Last updated on March 31st, 2022 , 10:10 am

Jump To

If you spent any time during 2021 reading about stocks like AMC Entertainment Holdings Inc (AMC) and GameStop Corp. (GME), chances are you came across the phrase “gamma squeeze”. Will the trend continue into 2022?

In a nutshell, here’s what this means.

TAKEAWAYS

- A gamma squeeze causes dramatic swings in the price of a stock, almost always on the upside

- A gamma squeeze is caused by traders purchasing large volumes of near-term call options

- Market makers that sell these options most hedge their short-call positions with long stock in a process called “gamma hedging”

- Gamma is one of the options Greeks and is the second derivative of “delta”, which is the first Greek

- A “short squeeze” is the product of many traders buying back a short stock that moves against them; a “gamma squeeze” occurs only on stocks that offer options, and is caused by call option buying

Gamma Squeeze and Call Options

During the meme stock craze of 2021, retail traders were buying hoards of near-term “call options” on stocks like AMC, GME, and BBBY.

Call options are derivatives that allow traders to place leveraged upside bets on an underlying stock. Puts, conversely, allow traders to bet the same way, but these contracts profit when the security falls in value. In this article, however, we will be focusing on calls, as they are the culprits behind gamma squeezes. Let’s do a quick rundown of call options before we continue.

- A call option gives the owner the right to purchase 100 shares of an underlying stock at a specific price by a specific date

- Call options are bullish, meaning a purchaser expects the underlying to go up a lot in value. If the stock stays the same or goes down, long calls lose money

- The expiration date for options varies widely; from days to years away (LEAPS).

- A gamma squeeze results from massive near-term call option buying

So retail traders buying these short-term call options were the catalyst to numerous gamma squeezes. But in order to understand what this means, we have to look at the parties that were selling these call options to the retail traders: market makers.

(1)")

New to options trading? Learn the essential concepts of options trading with our FREE 160+ page Options Trading for Beginners PDF.

Market Maker Explained

Market Maker Definition: A liquidity provider who facilitates both buy and sell orders on a particular security.

Whenever you send an order to get filled, chances are this order is routed to a market maker. If you buy 100 shares of TSLA, this market participant will sell you 100 shares of TSLA, leaving them short 100 shares of the stock.

The same is true of options.

If you were to buy 10 call contracts on GME, a market maker would sell you those contracts. You would be long 10 options; the market maker would be short 10 options.

Market makers make money by buying at the bid and selling at the offer. You can compare this profession to that of a car dealer – a car dealer buys cars at an auction, then sells the cars to you, pocketing the “spread”. Depending on the size of the trades and widths of the market, market makers can make a pretty good living.

Market Makers and Hedging

So let’s imagine you are a market maker who just sold a customer 10 call options on GME. That leaves you net short a pretty large position in a pretty volatile stock. Wouldn’t you prefer to hedge (or offset) that short option position as fast as you can? Remember, you’re after the “spread”, not market speculation.

In order to hedge their short-call options, market makers purchase stock. The goal of non-speculating market makers is to maintain a delta-neutral position. This means that they have offset all of their risks. Maintaining this neutrality is a constant battle.

A long stock position offsets a short call position. When a lot of calls are purchased, a lot of stock must also be purchased in return by market makers. This causes the stock price to skyrocket, resulting in a “gamma squeeze”.

We mentioned “delta-neutral” before. Delta is one of the option Greeks. Gamma, too, is one of the option Greeks. In order to understand gamma, however, we must first understand delta.

Let’s get started!

Option Delta Explained

Δ Option Delta Definition: In options trading, the Greek “delta” represents the amount an option price is forecasted to move in relation to a $1 change in the underlying stock price.

In options trading, the Greek “delta” allows a trader to predict how a particular option will react to a future change in the price of a security. In other words, delta offers traders a window into the future.

Like everything in options trading, the Greeks are standardized. An options delta is the amount the price of an option is expected to move in relation to a $1 change in the underlying stock.

- Call options have a delta value between 0 and +1.

- Put options have a delta value between 0 and -1.

Let’s take a look at a simple options chain now to see delta in action.

