The Cboe VIX Index measures prices of 30-day option prices (implied volatility) on the S&P 500 Index. Since option prices are an indicator of fear or complacency in the marketplace, the VIX is sometimes viewed as a “fear index” that gauges the level of uncertainty in market participants.

As mentioned in our guide on the VIX Index, the VIX cannot be traded directly, but there are products that allow traders to gain exposure to changes in the VIX Index. VIX futures are one of the products available when trading volatility.

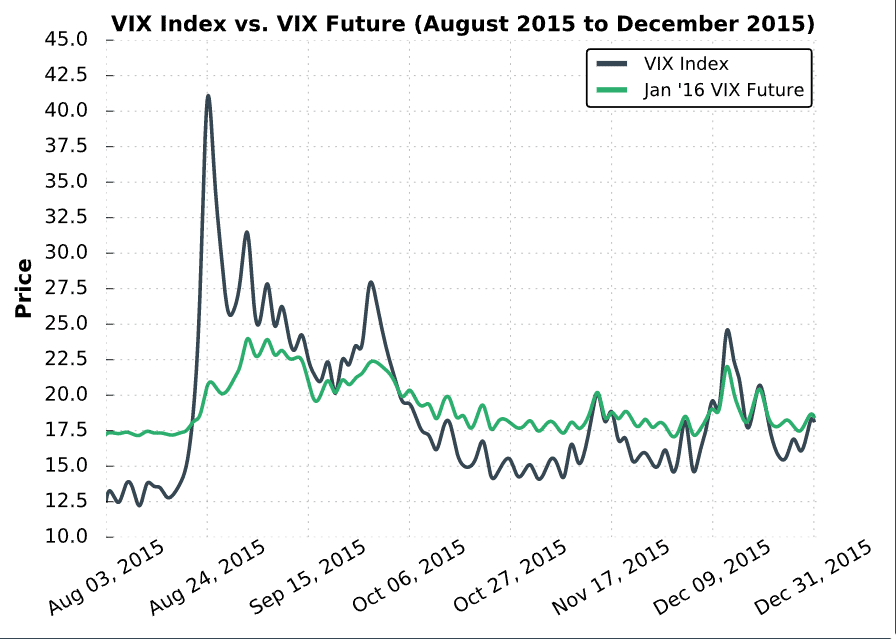

The following visual demonstrates how a future on the VIX can change relative to the VIX Index:

As we can see here, the price of the VIX futures contract changes in the same direction as the VIX Index, but not by the same amount in this case (we’ll discuss this in-depth shortly).

When holding VIX futures contracts, traders are exposed to profits or losses as the contract converges to the VIX Index.

When the VIX is low, the futures contracts tend to be priced higher than the index (referred to as contango). As time passes, the futures contracts will decay in price towards the VIX Index if the VIX doesn’t increase.

The following visual illustrates the concept of decaying volatility futures contracts as time passes (the dashed lines represent the settlement dates for each respective contract):

Data from Cboe’s Historical VIX Futures Data

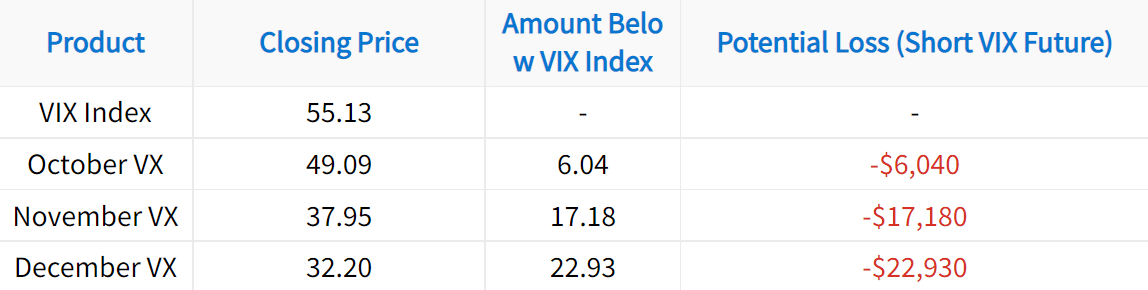

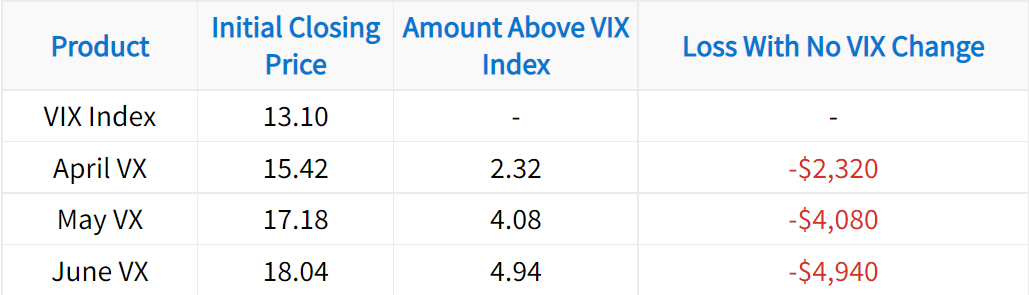

At the beginning of the period, each product had the following price and potential loss from purchasing the contract:

When the VIX is abnormally high, the futures contracts tend to be priced lower than the index (referred to as backwardation). As time passes, the futures contracts will increase in price towards the VIX Index if the VIX doesn’t decrease.

The following visual illustrates the concept of increasing volatility futures contracts as time passes:

Data from CBOE’s Historical VIX Futures Data

As we can see here, when the VIX Index surges, the prices of VIX futures tend to trade at lower prices than the index because the market doesn’t expect the VIX to stay at such elevated levels for long. In this scenario, carrying costs are transferred to the sellers of VIX futures, as increasing contract prices lead to losses for sellers. As an example, let’s look at the closing prices of each product on October 14th, 2008: