Search

About

Blog

Contact

About

Blog

Contact

Search

Watch on YouTube

Category: Options Trading

Options Trading

Bid Size vs. Ask Size in Options & Stocks Explained

Read More »

September 15, 2022

Options Trading

29 Core Options Trading Strategies For Beginners

Read More »

May 9, 2022

Options Trading

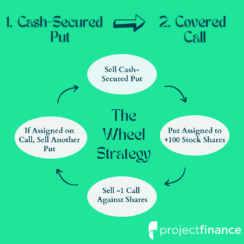

The Wheel Options Strategy: Collect Income From Options

Read More »

May 25, 2022

Investing

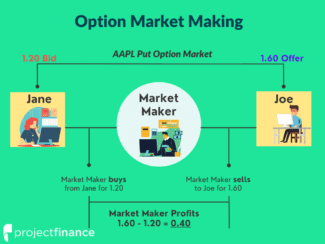

Market Makers in Options Trading: What Do They Do?

Read More »

March 12, 2025

Options Trading

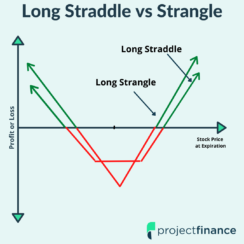

Options Straddle vs Strangle: How Do They Differ?

Read More »

April 5, 2022

Options Trading

What Is Options Trading?

Read More »

March 31, 2022

Options Trading

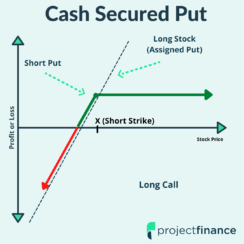

What Is a Cash-Secured Put? Get Income or Cheap Stock

Read More »

May 6, 2022

Options Trading

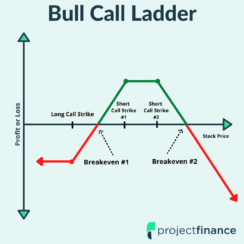

Long (Bull) Call Ladder Options Strategy: Visual Guide

Read More »

April 7, 2022

Options Trading

Poor Man’s Covered Call [The Ultimate Beginner’s Guide]

Read More »

May 6, 2022

Options Trading

Options Trading Approval Levels: Broker Guide

Read More »

March 24, 2022

«

Page

1

Page

2

Page

3

Page

4

Page

5

»