AAPL Option Delta Example

| Type | Strike | Price | Delta | +$1 Share Price Affect | -$1 Share Price Affect |

|---|---|---|---|---|---|

|

Call |

147 |

3.25 |

.64 |

3.89 |

2.61 |

|

Call |

148 |

2.63 |

.52 |

3.15 |

2.11 |

|

Call |

149 |

2.11 |

.42 |

2.60 |

1.62 |

Where AAPL is trading at $148.20

The above table illustrated how the prices of various AAPL call options react to a +/- $1 move in the underlying stock.

Let’s look at the 148 call, initially valued at $2.63. If the stock price were to pop by $1 immediately, the price of this call would rise to $3.15. How did we get this number? By simply adding the delta to the previous price. Voila! That’s delta (in a nutshell).

In addition to telling us the expected move of an options price to a $1 change in the price of an underlying stock, delta also has a few more useful functions. An options delta also tells us:

- The odds that an option has of expiring in the money. A delta of 0.40 has a forty percent chance of expiring in-the-money.

- How many shares of stock an option “trades like”. An option with a delta of +0.60 will trade similar to 60 long shares of the underlying stock.

So now we have delta down. Let’s move on next to gamma, which is actually a derivative of delta! It’s not that confusing – I promise!

Option Gamma Explained

(Γ) Option Gamma Definition: The Greek “gamma” measures the rate at which an options delta changes in response to the price movement of the underlying stock.

In order to truly understand gamma, you must first understand delta, so make sure you mastered this Greek before we move on.

Gamma tells us how the future delta of an option will change in response to a one-point move in the underlying stock.

Before we dive into gamma, let’s look at a few of this Greek’s key characteristics:

- Long Options Produce Positive Gamma; Short Options Produce Negative Gamma

- Gamma is Highest for At-The-Money Options

Take a moment to study the below table.

AAPL Option Gamma Example

| Type | Strike | Price | Delta | Gamma | New Delta (+$1 Share Price ) | New Delta (-$1 Share Price) |

|---|---|---|---|---|---|---|

|

Call |

147 |

3.25 |

.64 |

.06 |

.70 |

.58 |

|

Call |

148 |

2.63 |

.52 |

.08 |

.60 |

.44 |

|

Call |

149 |

2.11 |

.42 |

.06 |

.48 |

.36 |

Where AAPL is trading at $148.20

Before, we learned that delta shows us how an option reacts to a one-point change in the price of an underlying.

Gamma goes a step further here and tells us what the future delta will be when the stock moves by one point. Gamma is known as the first derivative of delta for this reason.

By looking at the 148 call, we can see that this options delta will increase by 0.08 if the stock were to go $1 higher, and decrease by 0.08 if the stock were to go $1 lower.

Long Gamma vs Short Gamma

When a market participant buys options, they are said to be “long” gamma.

A long gamma position implies that the delta of an option(s) will increase when the stock price rises, and decrease when the stock falls.

When a market participant sells options, they are said to be “short” gamma.

A short gamma position implies that the delta of an option(s) will fall when the stock rises, and rise when the stock prices falls.

To read more about this, check out our article, “Long Gamma vs Short Gamma”.

Gamma Hedging Explained

As we said before, the Greeks are used by market makers to reduce or eliminate risk.

When traders use delta to hedge, this is called “delta hedging“. When traders use gamma to hedge, this is called “gamma hedging,”

Since delta only looks at how an options price will change in value for the next dollar move in the underlying, it has its limitations. What about the dollar after that? And so on.

Gamma hedging allows traders to offset risk for potential future large moves in the underlying and is the preferred method of hedging amongst professionals. This is why it is called a “gamma squeeze” and not a “delta squeeze”.

That isn’t to say that delta hedging isn’t used; gamma hedging is simply a more important tool. They are typically used in tandem.

