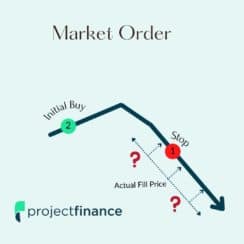

Investing TIF Orders Types Explained: DAY, GTC, GTD, EXT, GTC-EXT, MOC, LOC Read More » February 18, 2022