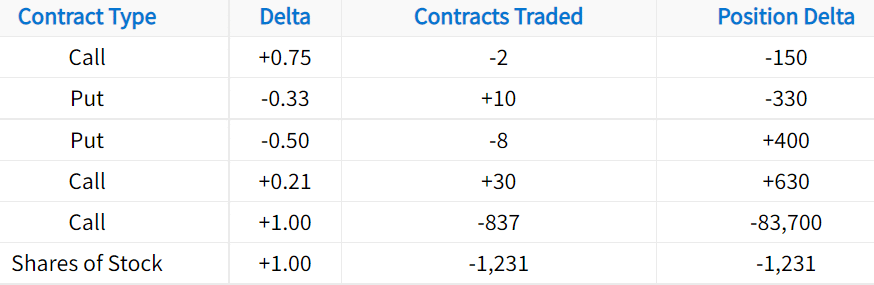

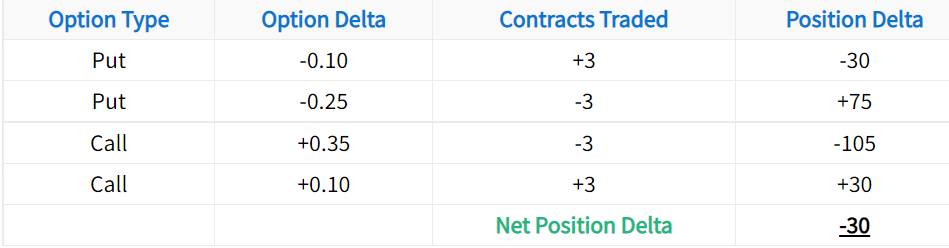

To calculate the position delta for a standard equity option position, the following formula can be used:

The following table demonstrates this formula applied to various simple option positions:

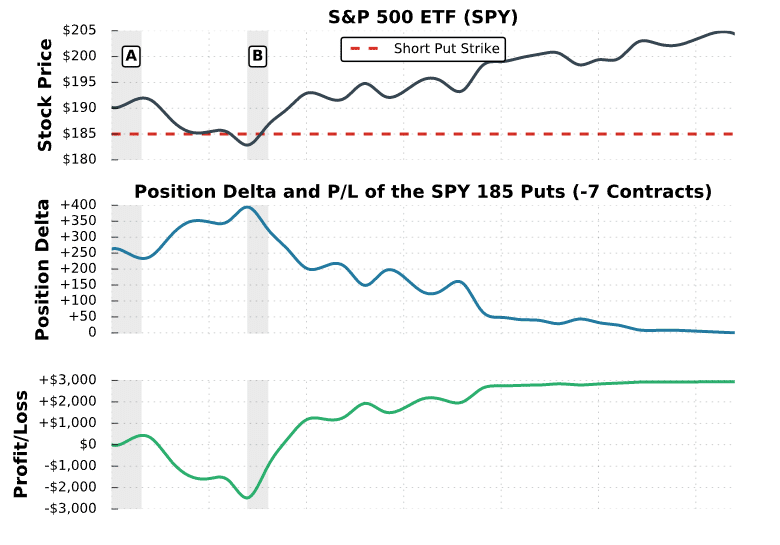

To make things easier for you, we’ve shaded two regions that demonstrate the accuracy of position delta. The following table compares the expected vs. actual P/L based on the position delta in each region.

Thanks for the read!

Quick question – do high deltas mean that a trade has a higher probability of success?

Thanks!

Thanks for the question Pauline!

In-the-money options have a greater probability of success than out-of-the-money options. As we learned, in-the-money options have higher deltas than out-of-the-money options. Therefore, higher deltas do indeed mean a higher probability of success. However, higher delta options also cost more money to purchase, and therefore have greater risk!

Mike