(1)")

UVXY: Contango vs Backwardation

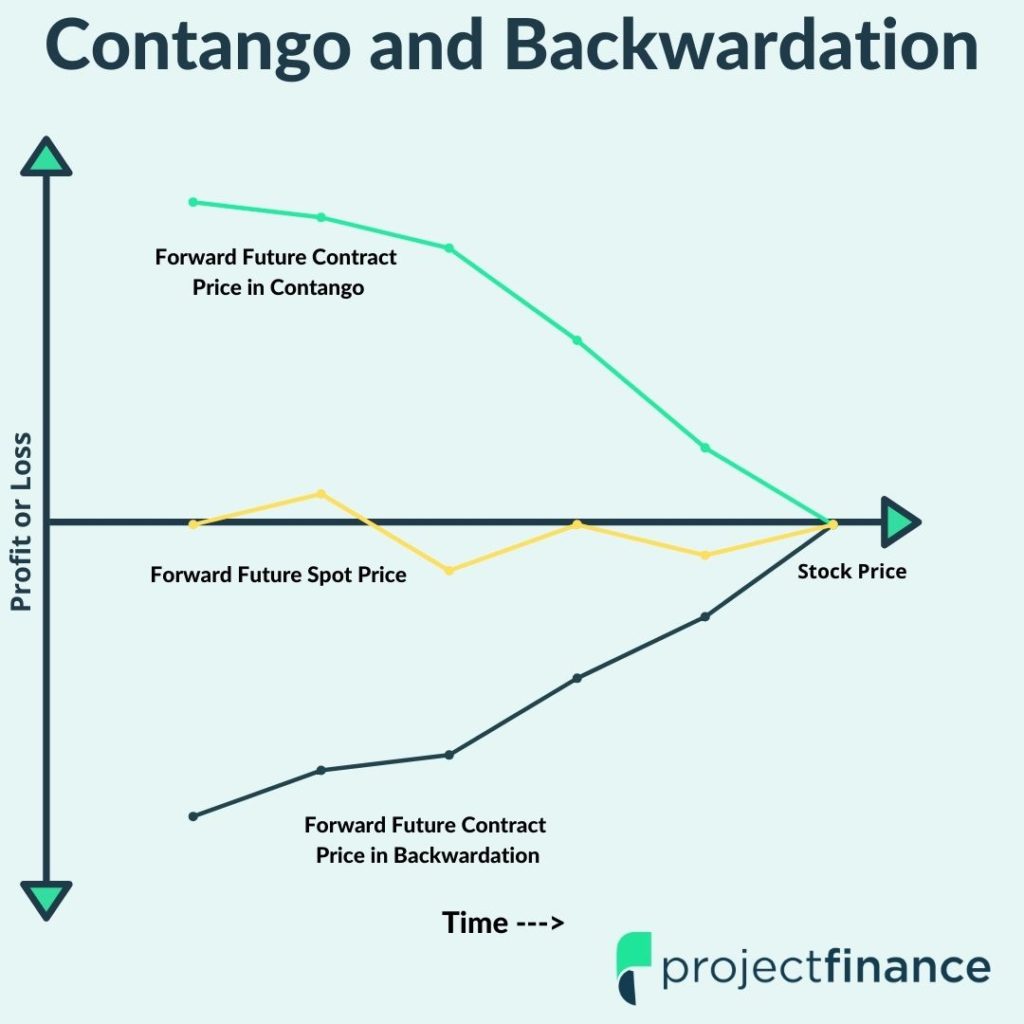

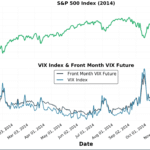

When the VIX futures contracts are trading at a premium to the VIX index, the VIX futures are in contango.

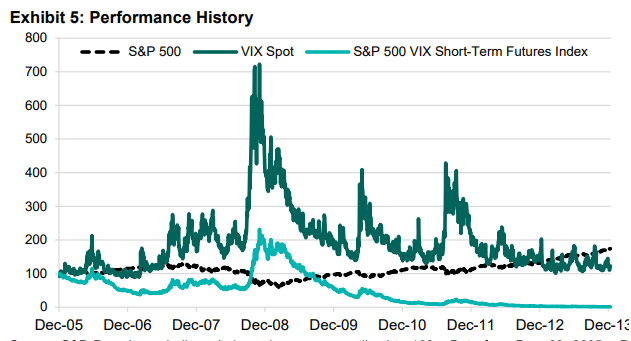

UVXY tracks the daily performance of the two nearest monthly VIX futures, such as February and March in the above example.

If the VIX index remains at 15 as time passes, the February and March VIX futures will steadily lose value as they converge to 15 because a VIX futures contract at maturity will be equal to the spot price (the VIX index).

