Choosing between target-date funds and index funds is a very common dilemma for retirement investors with a long-term time horizon.

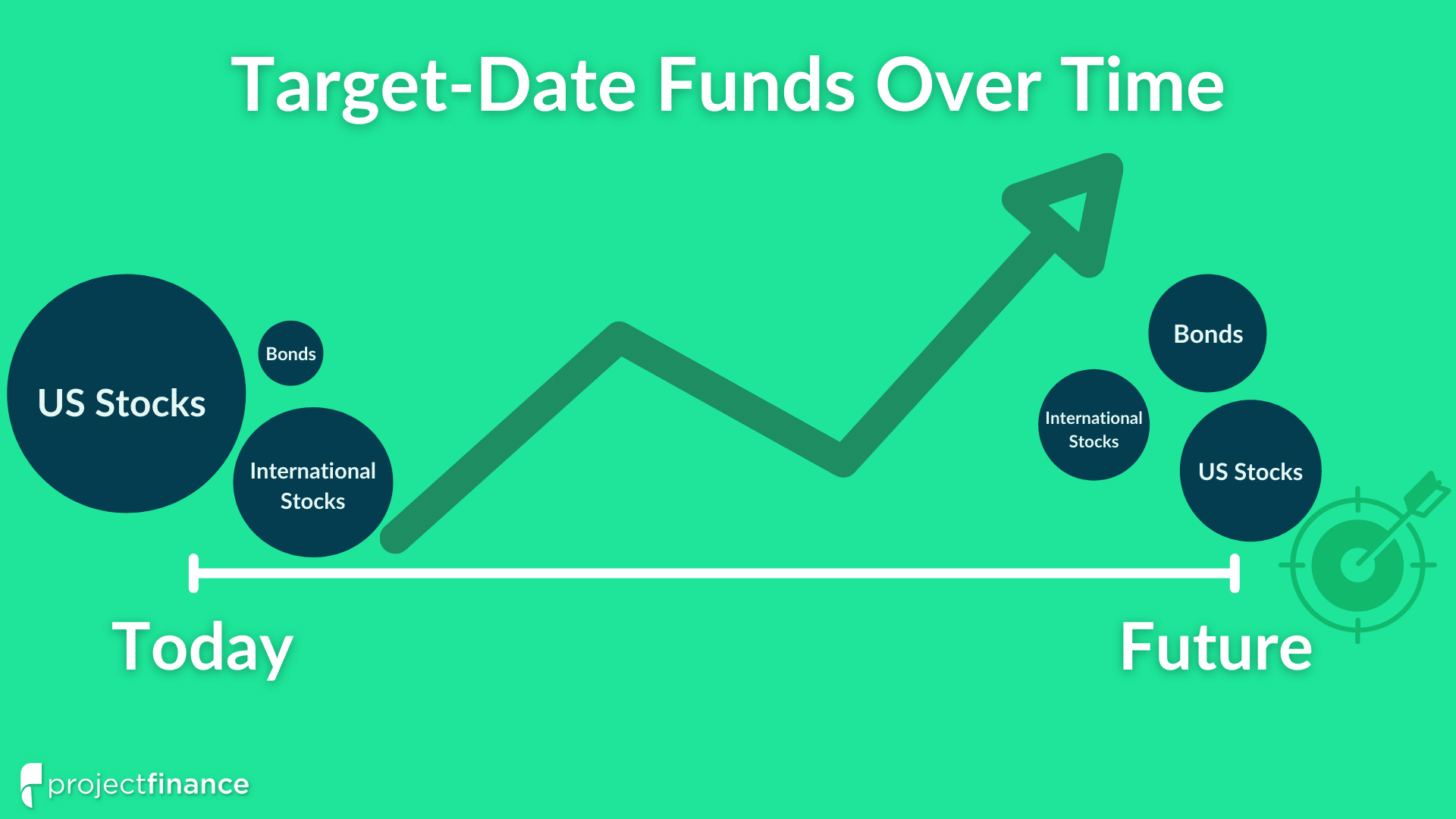

➥ Target-date funds are incredibly diverse investment products that aim to grow assets for a specific time frame. These low-cost funds are actively managed and restructured to offset risk as the target retirement date approaches using the “glide path” approach.

