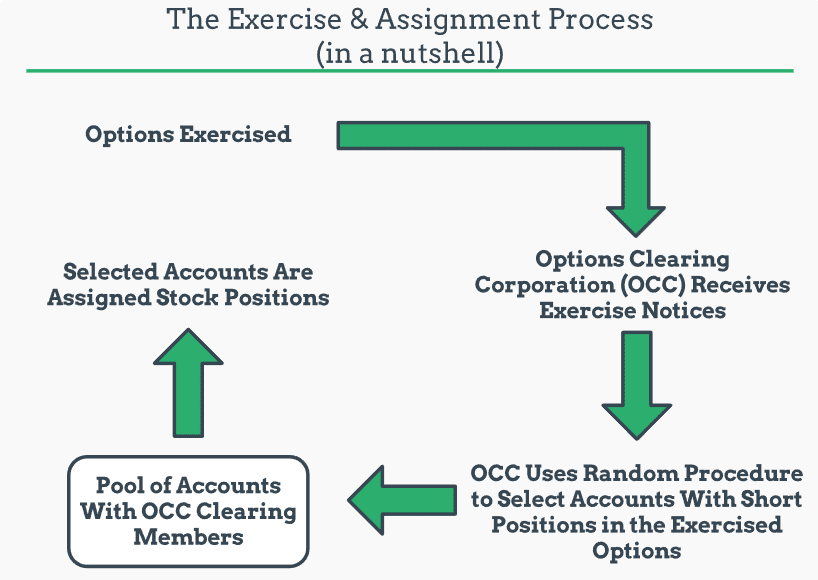

The final piece of understanding exercise and assignment is gauging the risk of early assignment on a short option.

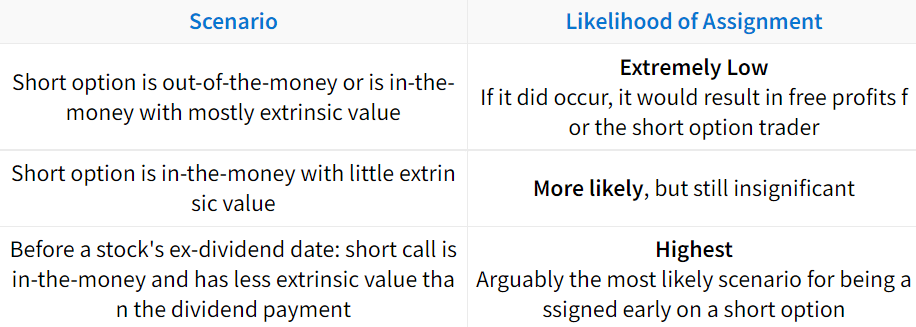

As mentioned early, only 7% of options were exercised in 2017 (according to the OCC). So, being assigned on short options is rare, but it does happen. While a specific probability of getting assigned early can’t be determined, there are scenarios in which assignment is more or less likely.

The following scenarios summarize broad generalizations of early assignment probabilities in various scenarios:

(1)")