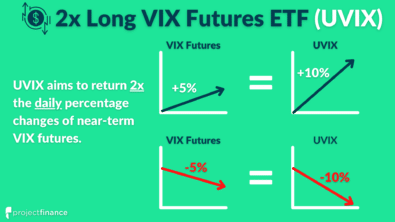

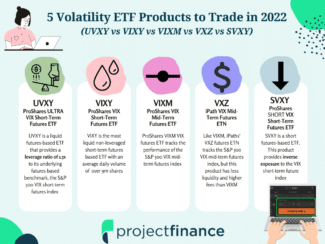

Investing VXX Alternatives: UVXY vs VIXY vs VIXM vs VXZ vs SVXY vs UVIX vs SVUX Read More » April 1, 2022