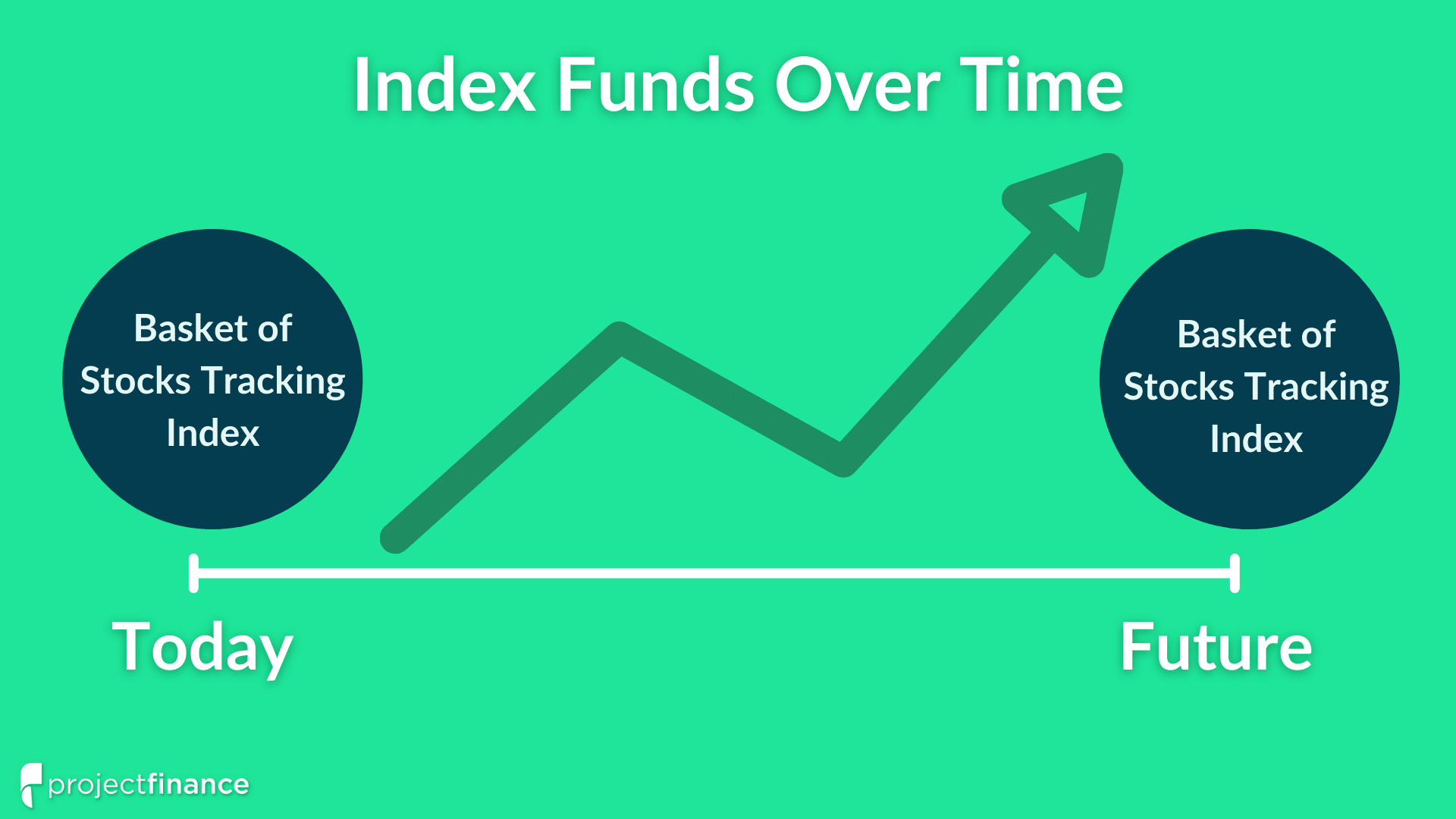

➥ S&P 500 Index funds are generally less diverse investment vehicles that have no time frame.

Because index funds have no “targeted” date, the holdings within these funds do not adapt to investors’ risk tolerance, which generally decreases with age.

For long-term, retirement-minded investors, target-date funds appear to be the better investment strategy. Why? Target funds simplify the process of saving for retirement. Instead of choosing amongst dozens of equity and bond funds, target-date funds only require you to have one position! Within this one position are numerous assets and types of securities.

But which type of fund actually performs best?

Though nobody knows what will happen in the future, this article aims to compare the past performance of target-date funds with index funds, specifically index funds that track the S&P 500 benchmark.

Jump To

TAKEAWAYS

Target-date retirement funds are designed to reduce risk as time passes and the target retirement date approaches.

S&P 500 index funds represent the largest 500 companies in the US and are not custom-tailored to investors changing risk levels.

Target-date funds contain equities of all market caps, as well as bond, international, and emerging market stocks.

American stocks tend to outperform both bonds and international stocks over time.

S&P 500 index funds can be combined with target-date funds for investors looking for more American equity exposure.

Index funds typically have marginally smaller fees than target-date funds, though these higher expense ratios are negligible.

How Do Target Date Funds Work?

Target-Date Fund Definition: A target-date fund – also known as an age-based or lifecycle fund – is a mixed allocation fund that seeks to grow assets over a specified time period for a target date.

When you’re 25, you can and should take on more risk than when you’re 55.

But how do you know what proportion of your retirement and savings should be in fixed-income (bonds) versus equities at various stages of your life? What about the large-cap to small-cap ratio? And what about money markets?

Target-date funds were designed to do this work for us. These funds rebalance as the target date approaches to change with investors risk appetites, which decrease with age.

Before the target-date fund, if an investor didn’t have a financial advisor, determining asset allocation was pretty much guesswork. And there really is no right answer – just a lot of grey.

Since this article is going to be comparing target-date funds with index funds, let’s explore the world of index funds before we move on

How Do Index Funds Work?

Index Fund Definition: Index funds can be either mutual funds or exchange-traded funds (ETFs). Index funds seek to track the returns of a market index.

So index funds track market indices. What type of market indices do they track? Innumerable. Let’s look at a few of the more popular ones now:

In order to invest in these indices, investors can either purchase mutual funds or ETFs. ETFs are becoming more popular investment vehicles because of their low fees and high liquidity.

