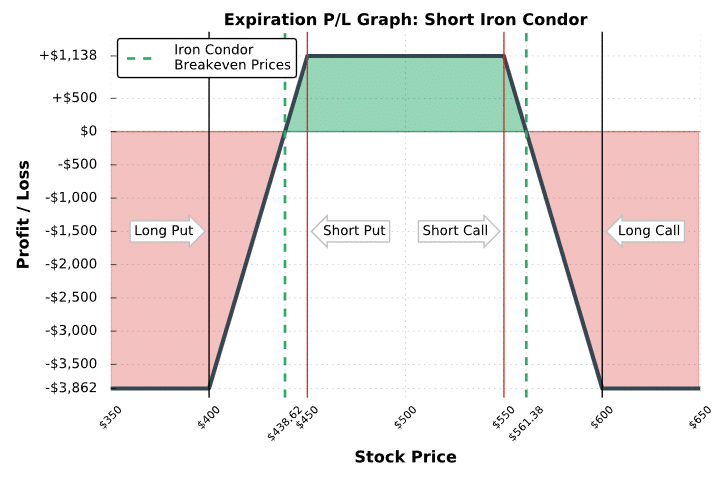

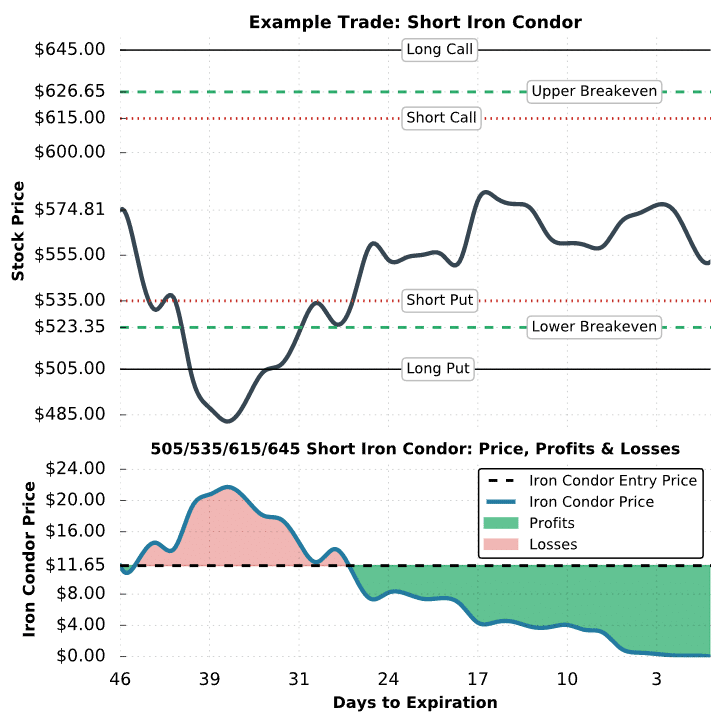

The long iron condor is the exact opposite trade of the short iron condor. Long iron condors are purchased for a debit while short iron condors are sold for a net credit.

When you buy an iron condor, you believe the underlying stock will make a large directional move either up or down. Short iron condors profit in a neutral market.

(1)")

2 thoughts on “Short Iron Condor Explained – The Ultimate Guide”

Thanks for the article!

From your experience, do you believe it is best to leg into iron condors, or just enter this trade all at once?

Thanks

Thanks for the question Tim!

That’s a tricky one. This all depends on your forecasted move for the underlying. If you think a stock is trading a little high, you can sell a call spread and if/when that stock sells off a bit, you can collect a little extra premium by selling a put spread.

Of course, the more time that passes, the more time decay (theta) will eat away at options, which means (in a constant environment) you will receive less credit for the put spread with each passing day.

Hope this helps!

Mike