Last updated on March 28th, 2022 , 02:05 pm

VIX Contango: The Ultimate Beginner's Guide

Stock market volatility products are confusing for beginner market participants because of their complexity.

Fear not!

In this particular guide, you will develop an understanding of:

Contango and backwardation in the Cboe volatility index (VIX) market

The major implications it has for the performance of popular volatility products such as VXX and UVXY.

VIX trading strategies for contango and backwardation market conditions

Prepare to take one step closer to becoming a master of the VIX/volatility landscape!

Jump To

What is Contango?

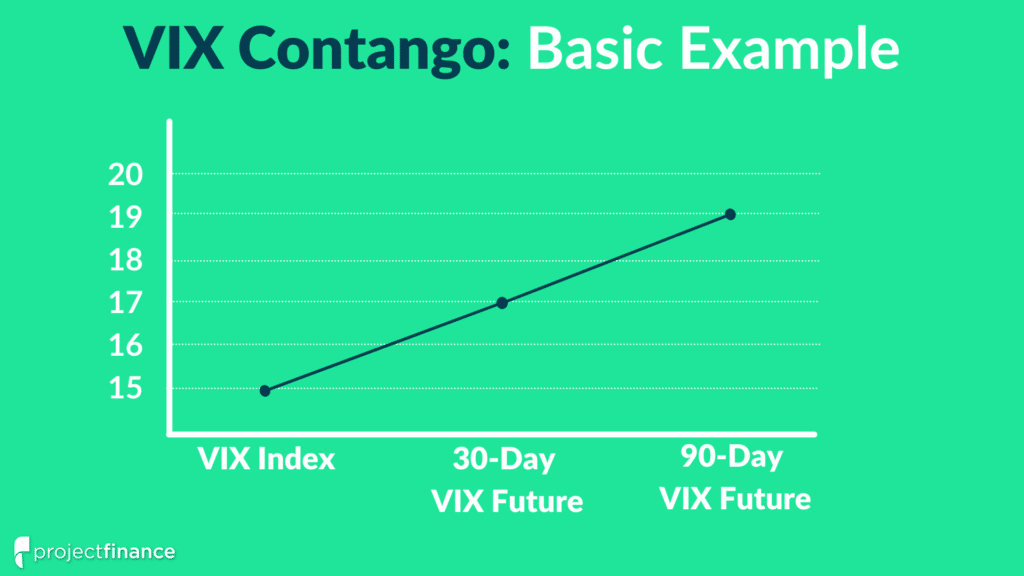

“Contango” refers to a situation where futures contracts trade at a premium to the “spot” price (the current price) of a commodity/index.

For example, if the Cboe VIX index is at 15 and the VIX futures contract settling in 30 days is 17, we have contango in the VIX futures market.

Here’s a simple example visualization of contango:

Contango is typically present in the VIX market, making it more useful to understand than backwardation (the opposite of contango). We will briefly cover backwardation in a later section.

Why is Contango Important to Understand?

Contango in the VIX market drives the performance of volatility products and trading strategies, so understanding it will help you make more informed trades.

In the VIX market, the VIX index is the calculation of expected S&P 500 volatility based on 30-day S&P 500 index (SPX) option prices. But we can’t directly trade the VIX index because there are no VIX shares. To trade VIX index predictions, traders turn to VIX options and futures.

But before trading futures, it’s essential to understand how futures prices perform over time relative to the spot price.

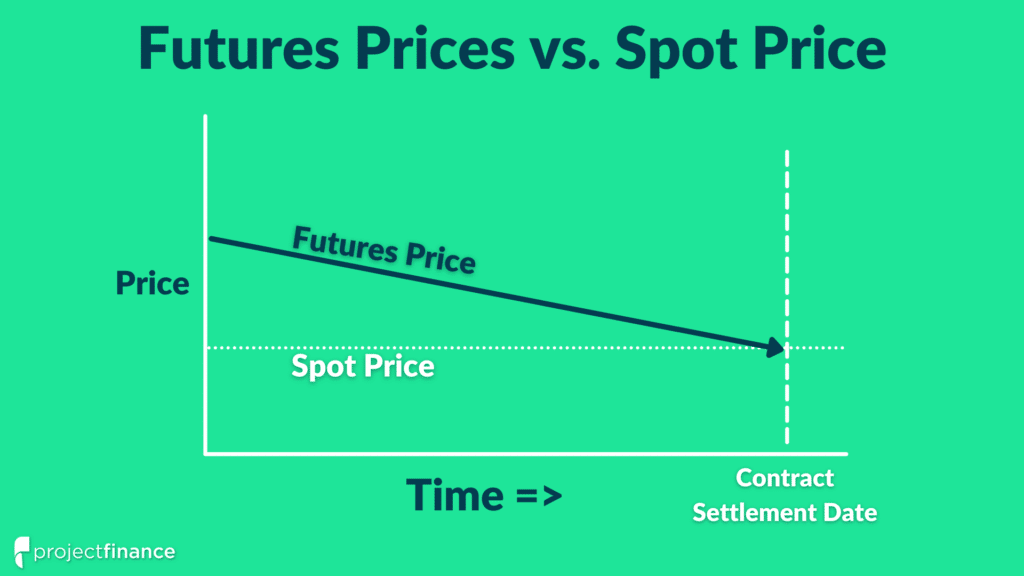

Futures Prices Converge to the Spot Price

A critical concept to understand in futures markets is that futures prices converge towards the spot price over time:

On a futures contract’s expiration date, the contract’s price will equal the spot price.

