Last updated on February 11th, 2022 , 12:14 pm

Highlights

The “Greeks” help traders predict how options will respond to various market changes in the underlying

Delta and gamma predict option price movement in response to changes in the underlying price

Theta tells traders how much extrinsic value an option will shed after one day, with all other conditions remaining constant

Vega predicts how an options price will respond to changes in implied volatility

Most trading platforms can be laid out to include the Greeks

Table of Contents

There are few things more daunting to the amateur options trader than the series of complex mathematical equations dubbed the Greeks. Just trying to wrap your head around these risk-management equations is panic-inducing. However, if you want to become a serious options trader, you must understand them.

The good news? You do not need an advanced degree from MIT to equate and understand these helpful market measures. On almost all trading platforms, the computations are done for us. All we need to do is interpret their meanings, which we will accomplish in this article.

Today we will focus on the big four Greeks: delta, gamma, theta, and vega.

Delta and gamma work together, measuring how options respond to changes in the underlying price. Theta tells us how much an option changes in response to the passage of time. Lastly, vega tells us how sensitive an option is to changes in the implied volatility of the underlying.

Possessing a basic understanding of these absolutely vital risk-management tools will surely pay your portfolio dividends in the future. Let’s get started!

The Option Greeks and Time

Perhaps the most important thing to know about the Greeks is that they are forward-looking. Think of them as little-time travelers, peering into the future and reporting back to you what could happen under various circumstances.

The most effective education happens when the student wants to learn. Therefore, before we continue, let’s plant that seed.

If you’ve ever been long a call option, haven’t you wondered why that option reacts the way it does to changes in stock price?

I have talked to many long-call holders on the phone who were a little more than discouraged to discover their option didn’t rise in value as much as they thought it would when the underlying stock rallied.

If only there was a way to tell ahead of time what would happen to an options price if the stock shot up by a dollar…oh, but there is!

(1)")

New to options trading? Learn the essential concepts of options trading with our FREE 160+ page Options Trading for Beginners PDF.

1. Option Delta Explained

Enter delta. The delta of an option tells us how an option will react to a change in stock price before that price change happens. Pretty cool, right?

Δ Option Delta Definition: In mathematics, an uppercase delta represents the change in a quantity. In options trading, the delta of a position is expressed as a ratio of change. This ratio tells us how much an options position is expected to change in value with a corresponding $1 move in the underlying security.

Option Delta in Calls and Puts

The value of an options delta will depend on the type of option:

- All call options will have a delta value between 0 and +1.

- All put options will have a delta value between 0 and -1.

Why is the delta negative for put options? Put options have an inverse relationship with a stock price; when the stock goes up, the value of the put goes down.

The delta of an option simply tells us how the price of an option will change if the underlying stock price were to immediately rise or fall by a dollar.

If you were long a call, and that call had a delta of 0.34, that option would increase in value by 34 cents if the underlying stock were to go up a dollar. Conversely, the option would fall by 34 cents if the underlying stock fell by a dollar.

Pretty simple stuff, right? Things can get a bit more complicated when you get into delta hedging, but we’ll save that for another lesson.

Let’s look at an example now on a truncated options chain.

AAPL Option Delta Example

| Type | Strike | Price | Delta | +$1 Share Price Affect | -$1 Share Price Affect |

|---|---|---|---|---|---|

|

Call |

147 |

3.25 |

.64 |

3.89 |

2.61 |

|

Call |

148 |

2.63 |

.52 |

3.15 |

2.11 |

|

Call |

149 |

2.11 |

.42 |

2.60 |

1.62 |

Where AAPL is trading at $148.20

The above options chain shows us how an increase/decrease in the price of Apple (AAPL) by $1 affects various option prices after contributing for delta.

If you want to determine how much an option will increase or decrease in response to a $1 move in the underlying, just add/subtract the delta from the option’s current price. Voila. That’s it.

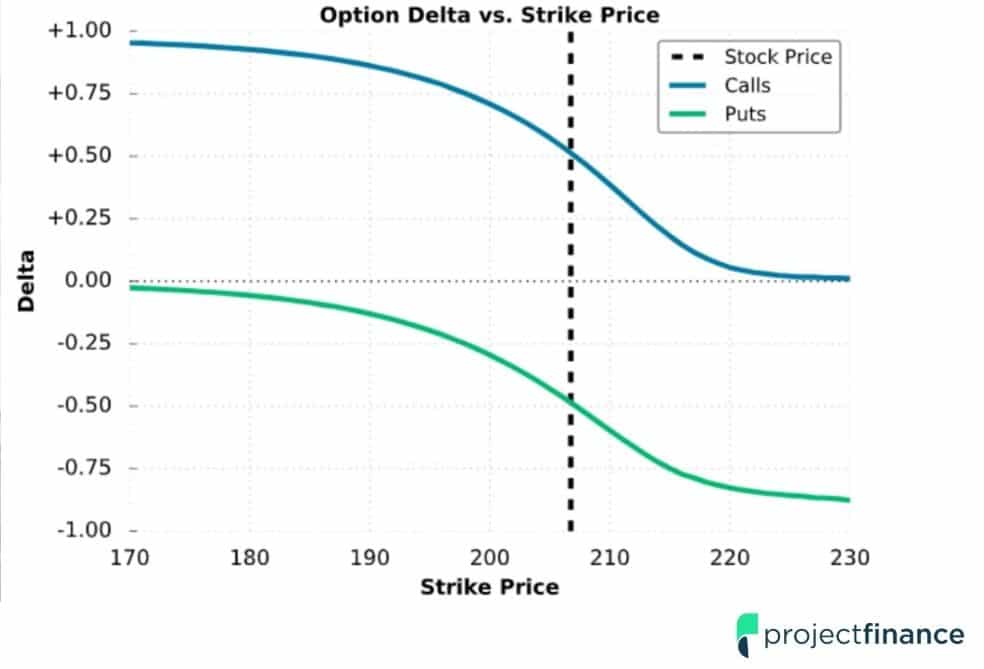

Delta and Moneyness

In the above table, AAPL stock is trading at $148.20. That means that the 147 call is in-the-money, the 148 call is (pretty close to) at-the-money and the 149 call is out-of-the-money.

We can see the 147 call has the highest delta. The delta of in-the-money call options approaches a positive 1 as expiration nears.

The 149 call has the lowest delta. The delta of out-of-the-money calls approaches zero as expirations near.

At-the-money-options (the 148 call) tend to have a delta of around 0.50 over their life. Ultimately, just about all options will close in or out-of-the-money.

The further we go out-of-the-money, the less effect stock price movement has on our options delta. If you’re long options, decreasing delta is bad news. However, if you’re short options, low deltas are a good thing.

Before we move on, take a moment to study the below graph, which shows the relationship between option delta and strike price (the dashed vertical line represents the current stock price, which is also where at-the-money options reside).

Delta vs Strike Price

Delta and Moneyness Odds

Delta has another function; it also tells us the odds an option has of expiring in-the-money.

Take a look at the 149 call in our AAPL option chain above. The delta for this option is 0.42. In addition to telling us this option will increase in value by 0.42 if the stock were to go up by a dollar, it also represents the odds that an option has of expiring in-the-money.

The 149 call has a 42% chance of being in-the-money at expiration. The 148 call has a 52% chance of expiring in-the-money.

Bear in mind these numbers are in constant flux with the underlying.

How Delta Mimics Shares of Stock

We’re not quite done with delta yet. I hope you’re beginning to see why it is the first Greek on this list! It is the most important by far.

The delta of a position can also tell us “how many” shares of stock an option trades like. If our delta is 0.20, our option will mimic the profit/loss on approximately 20 shares of stock. If an option has a delta of 1 (as many deep-in-the-money options have) that option will trade like 100 shares of stock.

Option Delta Summary

Before we move on to our next Greek, let’s sum up all we’ve learned about delta.

- The delta of an options position tells us how much the value of that particular option will fluctuate with a corresponding $1 move in the stock price.

- The delta of an option represents the odds that a particular option has of expiring in the money. A delta of 0.30 has a thirty percent chance of expiring in-the-money.

- Delta also tells us how many shares of stock our option “trades like”. In a profit/loss profile, a delta of +0.50 will trade similar to 50 shares of the underlying security.

To learn more about delta, please check out our video below!

2. Option Gamma Explained

Gamma takes a look at delta and then goes a step further. You can’t understand gamma without first understanding delta, so make sure you have a solid grasp of the concepts in our first Greek before moving on.

(Γ) Option Gamma Definition: In options trading, the Greek “gamma” measures the rate at which an options delta changes in correspondence to the price of the underlying security.

We learned earlier that the delta of an option is in constant flux with the market. If you watch the Greeks on your trading software, you’ll see they change just as frequently as the stock changes. Where do we find our footing?

Gamma steps in here and tells us how the future delta of an option will change in response to a one-point move in the underlying stock.

Sound confusing? We’ll clear the air in a moment with an example. First, let’s understand a few key concepts about gamma.

1.) Long Options Yield Positive Gamma; Short Options Yield Negative Gamma

We learned before that the delta of most put options has a negative value, whereas the delta of most call options has a positive value.

This changes for gamma. Regardless of the option type (call or put), long options always yield a positive gamma. Short options, however, will always yield a negative gamma.

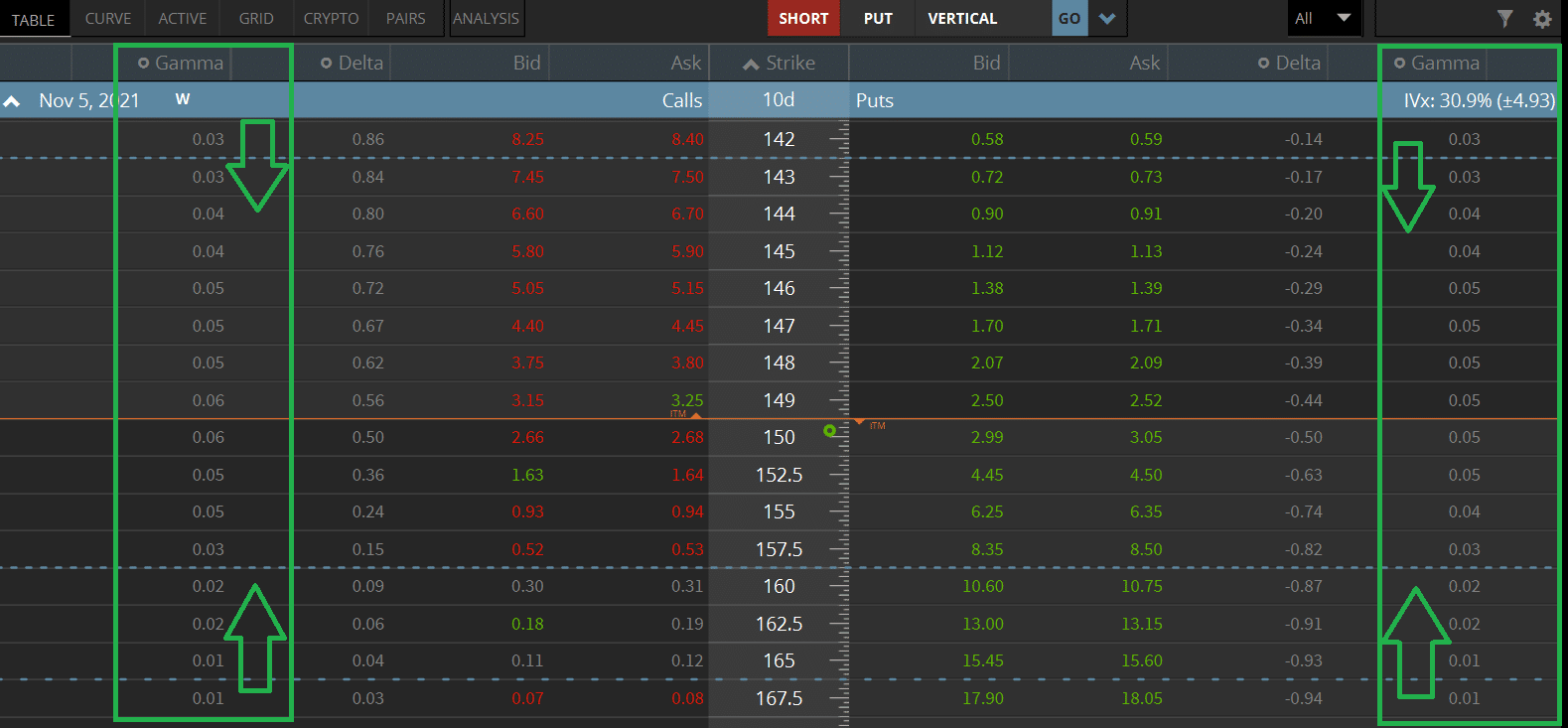

2.) At-the-Money-Options Yield the Highest Gamma

The further in-the-money an option is, the higher its delta is. This is not true for gamma. Gamma yields are highest for at-the-money options.

Why is this? The deltas of at-the-money options are most sensitive to stock price changes. The below screenshot (taken from the tastyworks software) illustrates how high gamma gravitates towards at-the-money options.

AAPL Option Gamma Example

| Type | Strike | Price | Delta | Gamma | New Delta (+$1 Share Price ) | New Delta (-$1 Share Price) |

|---|---|---|---|---|---|---|

|

Call |

147 |

3.25 |

.64 |

.06 |

.70 |

.58 |

|

Call |

148 |

2.63 |

.52 |

.08 |

.60 |

.44 |

|

Call |

149 |

2.11 |

.42 |

.06 |

.48 |

.36 |

Where AAPL is trading at $148.20

The furthest right two columns in the above table illustrate how an options delta will react to a +/−$1 change in the underlying stock. This is calculated by either adding or subtracting gamma to/from the previous delta.

For a stock increase, we simply add the gamma to the old delta to determine the new delta. For a stock decrease, we subtract the gamma from the delta.

You will notice that the gamma for the 148 call (the at-the-money call) is higher than the other gammas.

As we said earlier, deltas are most sensitive when at-the-money. Since gamma is a derivative of delta, these moneyness structures are most reactionary to stock price changes.

If delta is thought of as the speed at which an option moves, gamma can be thought of as the acceleration of this speed.

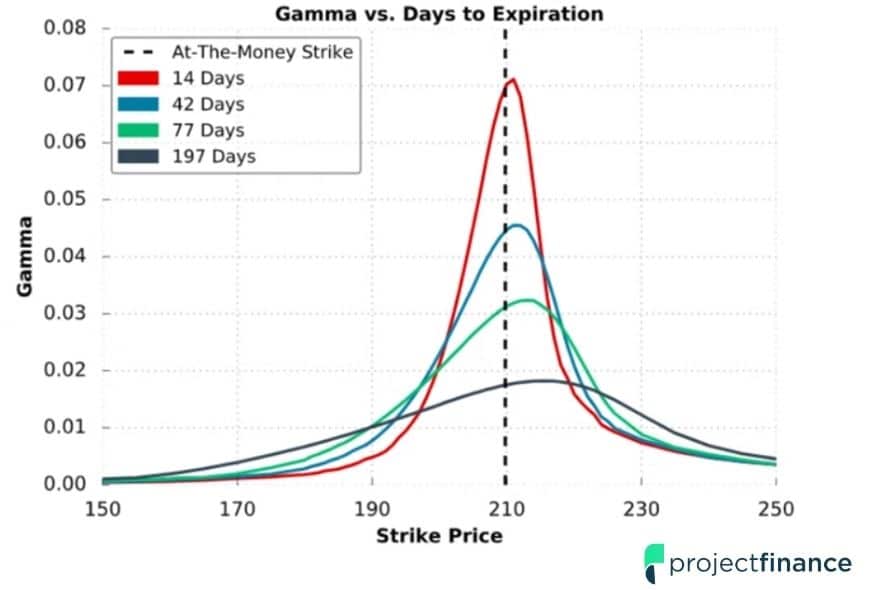

Option Gamma vs Days to Expiration

So far, we have looked at how gamma affects the options of a single, near-term expiration cycle. But what affect would time have on the gamma of options expiring in 30 days rather than 3?

Gamma is always greatest for near-term options. The further away an option is from expiration, the less the gamma will be. Take a look at the below graph to get a better understanding of how time affects gamma.

Gamma vs DTE

Option Gamma in Long and Short Options

Short option sellers do not want their position to be in-the-money at expiration. Since gamma is highest for at-the-money options, we can therefore deduce that high gamma is bad news for short option positions.

On the other hand, long option positions profit when the delta approaches 1. Therefore, high gamma is desirable for these positions.

To learn more about gamma, please check out our video below!

3. Option Theta Explained

Our next Greek pertains to something almost all beginner options traders learn the hard way: time decay.

Unlike stock, all options have an expiration date. If an option is out-of-the-money when it expires, its value will be zero.

In an environment where implied volatility and stock price remain constant, an out-of-the-money options contract will perpetually shed its extrinsic value (which is the only value out-of-the-money options have) as expiration nears. The option Greek theta tells us the rate at which this decay will happen.

(Θ) Option Theta Definition: The rate of decline in the value of an option attributed to a one-day change in the time to expiration.

Before we jump into theta, it may be helpful to understand the difference between “intrinsic” and “extrinsic” value in options trading. If you’re already familiar with this, please skip ahead!

Option Theta: Intrinsic and Extrinsic Value

The price of all options consists of intrinsic and/or extrinsic value.

Intrinsic Value Definition: In options trading, intrinsic value represents the value of an option should that option be exercised at the moment of observation.

Extrinsic Value Definition: In options trading, extrinsic value represents all option value that is not intrinsic value.

The intrinsic value of an option is simply the amount that option is in-the-money by. Extrinsic value is everything that is left over. Time and implied volatility play a part in determining an option’s extrinsic value. As time passes, and an option remains out of the money, its extrinsic value will shed. If an option is out-of-the-money on expiration, its value will be zero.

Let’s look at an example.

AAPL Call Option Example

Stock Price: $150

Call Strike Price: 149

Call Option Price: $3

Extrinsic Value: $2

Intrinsic Value $1

Since our above call option is in-the-money by $1, its intrinsic value is $1. The price of the option, however, is $3. Therefore the remaining $2 must be the option’s intrinsic value.

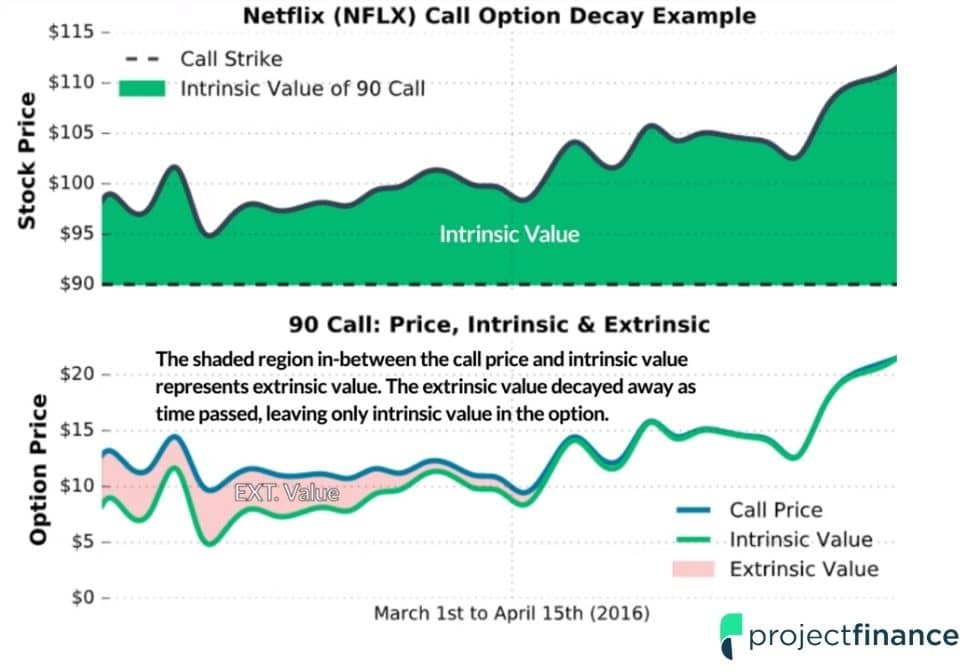

Like the Greeks, intrinsic and extrinsic values are in constant flux with the market. Check out the below graph, which shows how the different values which comprise a NFLX call option change as time passes and the underlying stock price changes.

NFLX Time Decay

Option Theta and Extrinsic Value

Theta is concerned with extrinsic value. This Greek tells us how much “extrinsic value” an option is expected to lose with each passing day. In an environment where the stock price and implied volatility remain constant, time decay causes an option to lose value.

Think about this intuitively. Let’s say a stock is trading at $130/share. You buy the 135 strike price call for 0.40 that expires in thirty days. If 29 days pass and the stock is still trading at $130, won’t your option decline in value? It’ll probably be worth a few pennies if anything. Theta tells us how fast this decay occurs – on a daily basis.

Option Theta in Calls and Puts

Theta is kryptonite for long option positions. If we’re long an option, theta causes it to shed value perpetually. This is particularly detrimental for long out-of-the-money options. Why? These options are comprised completely of extrinsic value. In-the-money-options still have intrinsic value, which is unaffected by the passage of time.

Short option positions, however, love theta. With each passing day, in a constant environment, theta chips away at premium, making a short call or put position more profitable.

For both calls and puts, theta is expressed as a negative value. Like gamma, theta is typically highest for at-the-money options.

AAPL Option Theta Example

| Type | Strike | Price | Theta |

|---|---|---|---|

|

Call |

147 |

3.25 |

-.52 |

|

Call |

148 |

2.63 |

-.56 |

|

Call |

149 |

2.11 |

-.54 |

Where AAPL is trading at $148.20 and expiration 2 days away.

At this point, determining theta should be relatively easy for you. Look at the above options chain, the options of which expire in 2 days.

With these options so near the end of their life, theta is going to be high. If by tomorrow the stock/implied volatility hasn’t changed, the 148 call (at-the-money) will be trading at 2.07 (Option Price 2.63 – Theta .56).

Why such a dramatic change in price? As we said, the option is expiring in 2 days. If we were to look at the theta of an option with a different expiration (30 days to expiration) but the same strike price, the theta will be only -.06.

As the expiration on an option nears, theta accelerates.

