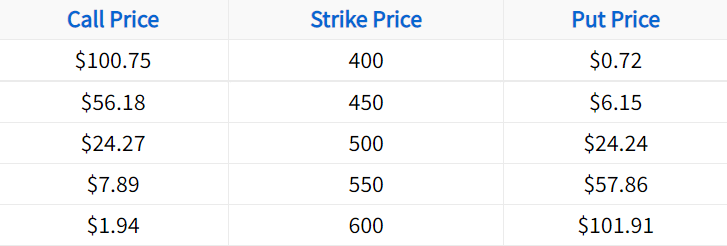

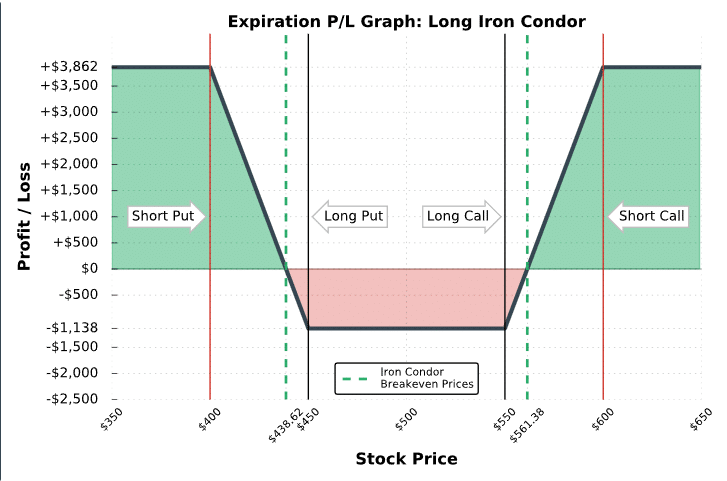

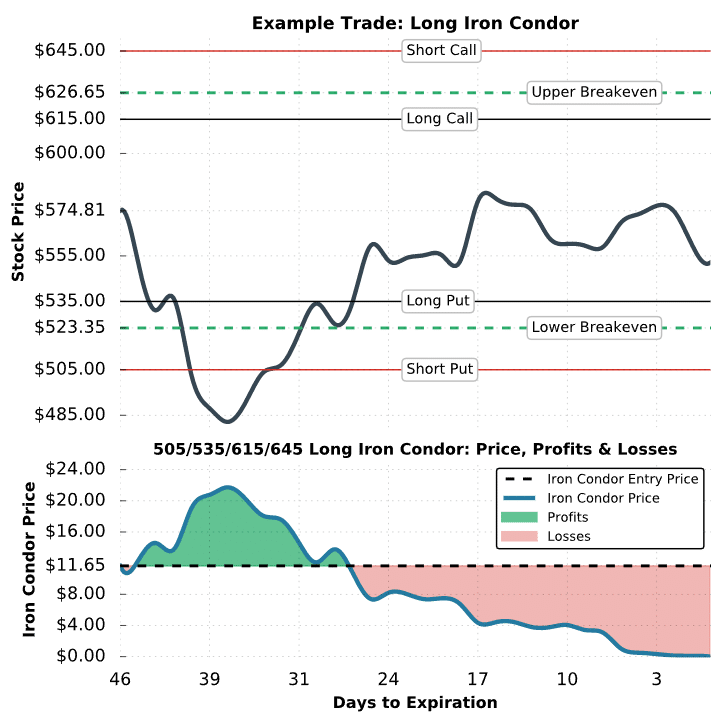

The profitability of iron condors will depend upon the “moneyness” structure of the options traded, implied volatility and the price of the underlying security.

The further an iron condor is sold out-of-the-money, the greater its possibly of success will be.

(1)")

2 thoughts on “Long Iron Condor Explained – The Ultimate Guide w/ Visuals”

Thanks for the article! Generally speaking, are long iron condors or short iron condors more profitable over the long run?

Thanks for the question Keith!

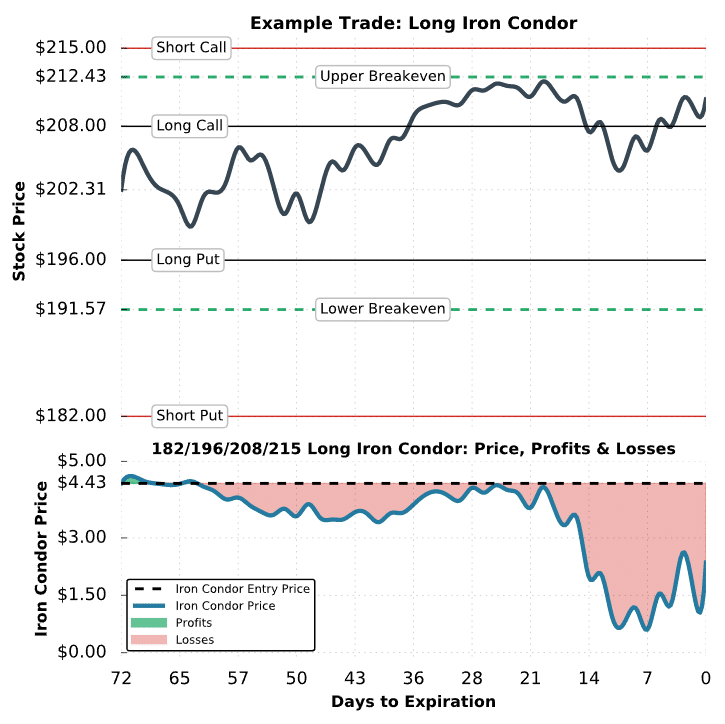

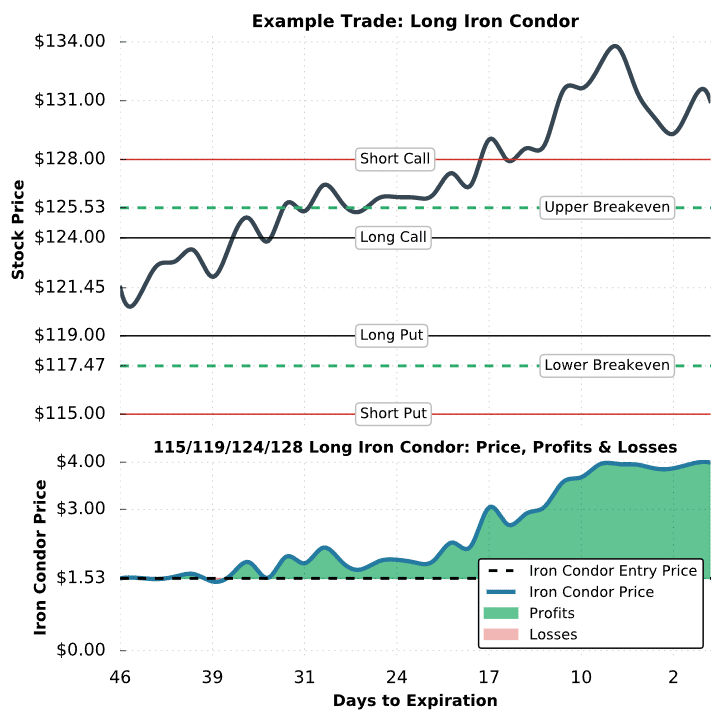

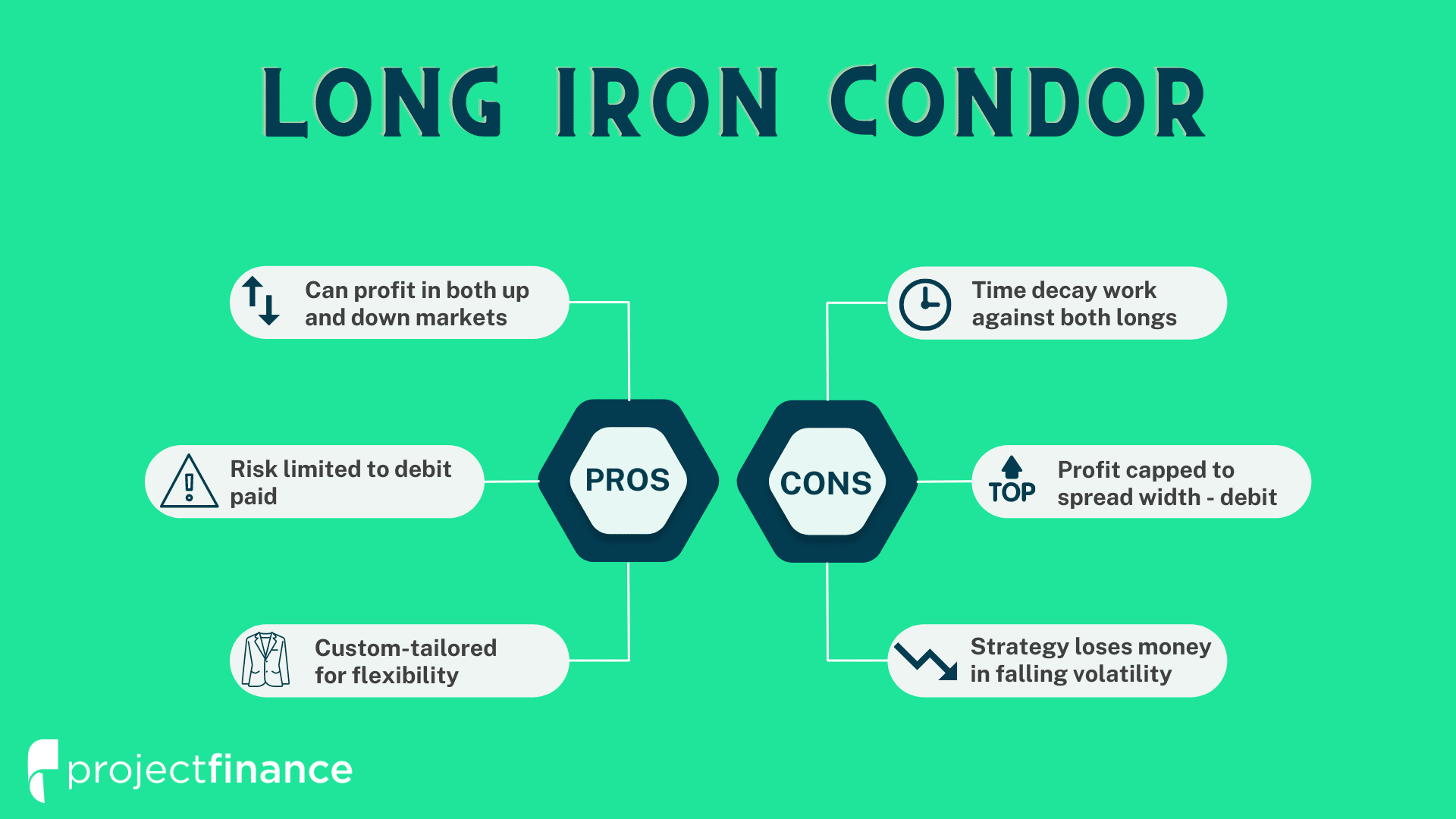

Over the long run, short iron condors tend to be more profitable than long iron condors. Why? Something called “time decay”. In the long iron condor, you’re net debit options (long a call and a put). If the stock doesn’t move at all, both of these options will fall in value. Double whammy!