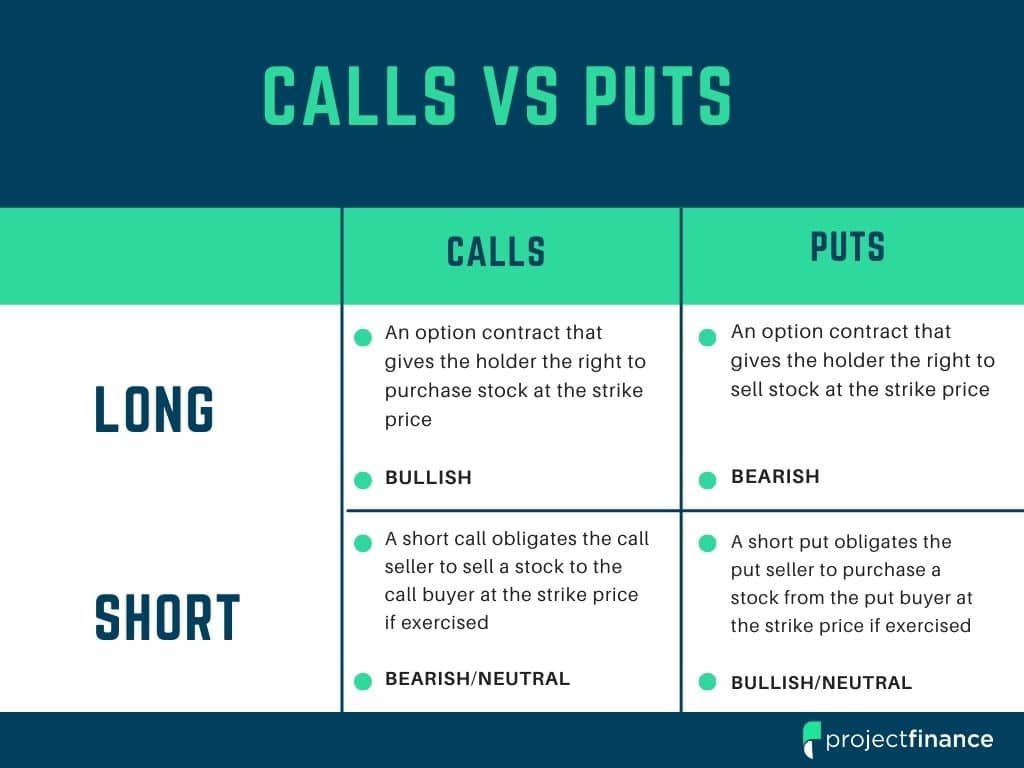

Selling put options are better suited when you are neutral or slightly bullish on a security. Call options are best for very bullish markets.

If you buy a call option and the price of the underlying asset does not rise significantly, you will not make money. Selling a put in this situation would make money. However, selling puts has far greater risk than buying calls.

")

(1)")

2 thoughts on “Calls vs Puts in Options Trading Explained: The Ultimate Guide”

Thanks for the article!

I bought a call option that is going to expire today. I’m trying to sell the option before it expires but I can’t. It won’t even accept an order for 0.01. Any idea why? Thanks!

Thanks for the question Nefeli!

Unfortunately, it sounds like your call option is worthless. I’m guessing the strike price of your call is quite far away from the price of the underlying stock.

In these situations, exercising your call would have no benefit as opposed to simply buying the stock in the market. This is the reason that no party is willing to “buy” this call from you.

Mike