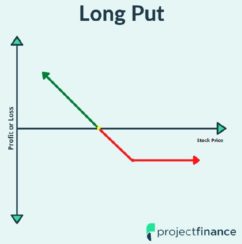

Options Trading Long Put Option Strategy for Beginners | projectfinance Read More » February 14, 2022