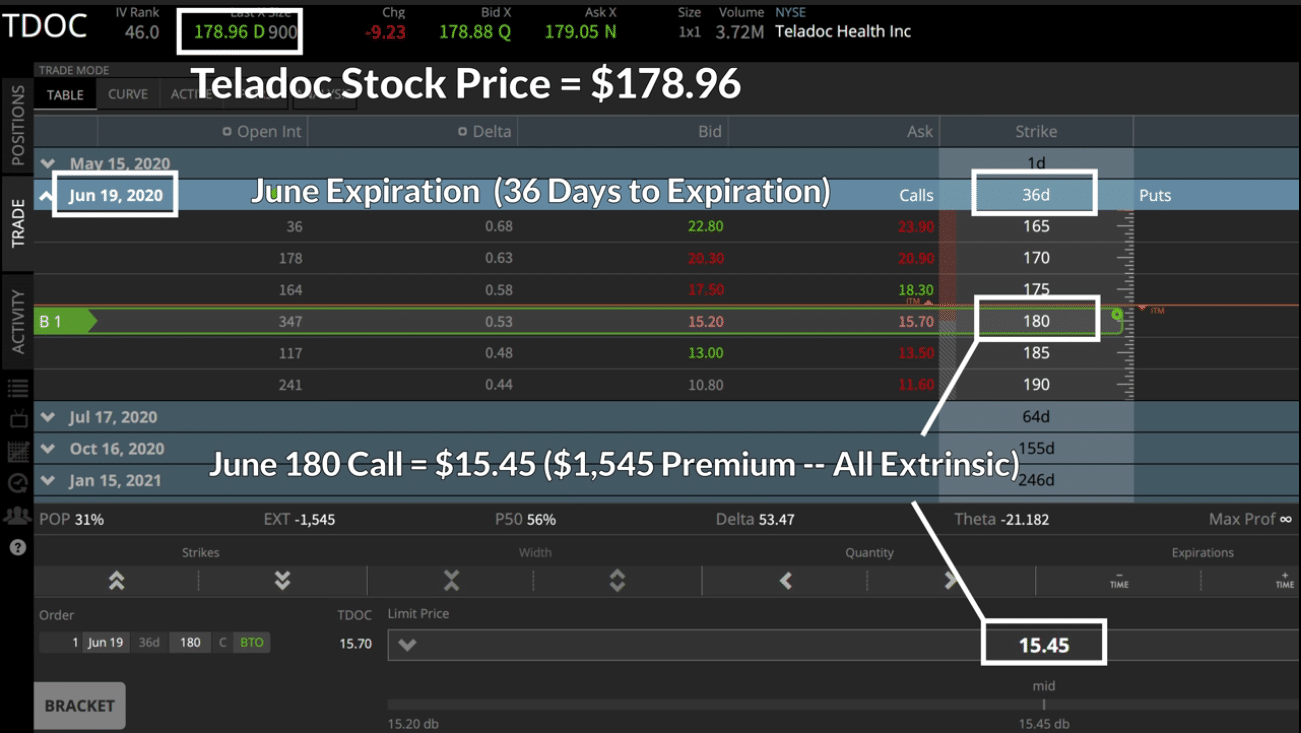

Options Trading for Beginners: The ULTIMATE Guide

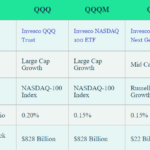

