Search

Search

About

Blog

Contact

Menu

About

Blog

Contact

Search

Search

Watch on YouTube

Month: September 2021

Investing

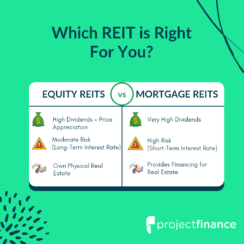

Equity REITs vs Mortgage REITs + 13 Best Stocks

Read More »

March 2, 2022

Investing

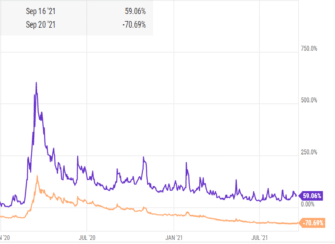

5 Way VXX Options Differs from VIX Options

Read More »

April 9, 2022

Investing

17 Best Low-Priced Stock ETFs for Beginners with Little Money

Read More »

April 21, 2022

Investing

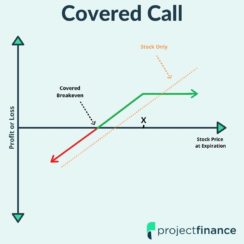

7 Covered Call ETFs and How They Work

Read More »

April 19, 2022

Options Trading

The Vertical Spread Options Strategies: Beginner Basics

Read More »

March 24, 2025