These two products are identical in almost every way. Two exceptions lie in their structure and fees:

1.) VFIAX charges a fee of 0.04%; VOO charges a fee of 0.03%

2.) VFIAX is not exchange-traded; VOO is exchange-traded

ETFs (like VOO) are exchange-traded, meaning you can buy and sell them during market hours. Mutual funds (like VFIAX) can only be traded once a day, and you never know the fill price you are going to get when you place a buy or sell order on a mutual fund.

Advantage ETF!

For these reasons, this article will be using the VOO as its benchmark when comparing the performance of target-date funds. VOO is a top-rated S&P 500 tracker, earning 5 stars at Morningstar.

Target-date funds have a lot in common with index funds. After all, target-date funds are comprised of index funds! In theory, you should be able to mirror any target-date fund on your own with index funds.

This is a good strategy for investors with both higher and lower risk tolerances than the benchmark target-date fund. For investors wanting less risk, more bond funds, as well as money market funds, can be used in tandem with the target-date fund. For more risk-on investors, equity index funds can be used to supplement target-date funds.

All investors have different risk appetites. Investing is not a one-size-fits-all business. So why are target-date funds so popular? Because they’re easy and cheap!

Let’s next look under the hood of both target-date funds and index funds.

Fund issuers must employ teams of fund managers and price stabilizers to make sure the funds do indeed track the underlying index.

The management fees for both Vanguard’s index funds and Vanguard’s target-date funds are both very low. However, target-date funds do have marginally higher fees.

Just about all Vanguard funds are comprised of four underlying index funds. Let’s take a look at these four fund fees individually, then take a look at the expense ratios of various target-date funds.

Index Fund Fees

Fund

Expense Ratio

Vanguard Total Stock Market Index Fund Institutional Plus Shares (VSMPX)

0.02%

Vanguard Total International Stock Index Fund Investor Shares (VGTSX)

0.17%

Vanguard Total Bond Market II Index Fund Investor Shares (VTBIX)

0.09%

Vanguard Total International Bond Index Fund Investor Shares (VTIBX)

0.13%

The above funds are what constitute the vast majority of Vanguard’s target-date funds. So what fees do the actual target-date funds charge? Let’s find out!

Target-Date Fund Fees

Fund

Expense Ratio

Vanguard Target Retirement 2030 Fund

0.08%

Vanguard Target Retirement 2040 Fund

0.08%

Vanguard Target Retirement 2050 Fund

0.08%

Vanguard Target Retirement 2060 Fund

0.08%

Given the relatively high fees for Vanguard’s “International Stock” and “International Bond” funds, the expense ratios for target-date funds are pretty much as they should be.

But what are the fees for VOO, Vanguard’s S&P 500 index-tracking ETF?

Vanguard S&P 500 ETF (VOO) Fee: 0.03%

Therefore, we can conclude that investing solely in Vanguard’s S&P 500 ETF is cheaper than investing in target-date funds.

Target Date Funds vs Index Funds: Asset Categories

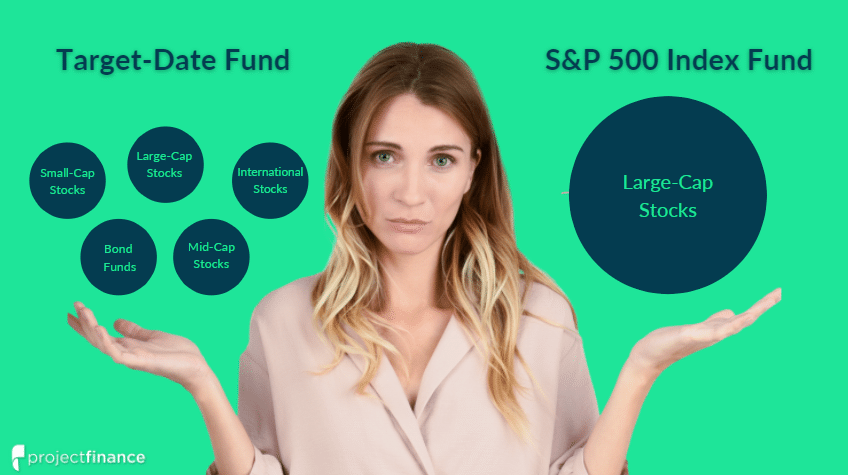

S&P 500 index-tracking ETFs and mutual funds provide exposure to the 500 largest companies listed on stock exchanges in the United States. All of these companies fall under the “large cap” umbrella.

Target-date retirement funds also invest in large-caps, while adding:

Small-cap equities

Mid-cap equities

International equities

Bonds

Let’s next break down a few of these asset classes target-date funds invest in.

Target-Date Funds: Bond Exposure

We are taught from a young age that diversification is the best way to go in investing. That includes investing in both bonds AND stocks. But we are not living in our parents’ age, nor our grandparent’s age.

In 2022, interest rates are rising, but many financial professionals believe rates will never again rise to the heights of previous decades.

Over the course of a few decades, having 15% of your portfolio producing relatively poor returns may be ballast on your retirement plans.

