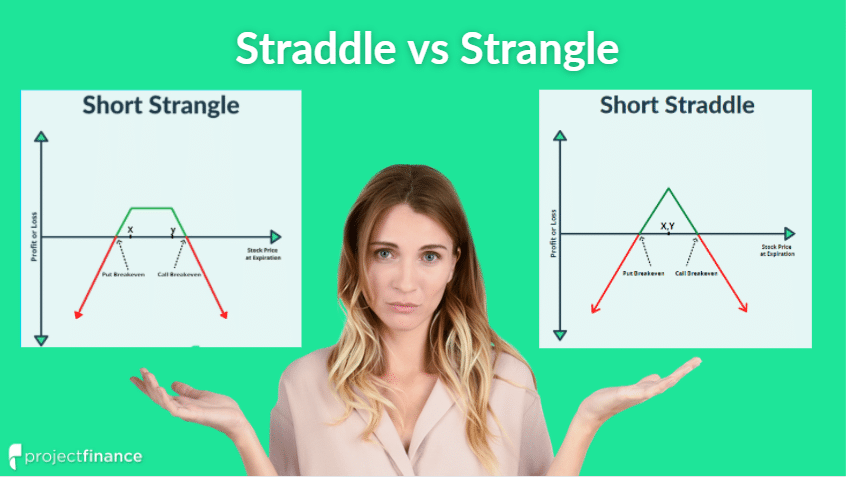

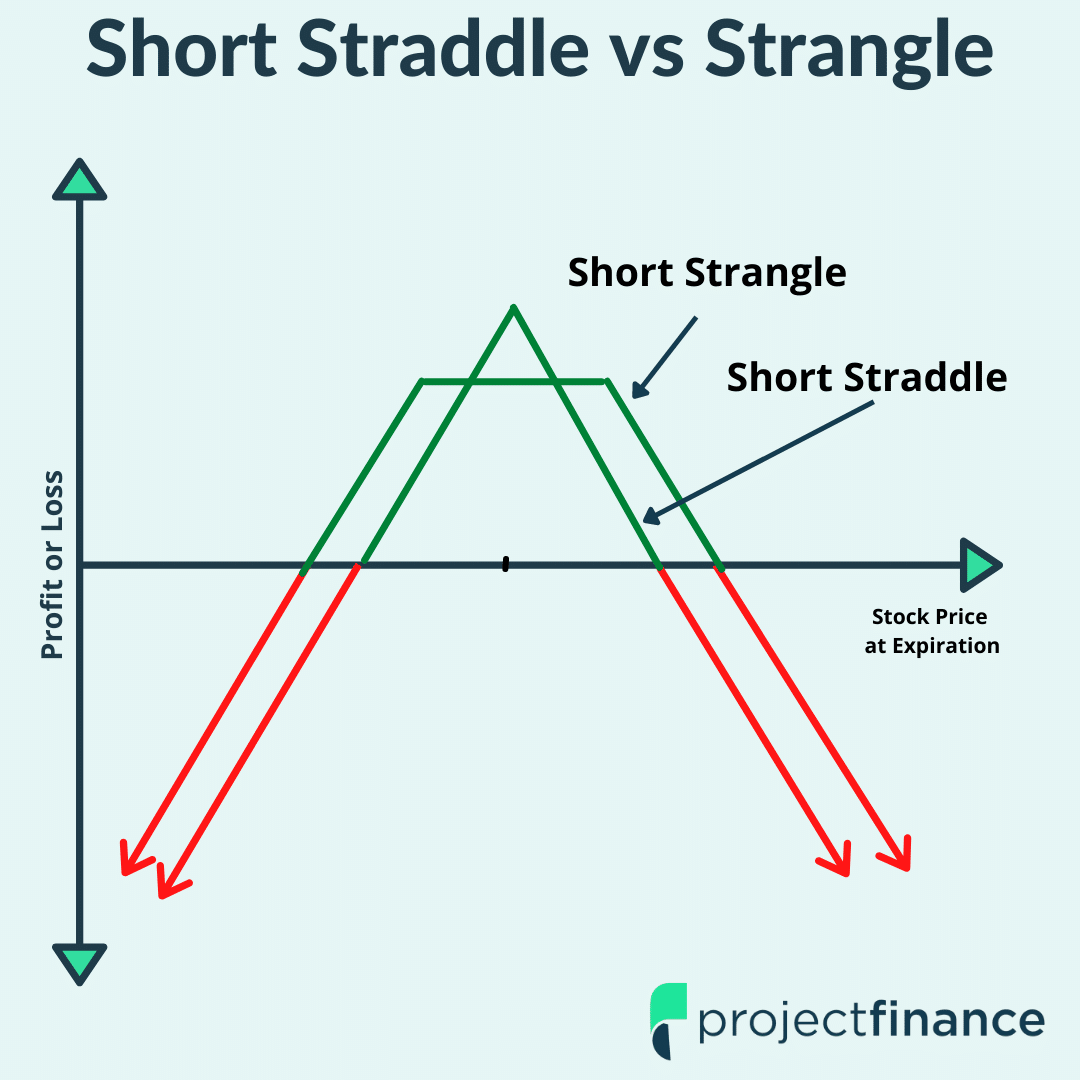

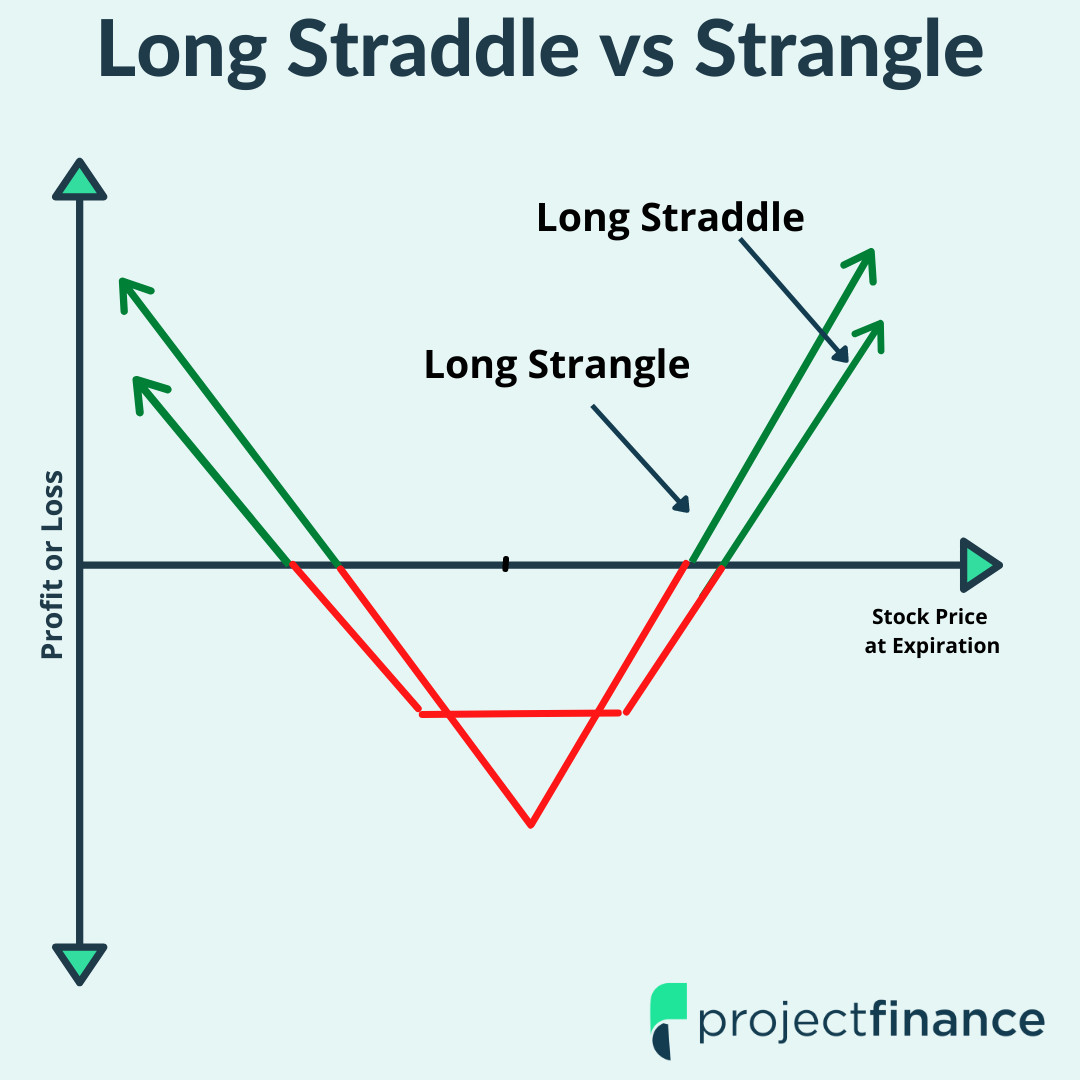

Option straddles are comprised of “at-the-money” options. Option strangles are comprised of “out-of-the-money” options. Since out-of-the-money options are cheaper than at-the-money options, the strangle strategy is cheaper to buy than the straddle strategy.

(1)")