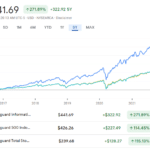

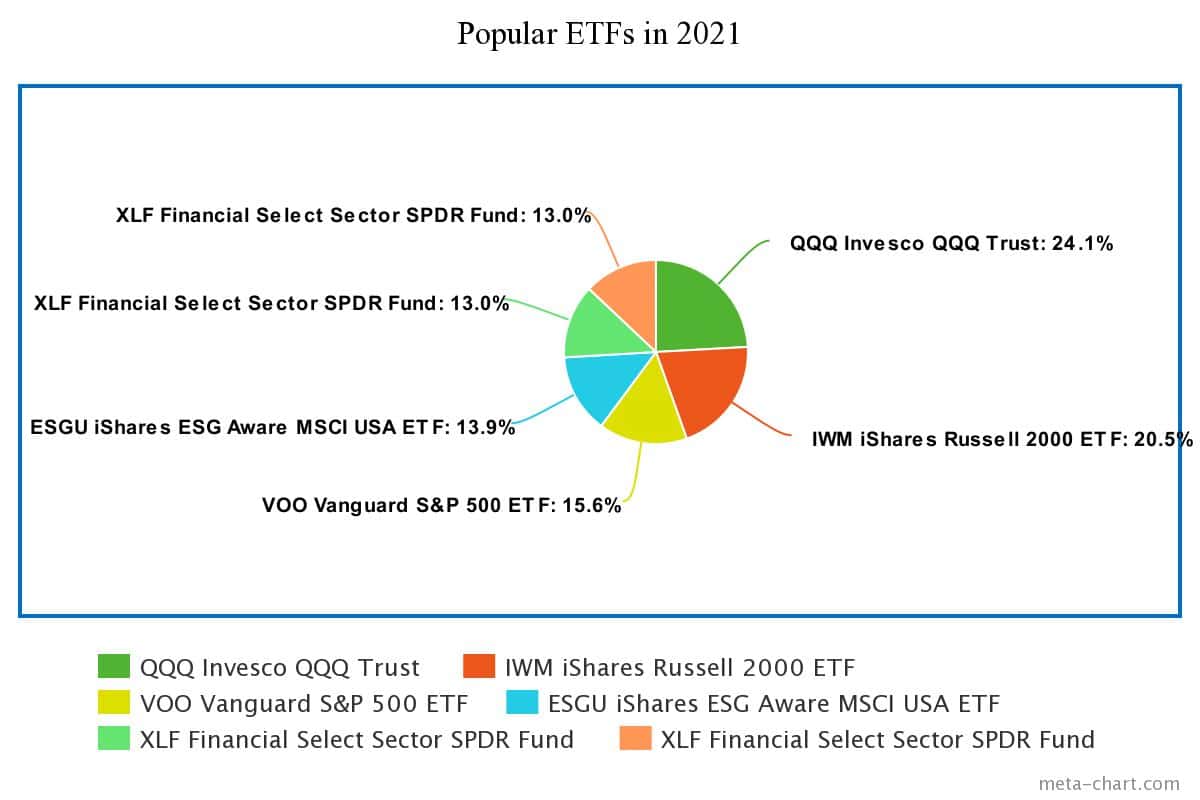

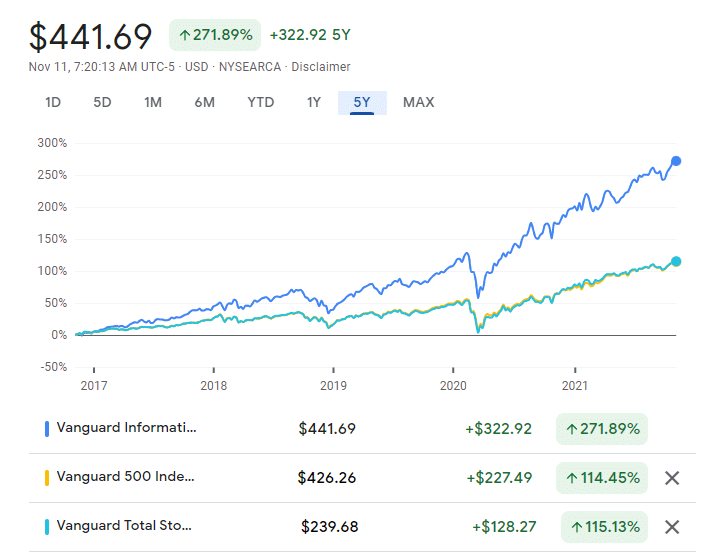

VTI vs VOO vs VGT: Here’s How They Differ

