Search

About

Blog

Contact

About

Blog

Contact

Search

Watch on YouTube

Category: Retirement

Retirement

How to Calculate Your Roth IRA and 401k Paychecks

Read More »

April 25, 2022

Retirement

FAQ: How Much Cash Should Retirees Keep on Hand?

Read More »

April 14, 2022

Retirement

Can You Contribute to Multiple 401(k) Accounts Simultaneously?

Read More »

April 13, 2022

Retirement

FAQ: Can You Cash Out a Life Insurance Policy for Retirement?

Read More »

April 6, 2022

Retirement

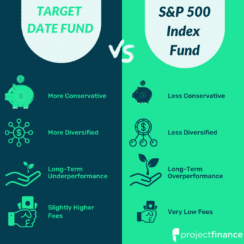

Target-Date Funds vs S&P 500 Index Funds: Which is Better?

Read More »

April 19, 2022

Retirement

The Pros and Cons of a SEP-IRA for Retirement

Read More »

March 30, 2022

Investing

What’s the Best Stock to Bond Ratio for Your Age?

Read More »

April 19, 2022

Retirement

7 Great ETFs for Your Roth Retirement Account in 2022

Read More »

February 23, 2022