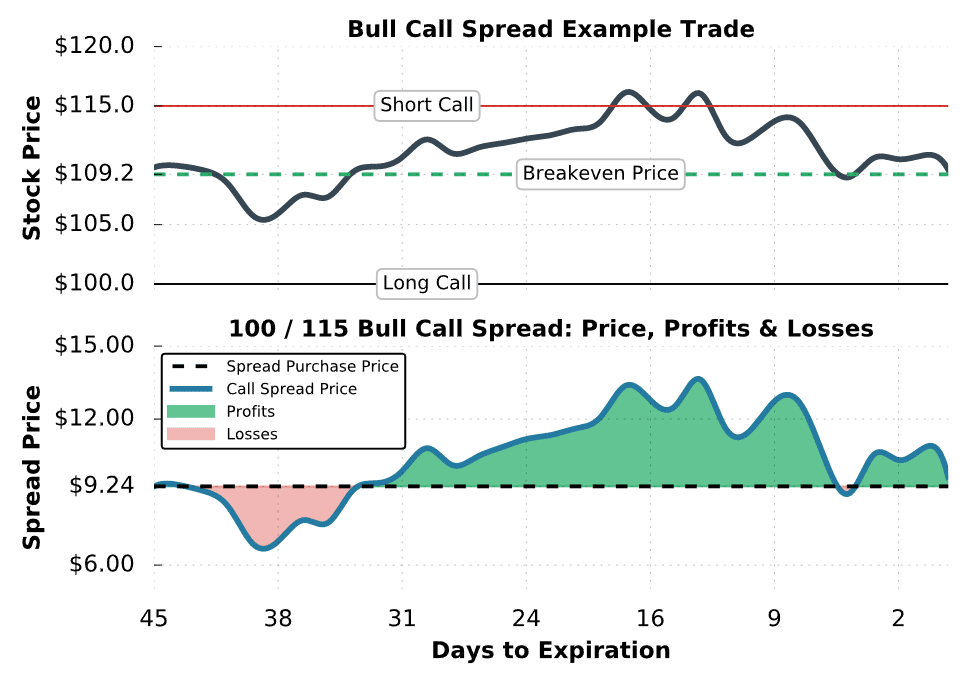

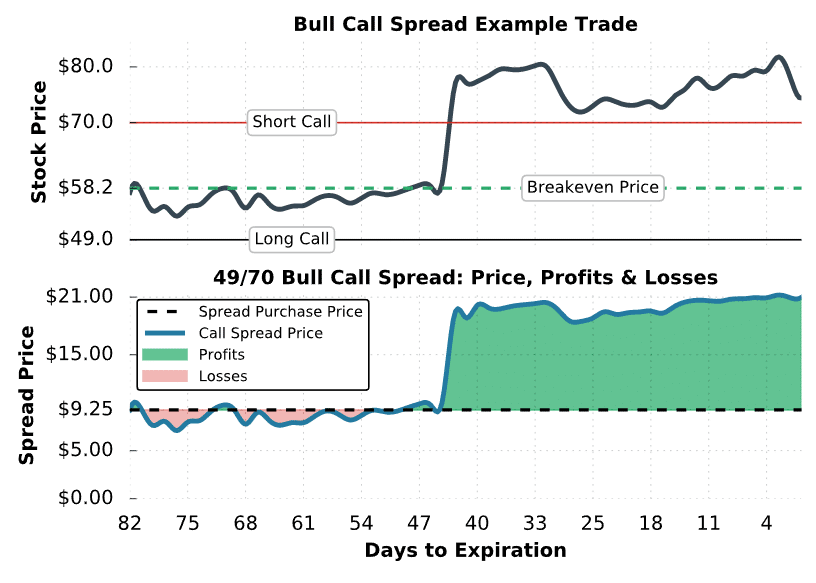

In the first 30 days of the trade, the stock price stagnates around the breakeven price of the long call spread. However, with around 45 days to expiration, the stock jumps 30% to $80 after an earnings announcement.

With the stock price $10 above the short call strike, the long call spread is worth around $20. With $21-wide strikes, the spread’s maximum value is $21. So, even though the position has around 45 days to expiration, the long call spread is worth near its maximum potential value.

When the call spread is worth $20, it’s likely that the long call spread trader closes the position for a profit because there’s only $1 left to make and $20 to lose.

If the trader did sell the spread for $20, the realized profit would be $1,075: ($20 sale price – $9.25 purchase price) x 100 = +$1,075.

Finally, if the spread was held through expiration, no stock position would be taken on because the exercise/assignment of the long and short call options cancel each other out. However, it’s possible that the spread trader is assigned on the short call when it’s deep-in-the-money before expiration.