And since UVXY tracks the daily percentage change of a mixture of these two contracts that are steadily losing value in this scenario, UVXY loses value.

UVXY in Backwardation

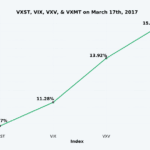

If the VIX futures contracts are trading below the VIX index, then the futures are in backwardation and will gain value as they converge towards the higher VIX index (assuming the VIX index remains elevated over time).

In this scenario, UVXY will gain value because it tracks the daily percentage change of a mixture of these two contracts that are gaining value as they converge towards the higher VIX index.

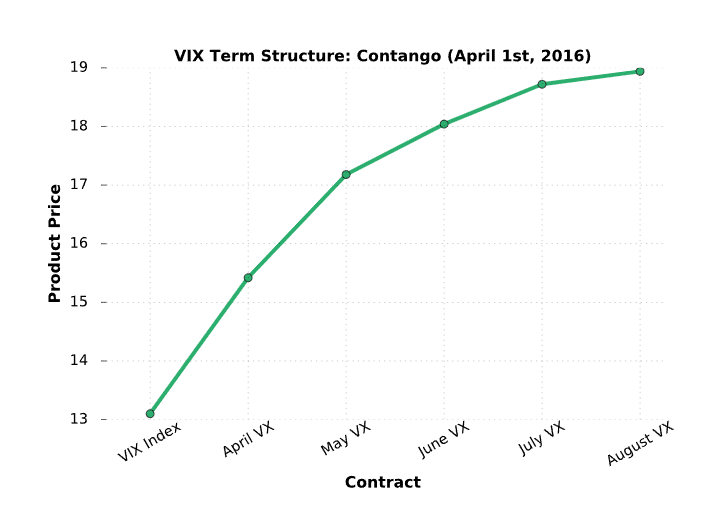

So do we have any idea how fast, or at what rate ETFs like UVXY will decay? Maybe, and that leads us to the VIX Term Structure.

4 thoughts on “UVXY: What Is It and Is It Worth The Risk?”

Thanks for the article!

Just curious – is there any advantage to trading UVXY over VXX?

Thanks!

Thanks for the question Eileen!

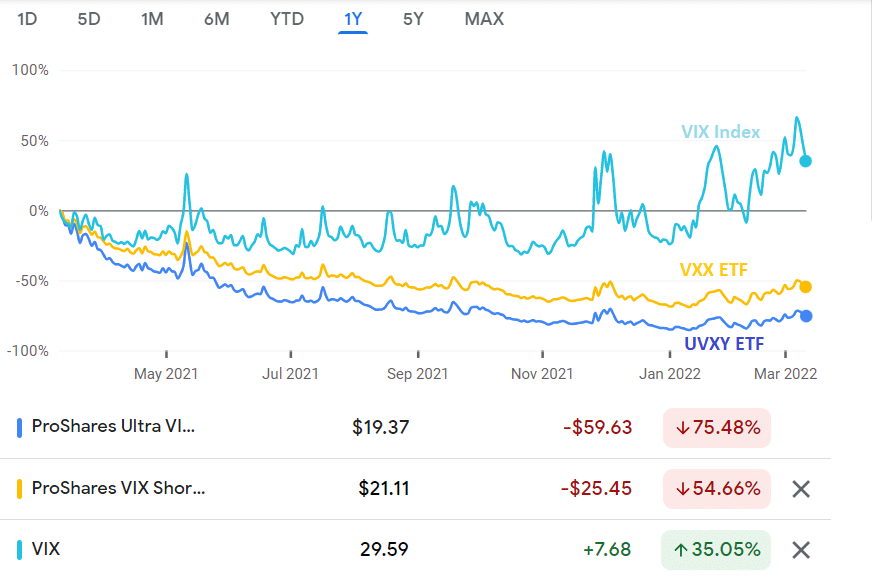

UVXY is a leveraged ETN while VXX is a non-leveraged ETN. This means that UVXY will be more sensitive to changes in volatility than VXX. UVXY is leveraged on a 1.5 basis. The leverage is small, but over time it really has an impact!

Also, Barclays recently stated they will suspend further issuance of VXX.

Mike

I’m really glad I came across this article! Thank you for posting it. In terms of price degradation over time due to contango – would a stronger leveraged product like UVIX (2x VIX) experience a higher degree of price degradation over time than UVXY?

Thank you!

-Kyle

Hi Kyle!

Thanks for reading the post! I’m glad it was helpful.

Yes, a more leveraged product will experience more decay (and also increases) over time. For instance, if the VIX remained low at 15 for a year, VIX futures would be in a constant state of contango and a leveraged long vol product will lose more value than an unlevered/less leveraged long vol product.

-Chris