Search

Search

About

Blog

Contact

Menu

About

Blog

Contact

Search

Search

Watch on YouTube

Month: March 2022

Retirement

FAQ: Can You Cash Out a Life Insurance Policy for Retirement?

Read More »

April 6, 2022

Options Trading

What Is Options Trading?

Read More »

March 31, 2022

Retirement

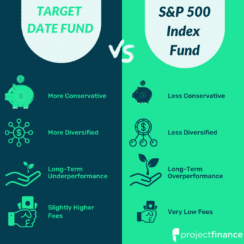

Target-Date Funds vs S&P 500 Index Funds: Which is Better?

Read More »

April 19, 2022

Investing

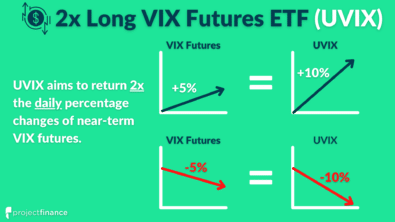

What is UVIX? (2x Long Volatility ETF Explained)

Read More »

March 29, 2022

Investing

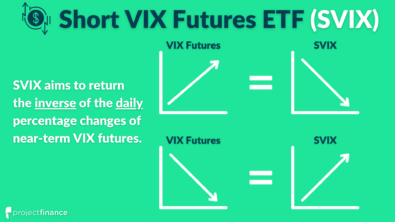

What is SVIX? (Short Volatility ETF Explained)

Read More »

March 29, 2022

Options Trading

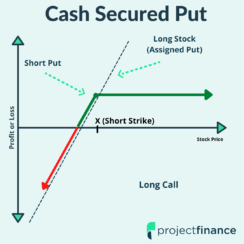

What Is a Cash-Secured Put? Get Income or Cheap Stock

Read More »

May 6, 2022

Investing

Money 101: The Functions & Characteristics of Money

Read More »

April 25, 2022

Options Trading

Long (Bull) Call Ladder Options Strategy: Visual Guide

Read More »

April 7, 2022

Retirement

The Pros and Cons of a SEP-IRA for Retirement

Read More »

March 30, 2022

Options Trading

Poor Man’s Covered Call [The Ultimate Beginner’s Guide]

Read More »

May 6, 2022

«

Page

1

Page

2

»