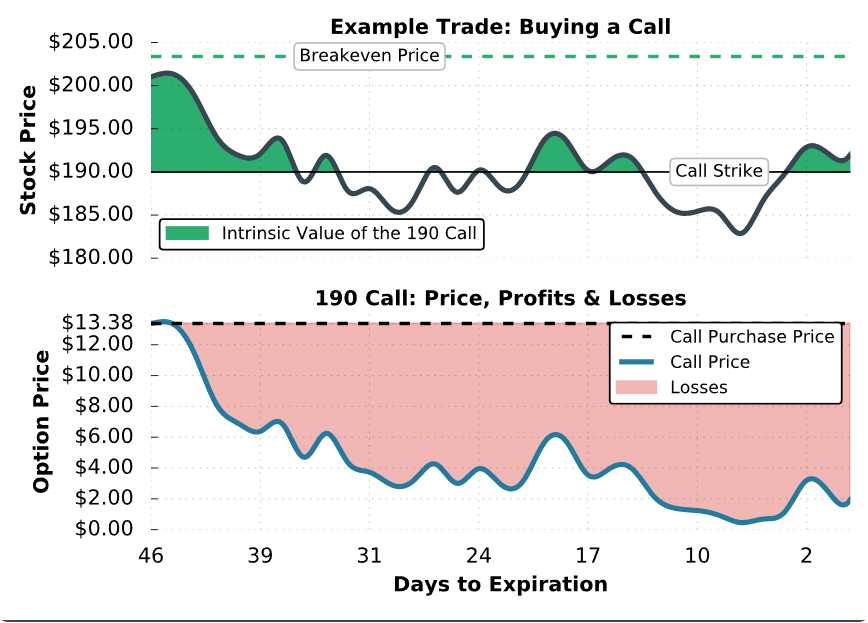

With an initial delta of +0.75, the 190 call option was expected to lose $0.75 for each $1 decrease in the stock price, which explains why the position performed so poorly when the stock price fell from $201 to $185. Over the same period, implied volatility increased from 21% to 28%. Unfortunately, that wasn’t enough to offset the losses from the decrease in the stock price.

From a probabilistic perspective, the decline in the call option’s price makes sense. With the stock price at $200, the probability of the 190 call expiring in-the-money was approximately 75% (based on a delta of 0.75). However, as the stock price fell to $185, the 190 call’s price fell because the likelihood of expiring in-the-money diminished.

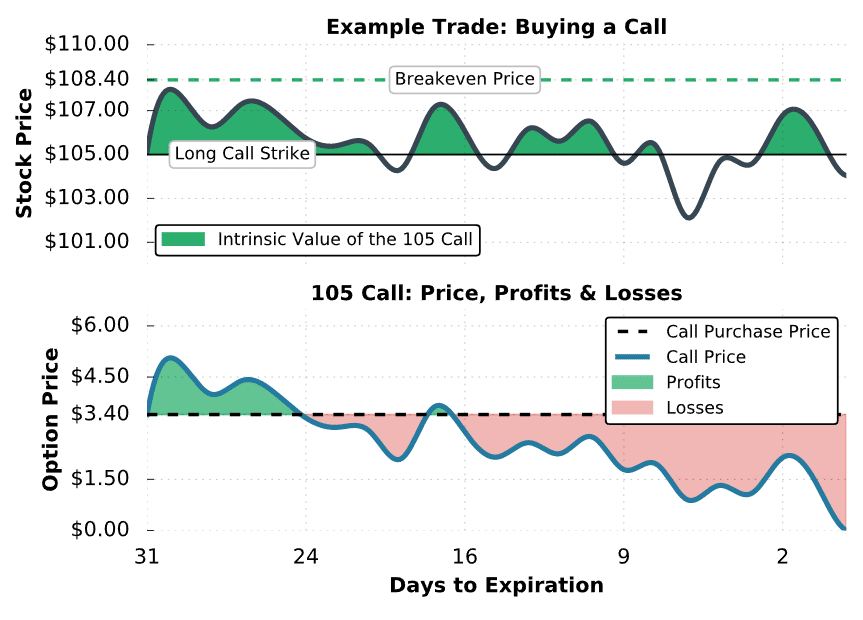

As mentioned previously, a call option can always be closed before expiration. As an example, let’s say the trader in this example wanted to cut their losses when the call traded down to $10. If the trader sold the call for $10, they would have locked in losses of $338: ($10 sale price – $13.38 purchase price) x 100 = -$338.

At expiration, the stock was trading around $192, and the 190 call was worth its intrinsic value of $2.00. With an initial purchase price of $13.38, the resulting loss is $1,138 per contract for the call buyer. If the trader held the call through expiration, the resulting position would be +100 shares of stock per contract. The effective purchase price of these shares would be $203.38, which is the call’s strike price of $190 plus the $13.38 purchase price of the option.

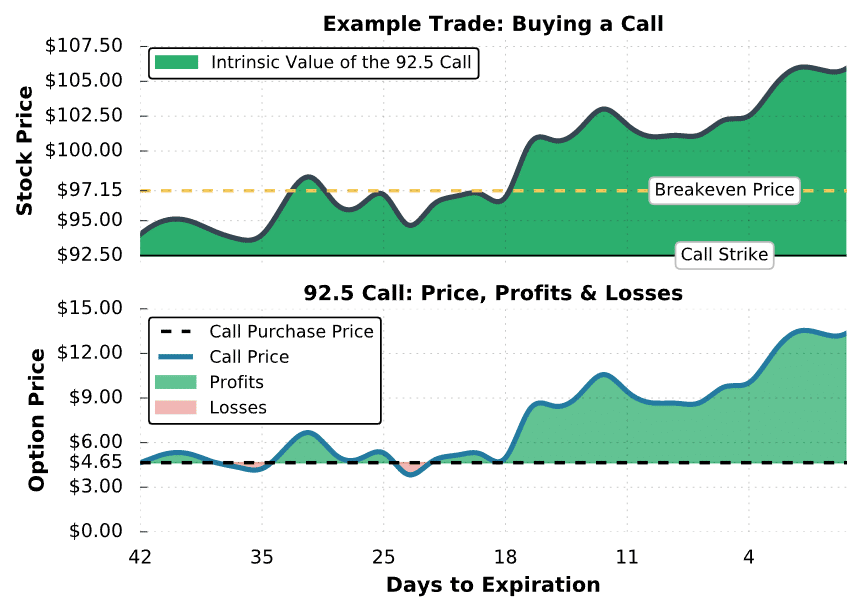

Alright, you’ve seen what can go wrong when buying calls. Let’s finish by investigating what needs to happen to profit when buying call options.