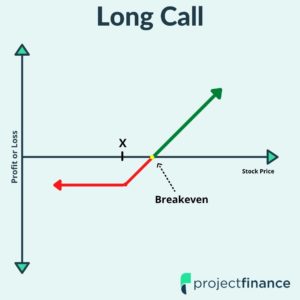

In options trading, a call option (call) is a financial contract between a buyer and seller that gives the owner the right to buy the underlying security (generally stock) at a certain strike price within a specific time frame.

The buyer of a call will profit when the underlying market increases in value. Since there is no cap on the price of most assets, the seller of a single call option has infinite risk.

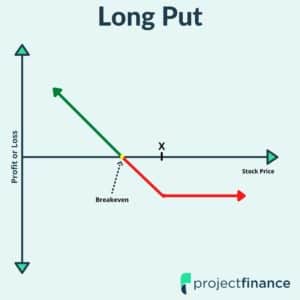

Put options are the opposite of call options. Whereas a call option is a financial contract that gives the holder the right to buy a security at a particular strike price on or before the expiration date, a put option gives the holder the right to sell the security (generally stock) under the same circumstances.

Put options increase in value when the underlying market decreases. An investment in a long put option thus acts as an insurance product if held with long stock.

(1)")

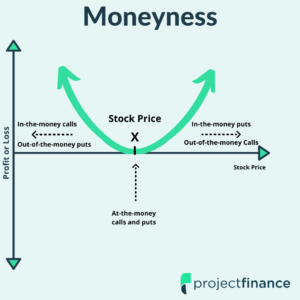

In options trading, the term “moneyness” is used to determine the intrinsic value of an option at any given time. An option can either be in the money, out of the money, or at the money. The relationship between the underlying stock price and the option strike price dictates where the option currently is on the money scale.

Long-term Equity Anticipation Securities (LEAPS) are extended options that track the price of underlying stocks or indices. Options with expiration dates greater than one year out fall into this category. LEAPS trade just like all other options of their class, with the exception of this prolonged expiration date. Investors sometimes use LEAP put options as a long-term insurance policy against their stock.