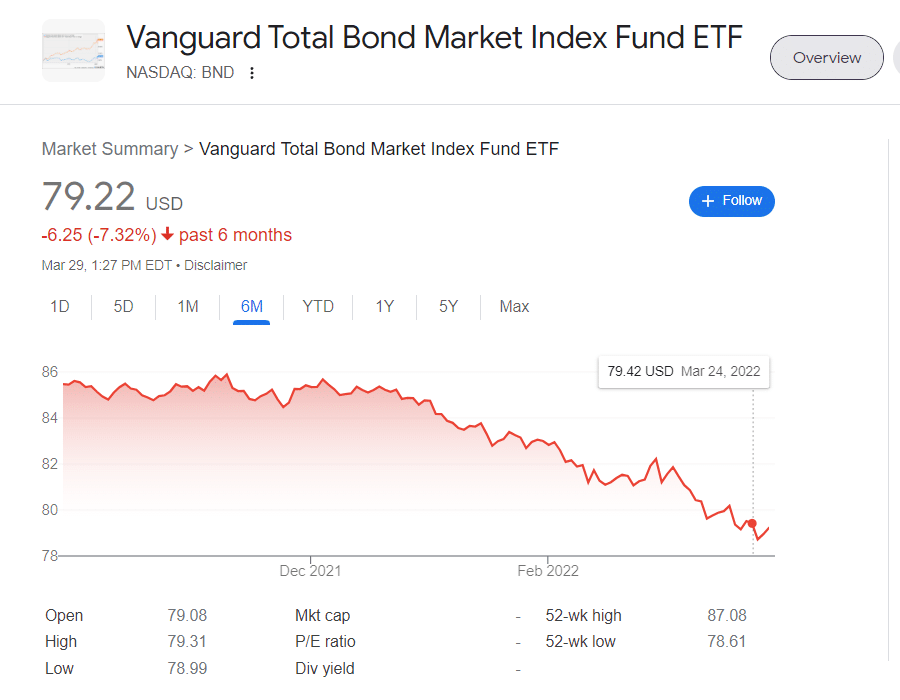

Additionally, bonds have taken a considerable hit this year. In the first four months of 2022, Vanguard’s Total Bond Market Index Fund ETF Shares (BND) has fallen over 4%. Quite volatile indeed for a historically “safe” asset class!

Though bonds have indeed been underperforming, it is important to note that bonds provide investors a great source of retirement income.

BND 6 Month Performance

Target-Date Funds: International Exposure

➥ S&P 500 ETFs and mutual funds invest only in American companies.

➥Target-Date Funds invest in stocks from all over the world.

Let’s get right into comparing the historical performance of American stocks with international stocks:

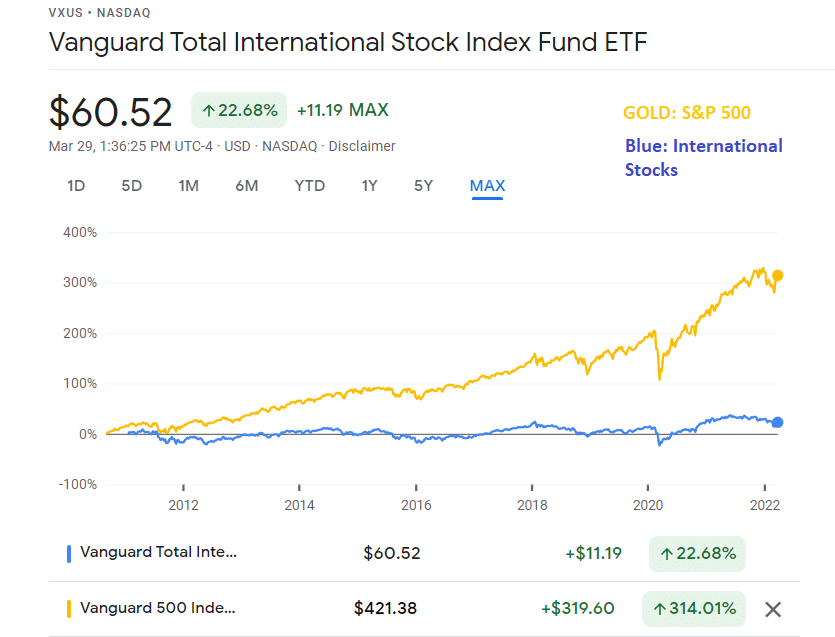

International vs Domestic Stocks: 11 Years

Over the past 11 years, the S&P 500 (as represented by VOO in gold) has returned 314%. During this same time, international stocks have returned 22.68% (as represented by Vanguard’s Total International Stock ETF (VXUS).

Does this mean international stocks are poised for a comeback? Perhaps. But for the past 11 years, international stocks have barely kept up with inflation. For me, that’s a red flag for what’s to come.

Now that we have an idea of the different types of assets and securities that comprise target-date funds, let now compare them with S&P 500 index funds.

New to options trading? Learn the essential concepts of options trading with our FREE 160+ page Options Trading for Beginners PDF.

All Vanguard target-date funds have this monster within them. This is where we are going to see overlap with S&P 500 index funds.

In addition to containing all S&P 500 stocks, VSMPX adds small-, mid-, and large-cap growth and value stocks.

Since this fund has a target-date only 8 years away, VTHRX (2030 target-date) is very conservative, having 35% of its holdings in bonds.

So how does this fund stack up against the S&P 500?

