When trading volatility products, it’s imperative that you’re aware of the costs associated with the positions you enter. More specifically, being aware of the current VIX term structure (VIX futures curve) as it relates to historical levels can help you make more informed volatility trading decisions.

My First Volatility Mishap

In May of 2014, I had just purchased my first VIX futures contract. The reason for the trade was that implied volatility was low and the market had been grinding steadily higher without any breathers to the downside, and I anticipated a reversion in volatility. At the time, I had overlooked the fact that VIX futures converge towards the VIX Index as time passes, and when volatility is low, VIX futures typically trade at a premium to the VIX. The result? Steady losses on long VIX futures contracts (and other long volatility strategies/products) when market implied volatility remains low.

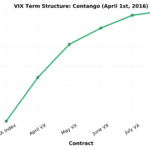

If you look at the graph below, you’ll notice that the front-month VIX futures are consistently above the VIX Index when the VIX is at suppressed levels (a structure referred to as “contango”):

Data compiled from Yahoo! Finance and CBOE VIX Futures Data.

When the VIX term structure is in contango, long volatility traders pay the price, and must correctly time the inevitable volatility increase to avoid the costs of contango. If the timing is off, the losses from contango lead to an increase in the cost basis of long volatility trades, which means a more significant increase in volatility is needed to break even or profit.

NOTE! In March, 2022, Barclay’s suspended sales and issuance of VXX. Read about other volatility finds in our article: “VXX Alternatives“.

Historical VIX Term Structure Levels

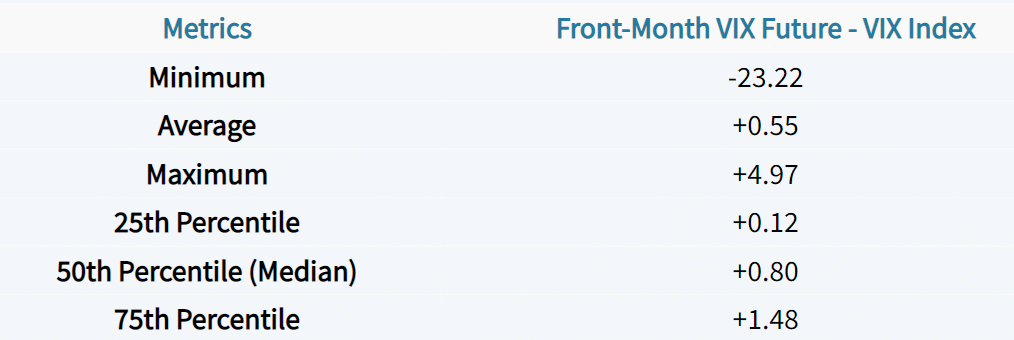

So, how often is the VIX futures curve in contango and backwardation? Here are the historical spreads between the front-month VIX Future and the VIX Index since 2008:

As we can see, the difference between the front-month VIX future and the VIX Index is typically positive, indicating that the VIX Index is at a discount to the front-month VIX future. Let’s take a look at some metrics that describe the spread’s history since 2008:

(1)")