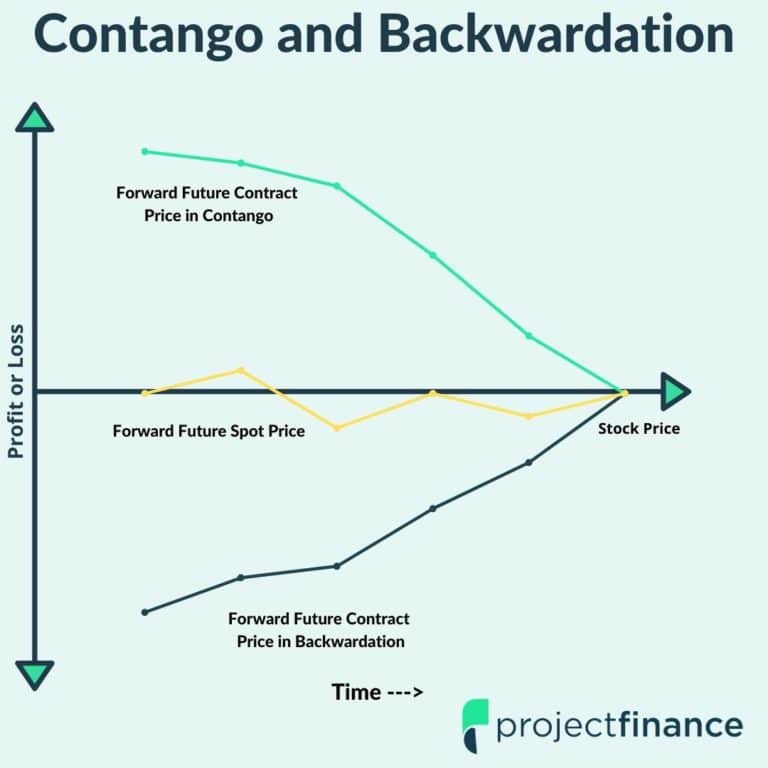

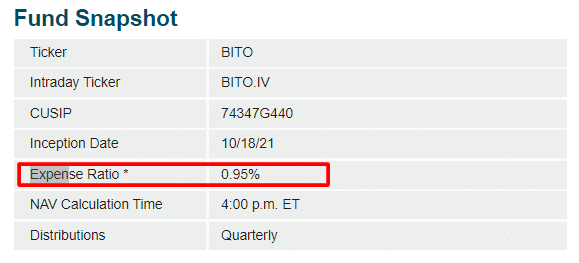

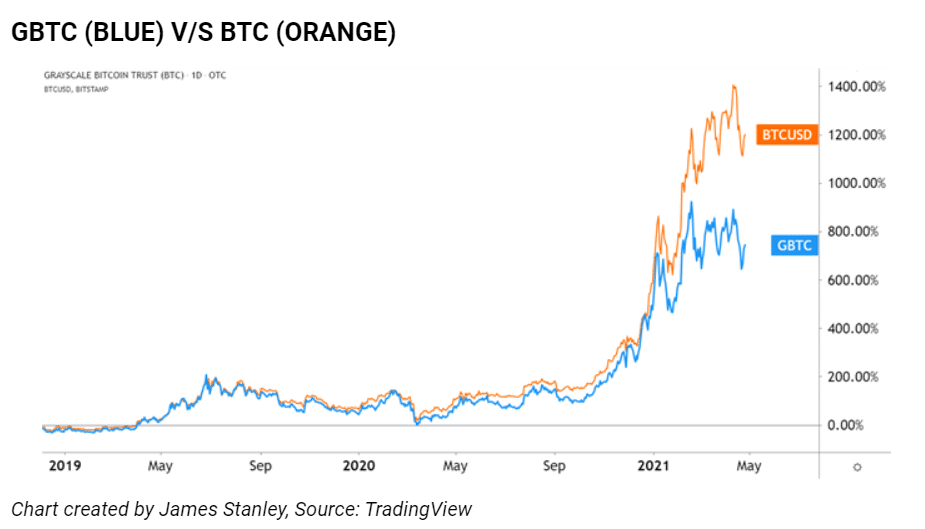

ProShares BITO ETF Explained