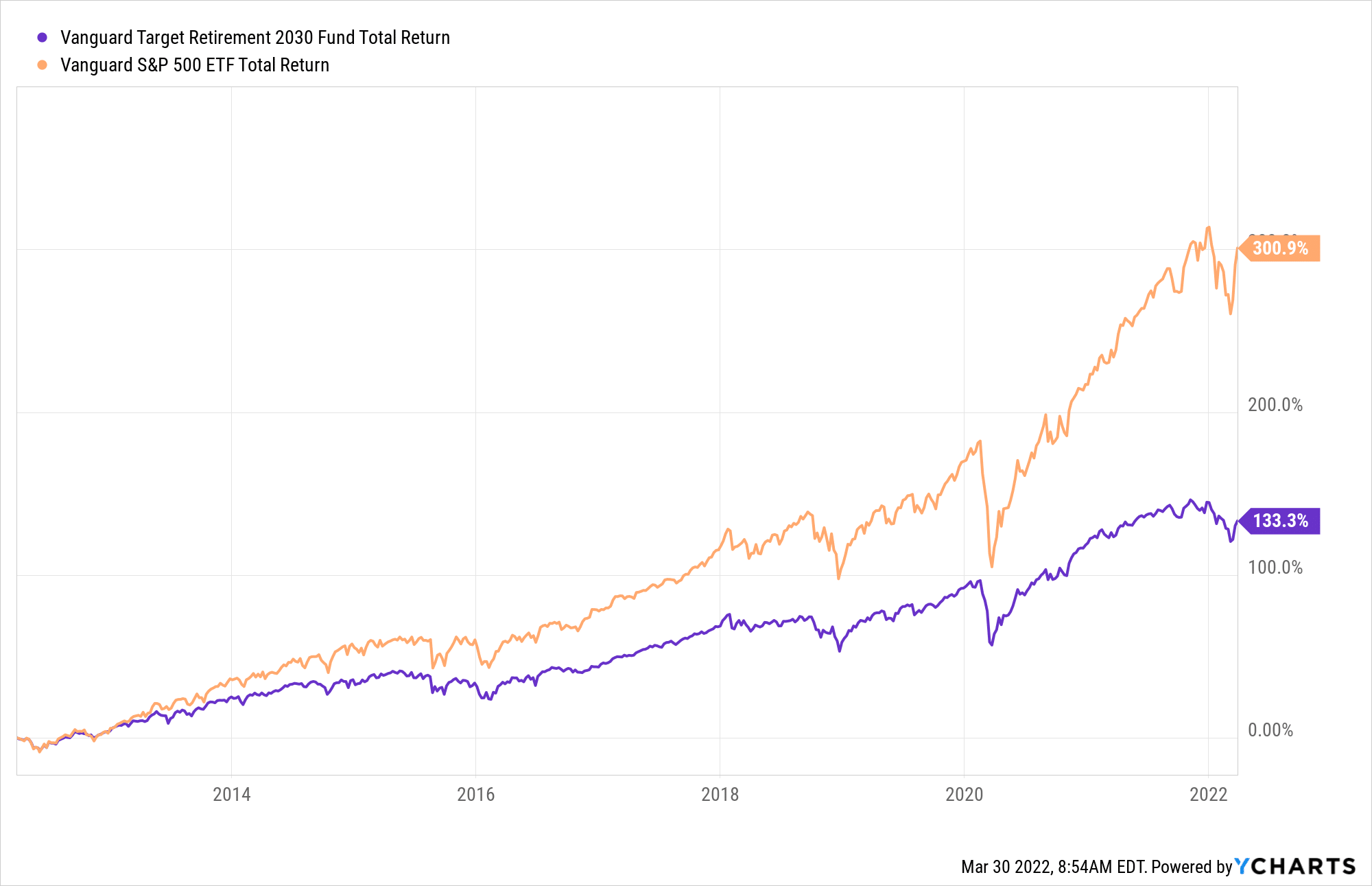

VTHRX vs VOO: 10 Year Total Total Return

As we can see, the S&P 500 has vastly outperformed Vanguard’s 2030 target-date retirement fund during the past 10 years.

Of course, this is to be expected given the planned retirement date for this investor is only 8 years away. As target-date retirement funds approach their specified date, the funds become more conservative and (in bullish markets) generally underperform the S&P 500.

