Search

Search

About

Blog

Contact

Menu

About

Blog

Contact

Search

Search

Watch on YouTube

Month: October 2021

Options Trading

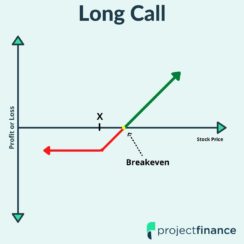

Here’s How a Long Call Option Works (W/ Visuals)

Read More »

March 24, 2022

Options Trading

Stop-Loss Orders On Options Explained

Read More »

February 16, 2022

Cryptocurrency

The HUGE risks of a Bitcoin ETF: Futures ETFs Explained

Read More »

February 11, 2022

Options Trading

Long Call Calendar Spreads Explained

Read More »

February 11, 2022

Options Trading

Dangers of After Hours Options Assignment

Read More »

February 11, 2022

Options Trading

Options That Trade Until 4:15 pm (3:15 Central)

Read More »

March 11, 2022

Investing

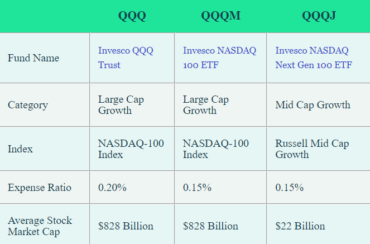

Differences Between Invesco’s QQQ, QQQM, and QQQJ

Read More »

February 11, 2022