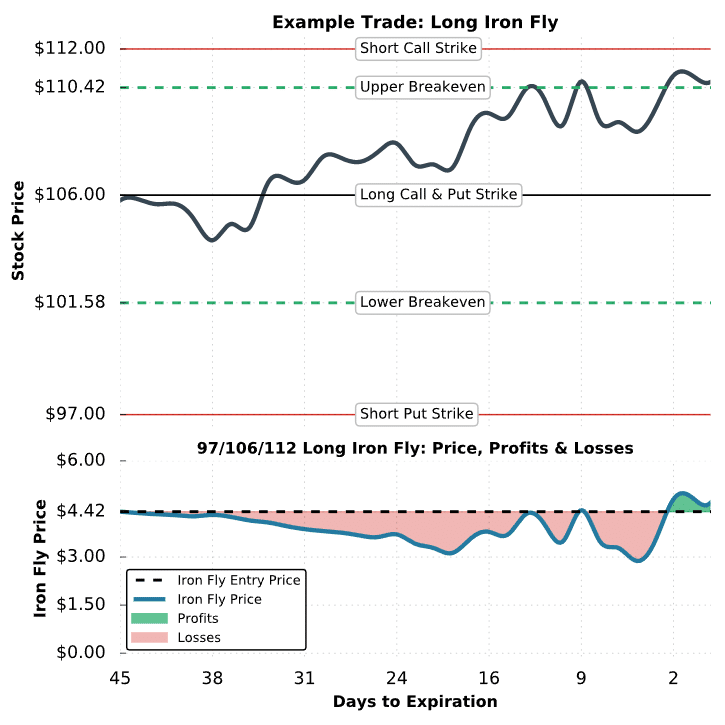

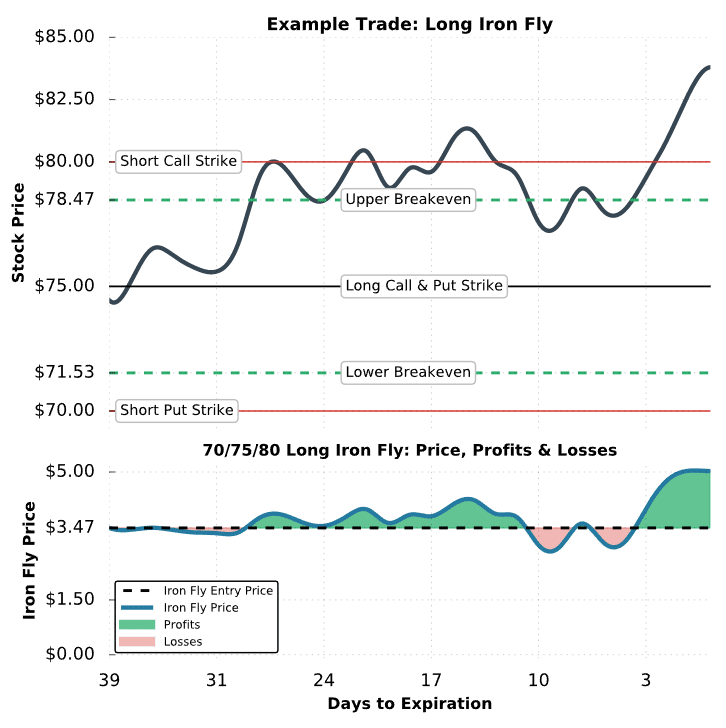

The first example we’ll look at is a scenario where a trader buys an iron fly, but the stock price is near one of the breakeven prices at expiration.

Initial Stock Price: $105.79

Strikes and Expiration: Long 106 Call and Put; Short 97 Put and 112 Call; All options expiring in 45 days

Premium Paid for Long Options: $3.04 for the 106 put + $2.50 for the 106 call = $5.54 in premium paid

Premium Collected From Short Options: $0.77 for the 97 put + $0.35 for the 112 call = $1.12 in premium collected

Net Debit: $5.54 in premium paid – $1.12 in premium collected = $4.42 net debit

Breakeven Prices: $101.58 and $110.42 ($106 – $4.42 and $106 + $4.42)

Maximum Profit Potential (Upside): ($6-wide call spread – $4.42 debit) x 100 = $158

Maximum Profit Potential (Downside): ($9-wide put spread – $4.42 debit) x 100 = $458

Maximum Loss Potential: $4.42 debit x 100 = $442

As mentioned earlier, the maximum profit potential of a long iron butterfly depends on the wider spread. In this example, the long call spread is $6 wide, and the long put spread is $9 wide. Because of this, the maximum profit potential of this iron fly occurs when the stock price collapses through the long put spread. More specifically, this trade has $158 in profit potential on the upside and $458 in potential profits on the downside, resulting in a bearish bias.

Let’s see what happens!