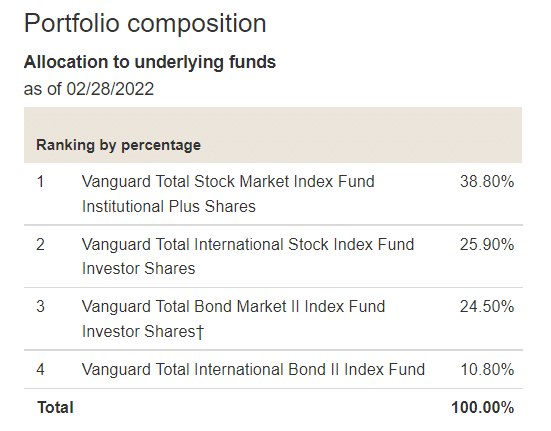

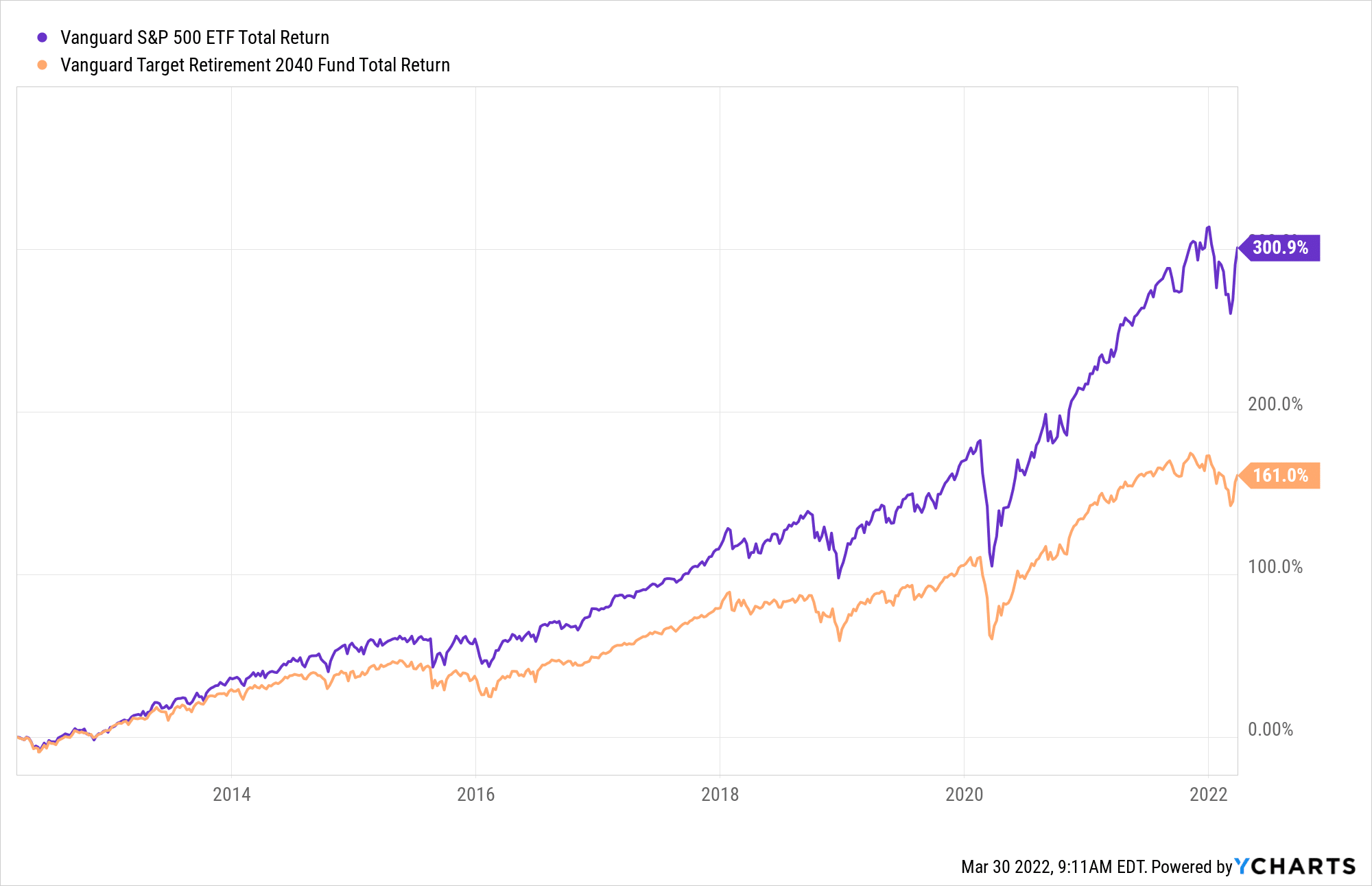

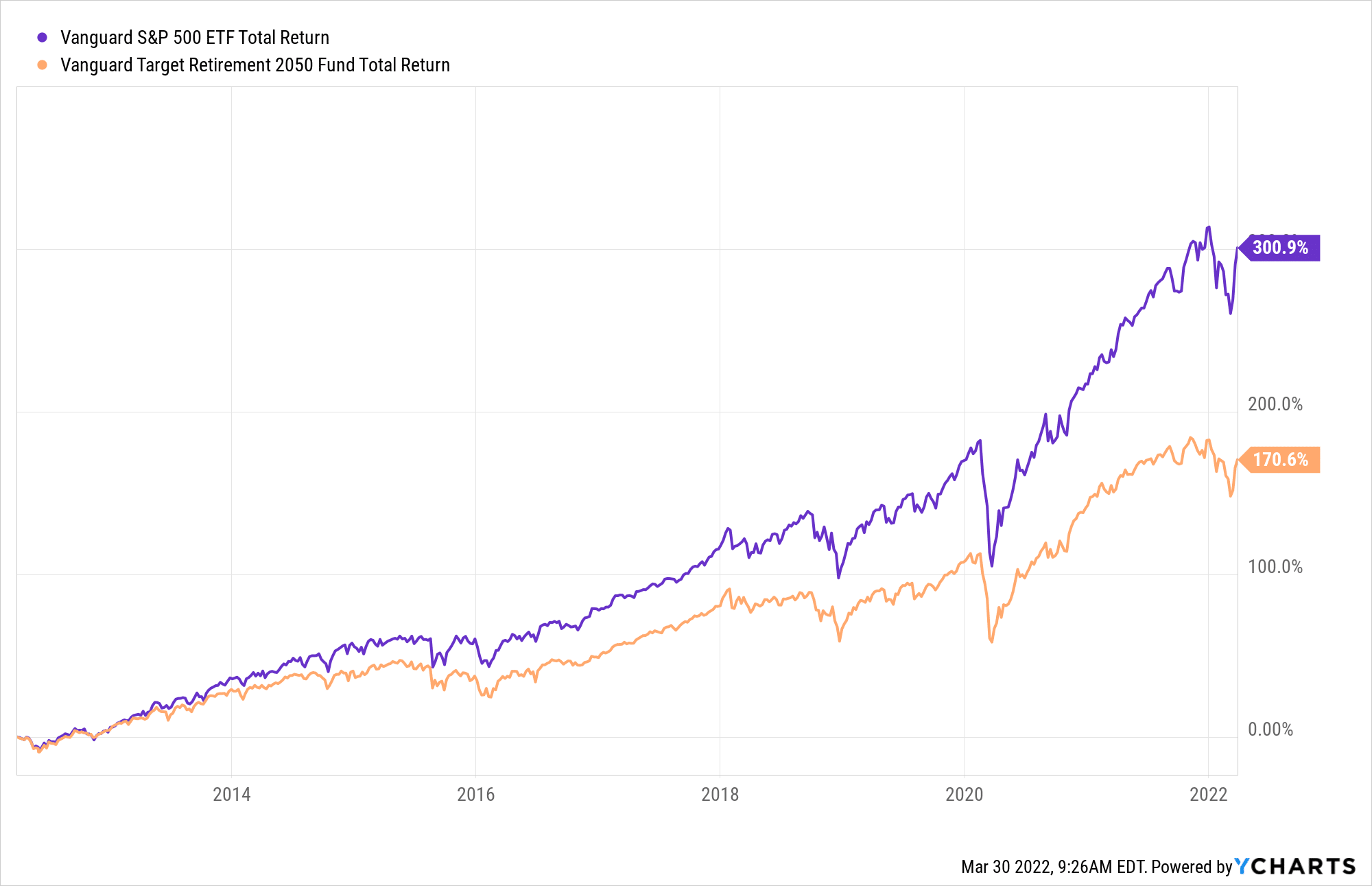

As we can see, Vanguard’s 2040 fund is a little less conservative than its 2030 fund, having about 20% of its assets invested in bond funds.

Additionally, this fund has an international equity exposure of 32%, compared to the 2030s international equity exposure of 26%.

So how has this slightly more aggressive fund performed over the last ten years in relation to the S&P 500 (as represented by Vanguard’s VOO S&P 500 ETF)?

VFORX vs VOO: 10 Year Total Return

Because of this fund’s slightly higher equity exposure, it has performed slightly better than the 2030 retirement fund over the past decade. However, the fund still pales in comparison to the S&P 500.

