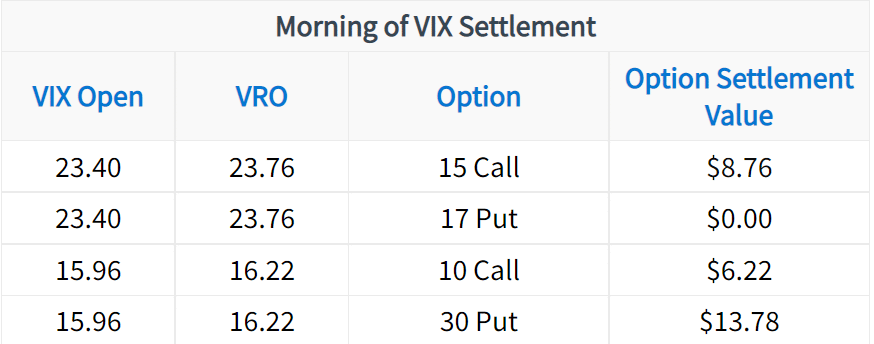

(1)")

As we can see, the deep-in-the-money January VIX put is priced almost perfectly to the price of the January volatility future. So, don’t be fooled by any potential “mispricings” when examining options on the VIX.

To hammer this point home one last time, we’ll visually compare the prices of the VIX index and the cost of a long synthetic stock position (strike price of synthetic + cost of synthetic) on the VIX. A long synthetic stock position consists of a long call and short put at the same strike price, and in the same expiration. As the name suggests, a synthetic stock position should replicate a position in the underlying shares.

On the VIX, this means the synthetic should track the underlying product price (the VIX) very closely. Let’s take a look at the long synthetic in VIX options compared to the VIX Index:

Clearly, the cost of the long synthetic does not match up well with the price of the index, as it would with standard equity options on non-dividend stocks. However, if we add in the price of the future that corresponds to the options on the VIX, they should track each other almost perfectly:

Note that any subtle differences between the price of the synthetic stock position and the VIX future can be attributed to using the mid-price of the options in the synthetic and the mid-price of the VIX future.

When trading VIX options, you might wonder why you don’t just trade the longest-term VIX options to allow more time for your positions to profit.

The answer is that not all VIX options have the same sensitivity to changes in market implied volatility. When examining movements of the VIX Index and futures, you’ll notice that the VIX Index is more responsive to market movements compared to VIX futures with more time until settlement.

As a result, longer-term options on the VIX are less sensitive to changes in implied volatility.

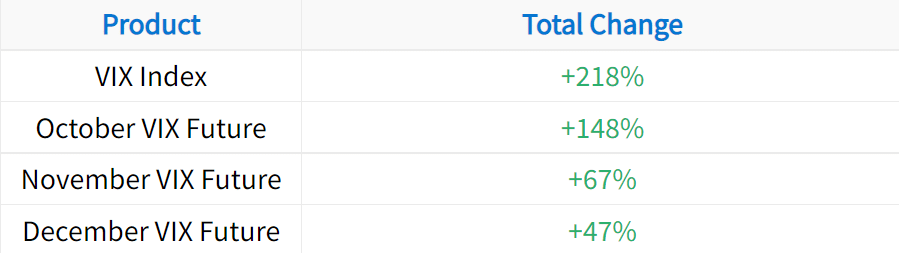

Consider the following visualization of three different VIX futures contracts in 2008:

Between September 2nd and October 10th, the following movements occurred in each volatility product:

Let’s compare the changes in the call options with strike prices of 20 over the same period:

As we can see, when the VIX increased from 20 to 70, the October 20 VIX call increased from $3.90 to $35.00, while the December 20 VIX call only increased from $4.20 to $14.10.

While trading long-term options on the VIX might give you more time to be right, volatility will need to experience much more significant changes for your positions to profit.

2 thoughts on “Here’s How to Trade VIX Options (3 Things to Know)”

Thanks for the article!

I’m generally bearish on the VIX. Is it better to trade options on the VIX directly or VIX ETFs?

Thanks for the question Mary!

If you’re long-term bearish on the VIX, trading VIX-based ETFs and ETNs may work out better for you. Why? Over time, these products tend to experience “contango”, which has an adverse effect on the underlying. Most of the time, volatility-based ETFs underperform the VIX.

Hope this helps!

Mike