(1)")

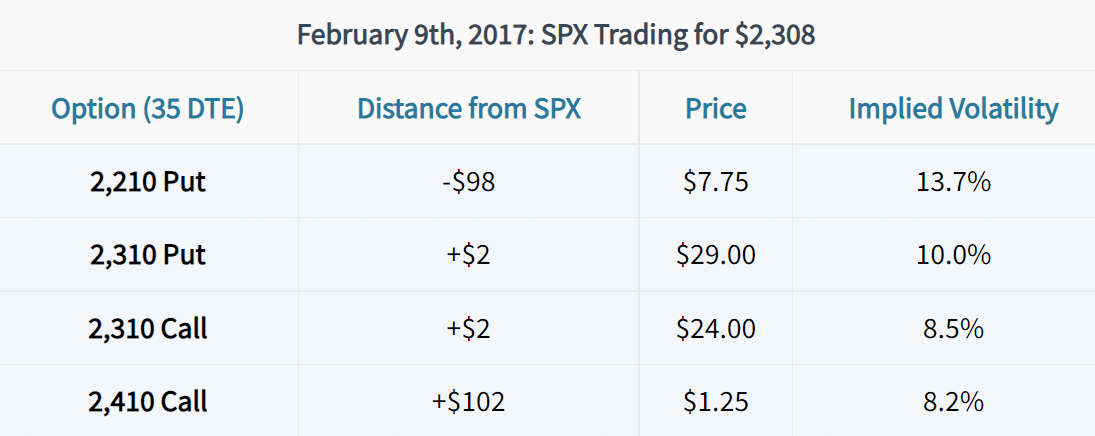

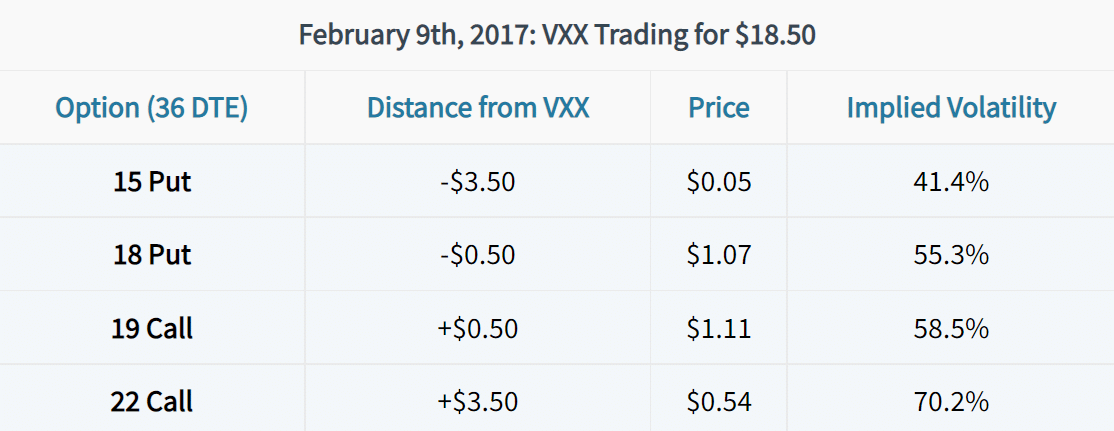

In this case, we can see that the price and implied volatility of the out-of-the-money put (15) are far less than the price and implied volatility of the out-of-the-money call (22) that’s the same distance from the current price of VXX. As a result, the volatility skew in VXX is to the upside.

What Does Volatility Skew Tell You?

There are three useful pieces of information that one can glean from an underlying’s volatility skew:

1. The direction in which the risk is perceived to be in the underlying.

2. How implied volatility will change relative to movements in the underlying.

3. The prices of call spreads and put spreads on that underlying.

#1: An Underlying’s Perceived Risk

As discussed earlier, a downside volatility skew indicates that the market is pricing in more risk for decreases in the underlying than increases in the underlying. On the other hand, upside volatility skew indicates more risk being priced into increases in the underlying than decreases in the underlying.

#2: How Implied Volatility Will Change Relative to Underlying Movements

In stocks with downside volatility skew, the implied volatility of the underlying will typically increase if the stock price falls. As an example, let’s look at the relationship between the S&P 500 Index and the VIX Index:

The VIX Index quantifies the prices (implied volatility) of near-term options on the S&P 500 Index (SPX). As shown earlier, SPX typically has downside volatility skew. In the chart above, we can see that when SPX falls, SPX implied volatility (the VIX) tends to increase.

What about on an underlying with upside volatility skew? To illustrate changes in implied volatility on an underlying with upside volatility skew, let’s examine the relationship between changes in the VIX Index and the implied volatility of VIX options (quantified by VVIX):

As we can see here, as the VIX Index increase, so do the implied volatilities of VIX options (VVIX).

So, volatility skew can tell you how the implied volatility of the underlying’s options are expected to change relative to changes in the underlying price.

Why does this matter? Well, if you’re trading positive delta, positive vega strategies on a product with upside volatility skew, you’ll know that an increase in the underlying should lead to profits from changes in direction and volatility.

On the other hand, if you’re trading negative delta, negative vega strategies on a product with downside volatility skew, and that underlying falls in price, you can expect some of your directional profits to be offset by an increase in volatility.

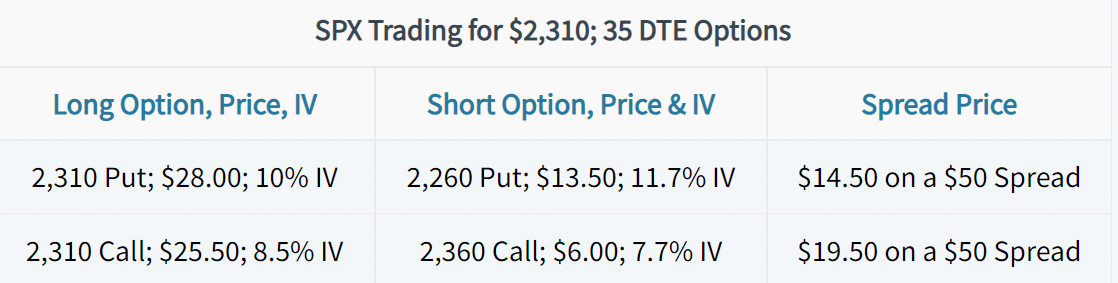

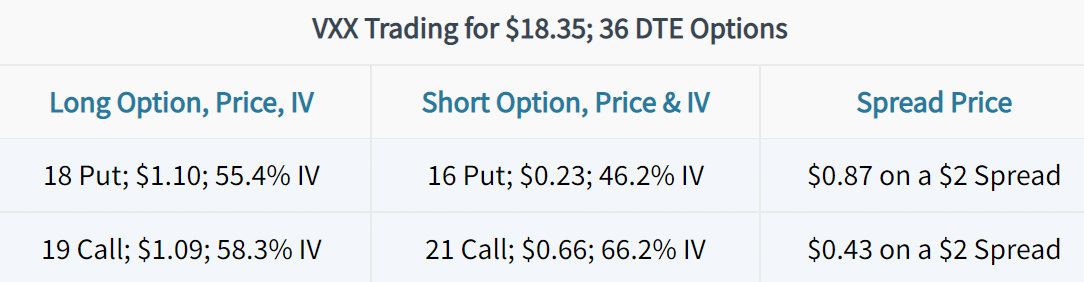

#3: The Prices of Call Spreads and Put Spreads

The third helpful piece of information that the skew of an underlying’s option volatility can tell you is the price of call and put spreads (in a broad sense):

Let’s take a look at some examples: