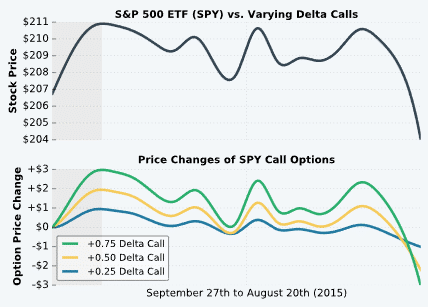

Delta estimates an option’s price change when the stock price rises or falls by $1. In other words, delta is used to gauge an option’s directional exposure.

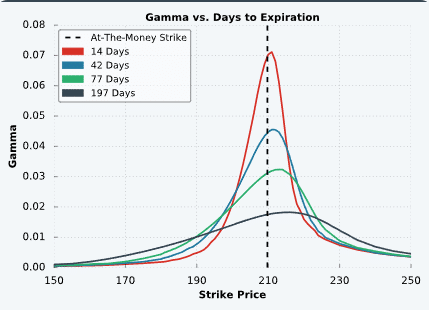

An option’s directional exposure changes when the stock price shifts. Gamma estimates how much an option’s delta will change when the stock price rises or falls by $1.

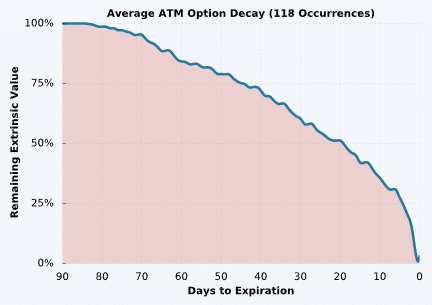

The passage of time is the enemy of option buyers, and the best friend of option sellers. Theta estimates how much an option’s price will fall with each day that passes.

(1)")