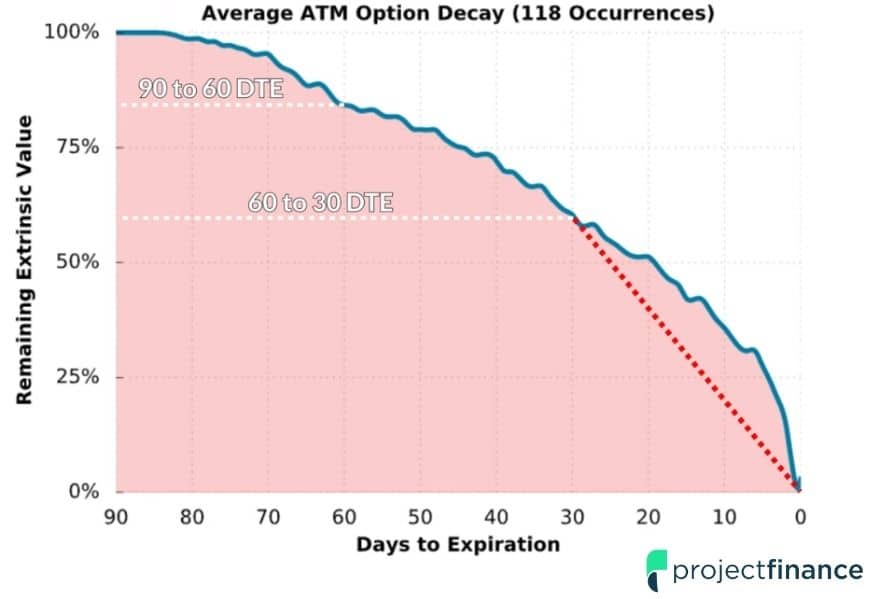

Take a moment to study the below image, which shows just how detrimental time can be to the extrinsic value of an at-the-money option over a duration of 90 days.

Time Decay Over 90 days

Option Theta Summary

Before we move on, let’s review a few highlights from theta. After delta, this is the most important Greek.

- Theta is typically expressed as a negative value

- Theta is highest for at-the-money options

- In an environment of constant stock price and implied volatility, theta will perpetually eat away at an options extrinsic value

To learn more about theta, please check out our video below!

New to options trading? Learn the essential concepts of options trading with our FREE 160+ page Options Trading for Beginners PDF.

4. Option Vega Explained

So far, we have learned about delta, gamma and theta. Delta and gamma show us how an option reacts to a future change in stock price. Theta shows us how an option responds to the passage of time.

But how will an option react to future changes in implied volatility?

This is where vega comes in.

(V) Option Vega Definition: In options trading, Vega measures the expected change in the price of an option in response to a 1% change in implied volatility of the underlying security.

First off, it is important to understand that vega and implied volatility are not synonymous. Volatility measures the instability of a stock; vega shows us how an option reacts to potential, future changes in implied volatility.

Option Vega in Calls and Puts

Let’s first understand the fundamentals of vega.

1.) Vega is Most Affected By At-the-Money Options

I hope you’re starting to see a pattern here. Gamma, theta, and now vega are all at their zenith for at-the-money options. This is true also for vega. Why? At-the-money options are most sensitive to changes in implied volatility.

2.) All Options Have Positive Vega

Whether it be call or put, vega will always be positive for long options. When implied volatility goes up, both calls and puts increase in value. Vega isn’t concerned with the type of option, it focuses on the overall impact a change in future implied volatility will have on all options.

Long options love vega. Why? An increase in implied volatility is synonymous with the increase of an options price. Option sellers, however, do not like an increase in vega as they hope the options price (and the underlying implied volatility) will decrease.

AAPL Option Vega Example

| Type | Strike | Price | Vega | +1% Implied Volatility | -2% Implied Volatility |

|---|---|---|---|---|---|

|

Call |

147 |

3.25 |

.06 |

3.31 |

3.13 |

|

Call |

148 |

2.63 |

.07 |

2.70 |

2.49 |

|

Call |

149 |

2.11 |

.06 |

2.17 |

1.99 |

Where AAPL is trading at $148.20 and expiration is 2 days away.

Take a moment to study the above options chain for AAPL. As mentioned above, we can see that the at-the-money option (148 call) has the highest vega.

So how do we determine how the price of an option would change in response to a 1% increase in implied volatility? Simply add the vega to the value of the option. That’s it!

In the far right column, we threw a bit of a curveball; instead of a 1% decrease in volatility, we changed it to a 2% decrease. To determine how an option will react to a 2% decrease (or even 4%) in implied volatility, you only need to double (or quadruple) the options vega, and then subtract that value from the option price.

To see how the 148 call would respond to a 2% decrease in implied volatility, just double the vega, and subtract that number from the price (2.63-0.14= 2.49).

To learn more about vega, please check out our video below!

Option Greeks Summary

By this point, you should have a working understanding of how the Greeks can be helpful to you as an options trader. In conclusion, let’s review a few of our key terms.

- Option Delta: Measures how an option responds to changes in the underlying price.

- Option Gamma: Measured the acceleration at which an options delta changes.

- Option Theta: Measures how the price of an option changes with a one-day advancement to expiration.

- Option Vega: Measured the sensitivity of an option to changes in implied volatility.

Next Lesson

projectfinance Options Tutorials