Warning!Most financial professionals agree target-date funds are a great way for less market savvy investor's to save for retirement. The DIY yourself approach can prove to be a costly endeavor if not conducted with diligence and financial aptitude.

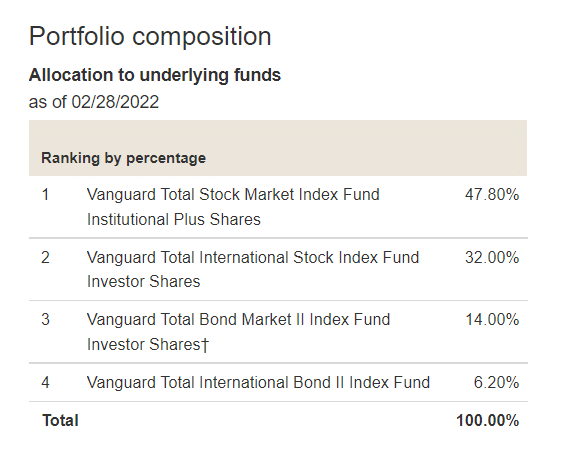

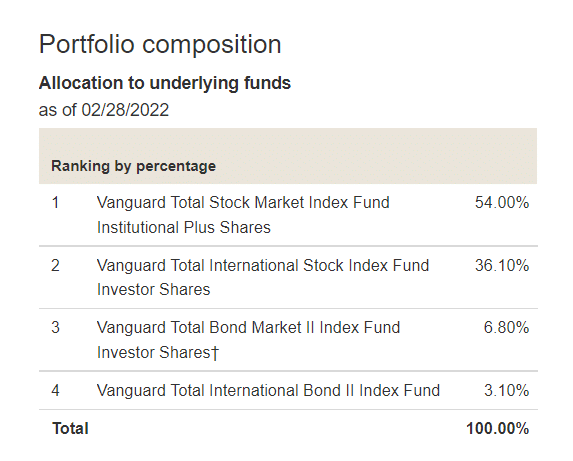

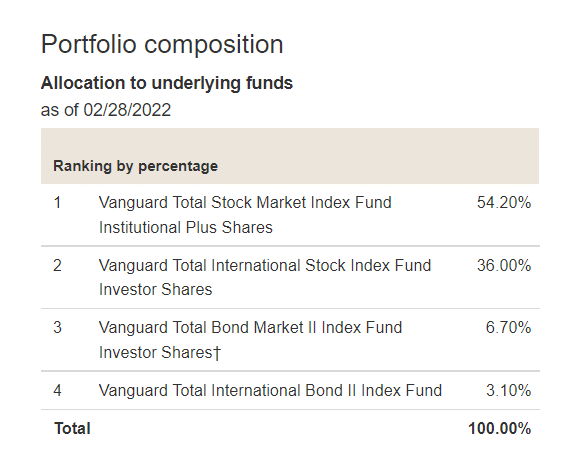

Relative to Vanguard’s 2040 fund, Vanguard’s 2050 target-date fund reduces its bond exposure to 10% while increasing its international equity exposure to 36%. Additionally, its US equity exposure has increased by 6%.