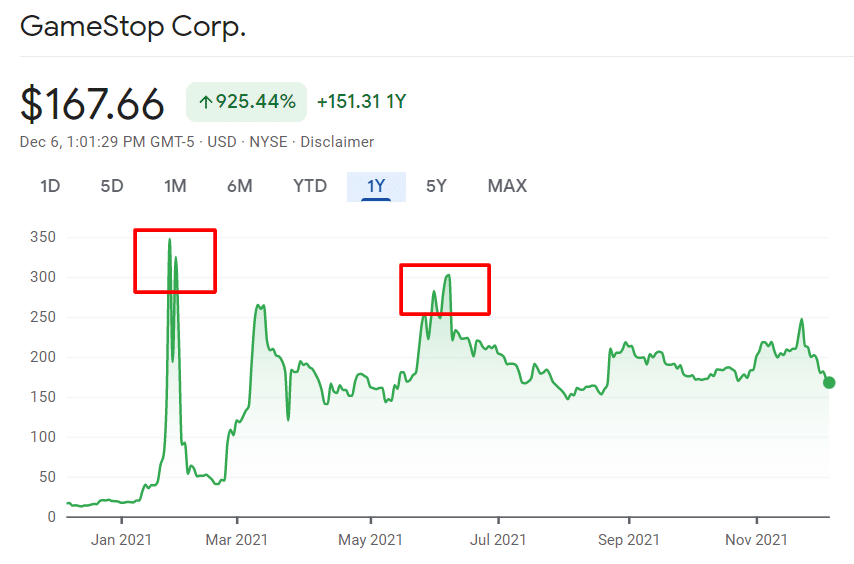

GME Gamma Squeeze

Chart from Google Finance

Take a look at the above one-year chart on GameStop (GME).

During these incredible rallies, retail traders were buying as many call options as they could. Market makers were fulfilling their duty to provide liquidity by filling these orders as they came in.

This left the market makers with short-call options. As we learned, a short options position leaves a trader with “short gamma”.

Being naked short gamma in GME is a huge risk. In order to offset this risk, market makers purchased stock.

But how much stock do they need to purchase? This number was communicated to them via the Greek gamma. They were short a ton on gamma, so, therefore, had to purchase a ton of stock, thus wildly driving up the price of GME.

A gamma squeeze is a relatively rare market phenomenon, occurring mostly when short-term call buying precipitates in an uncontrollable fashion, as it did for several meme stocks.

If you’re on the right side of the market, a gamma squeeze can make you a lot of money. If you’re on the wrong side – watch out!

Sometimes, the term “gamma squeeze” gets confused with “short squeeze”. Let’s end this article by looking at the fundamental difference between these two market events.

Gamma Squeeze vs Short Squeeze

Short Squeeze Definition: A short squeeze occurs when there is more demand than supply for a security due to short positions being repurchased.

You can both buy and sell short shares of stock. When you sell a stock, you profit when the stock goes down in value. Companies with dim prospects are shorted frequently. There is no cap on how high a stock can go, therefore, short sellers of stock have infinite risk.

Take a look at the below chart of AMC stock.

AMC Short Squeeze

Chart from Google Finance

Imagine selling AMC for $20/share only to have it rally to $50/share a couple of days later. Your maximum gain was only $20 in this scenario. You would have lost more than twice what you could have made under the best-case scenario if the stock went to zero.

When you sell a stock, you do so on margin, which is essentially borrowed funds from your brokers.

If your position moves against you and you don’t have the funds to hold the position, you will enter a “margin call”. Your broker will either require you to deposit funds in your account, or they’ll take the liberty of liquidating your account for you. How do they do this? By buying the stock you are short.

When a short squeeze happens, it tends to happen all at once, creating a domino effect. This mass buying sends the stock higher. Check out this article on gamma squeeze by RagingBull to learn more.

Short selling is rooted in equity trading and traders are the cause; gamma squeeze is rooted in options hedging and market makers are the cause.

There are two ways to determine whether or not a stock is experiencing a gamma squeeze or short squeeze:

- Only stocks that have options can experience gamma squeeze; if there are no options, there is no gamma squeeze.

- A gamma squeeze can be confirmed by determining whether or not large call buying takes place simultaneously as the stock price rallies. The historical volume of options can be charted on most trading platforms.

As stated by the Wall Street Journal, GME’s meteoric rise wasn’t caused by a short squeeze, but by market makers hedging their short calls.

Can a short squeeze and a gamma squeeze happen simultaneously? Absolutely! It can be difficult to tell sometimes why, exactly, certain securities rise sky-high over a short period of time. However, these two rare market events are often to blame.

Next Lesson

projectfinance Options Tutorials

Mike Martin

New to options trading? Learn the essential concepts of options trading with our FREE 160+ page Options Trading for Beginners PDF.