So how has this more aggressive fund stacked up to the S&P 500 over the past decade?

VFIFX vs VOO: 10 Year Total Total Return

As expected, due to its more aggressive nature, VFIFX outperforms the 2030 and 2040 funds. However, when comparing VFIFX to the S&P 500, we can see it has vastly underperformed.

This fund currently has over 90% of its holdings in equities and less than 10% in bonds.

So how has this fund performed in relation to the S&P 500?

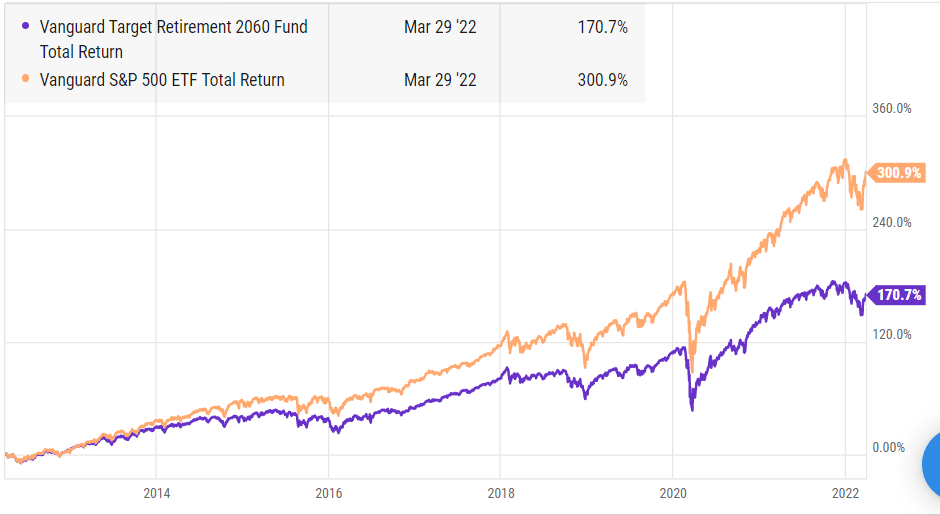

VTTSX vs VOO: 10 Year Total Return

The further away a target date becomes, the more Vanguard target-date funds begin to mirror one other.

Vanguard’s 2060 fund is almost an exact replica of its 2050 fund.

They both have ≈ 54% of their holdings in US stocks, ≈36% in international stocks, and ≈10% in bond funds.

The ten-year performance of the 2050 and 2060 fund is therefore almost identical.

However, when compared to the S&P 500 – again – they both underperform quite dramatically.

Target-Date Funds vs S&P 500: Which Is Right for You?

Target-date funds get a lot of things right (they produce a phenomenal diversified portfolio for individual retirement accounts) – but they get a lot of things wrong as well:

Target-date funds do not take into consideration investments held outside the fund.

Target-date funds assume all investors have the same risk tolerance.

Target-date funds do not adapt to the ever-changing financial needs of investors.

Many financial professionals believe retirement savers should have more equity exposure than target-date funds offer.

Let’s focus for a moment on the fourth item on the list.

Perhaps this approach is too aggressive, but investors do not need to choose one or the other.

A great investment portfolio strategy (particularly for traditional and Roth IRAs) is to keep a portion of your retirement savings in target-date funds while managing the remaining funds on your own. This will allow you to reach the bond/equity ratio that best suits your individual risk tolerance. This approach will also allow you to invest in more asset classes, such as real estate funds.

Additionally, having the bulk of your funds in a target-date fund will help shield you from market volatility.

In bull markets, index funds that track the S&P 500 tend to outperform target-date funds. However, during times of high volatility, equity index funds will generally lose more in value than target-date funds, which are more conservative.

Many investment professionals believe that target-date funds do not provide enough equity exposure. Investors must understand their own risk tolerance before determining if target-date funds are too conservative (or too aggressive).

Target-date funds are very diverse products that change and grow with investors risk appetites’ (which decreases with age); index funds are static and do not adjust over time to meet investors changing needs.

Mike was a writer for projectfinance. He has spent over 15 years in the finance industry, working for such companies as thinkorswim, TD Ameritrade and Charles Schwab. His work has appeared in the Financial Times, the Chicago Sun-Times, and The Buffalo News.

Share this post

2 thoughts on “Target-Date Funds vs S&P 500 Index Funds: Which is Better?”

What about combining target-date funds with an S&P 500 index tracker in a 401k?

Hey Andres! That depends on your time horizon. If you’re bullish on the American economy and have a long time horizon, putting a nice chunk into an S&P 500 tracking fund may help supplement those bonds and intl stocks weighing down your target-date fund! Of course, this all depends on the long-term performance of the S&P 500!

")

(1)")

2 thoughts on “Target-Date Funds vs S&P 500 Index Funds: Which is Better?”

What about combining target-date funds with an S&P 500 index tracker in a 401k?

Hey Andres! That depends on your time horizon. If you’re bullish on the American economy and have a long time horizon, putting a nice chunk into an S&P 500 tracking fund may help supplement those bonds and intl stocks weighing down your target-date fund! Of course, this all depends on the long-term performance of the S&P 500!