A futures contract with no future equals the spot price.

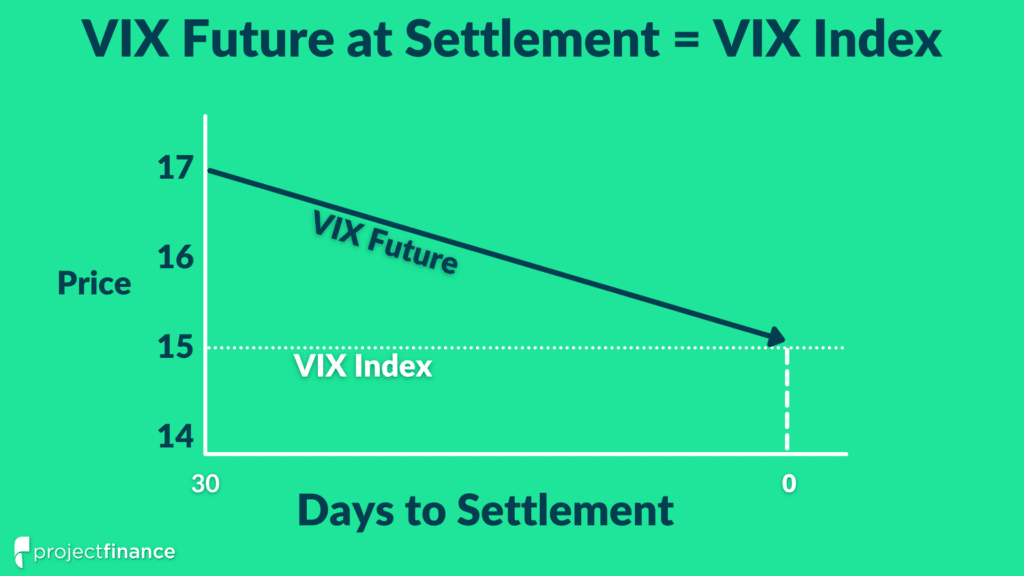

For example, if the VIX index is at 15 and a 30-day VIX futures contract is at 17, the contract’s price will fall from 17 towards 15 with each passing day if the VIX index remains at 15:

The above image illustrates how a futures price converges to the spot price over time if the spot price remains constant.

In reality, the VIX index will fluctuate as market volatility changes, but volatility index futures will get “pulled” towards the index as their settlement dates approach.

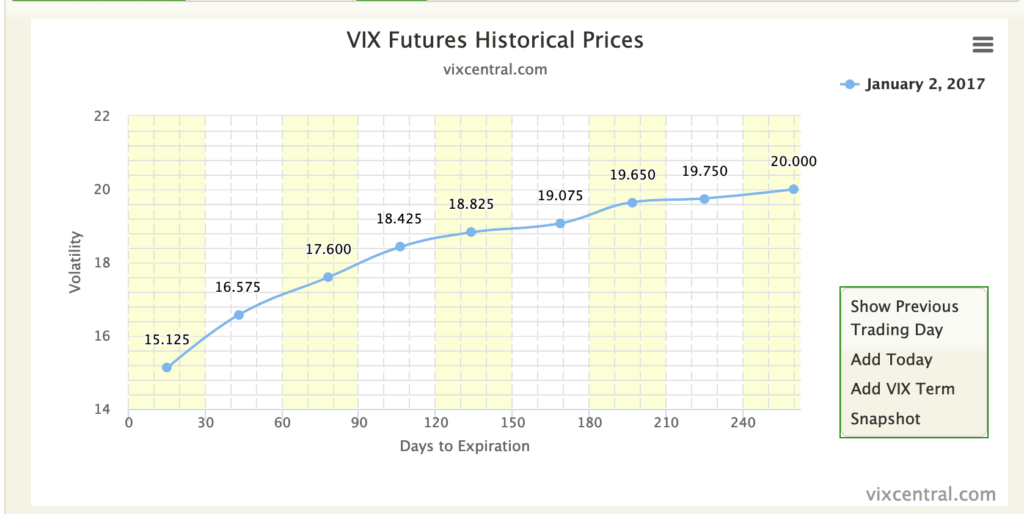

Here’s a visual using real historical data to prove this:

As we can see, each contract’s price equals the VIX index value at expiry.

What can we do with this information?

The VIX Futures Curve

Volatility traders pay close attention to the “VIX futures curve” or “VIX term structure” because it can inform them of how volatility products will perform over time if volatility remains unchanged. It also tells us how much we need the VIX index to change for our volatility trades to work out.

The “VIX futures curve” is simply a chart of the prices of VIX futures contracts with varying expiration dates, from shorter-term to longer-term.

VIX Central is a free resource for visualizing the current VIX futures curve, as well as viewing historical curves.

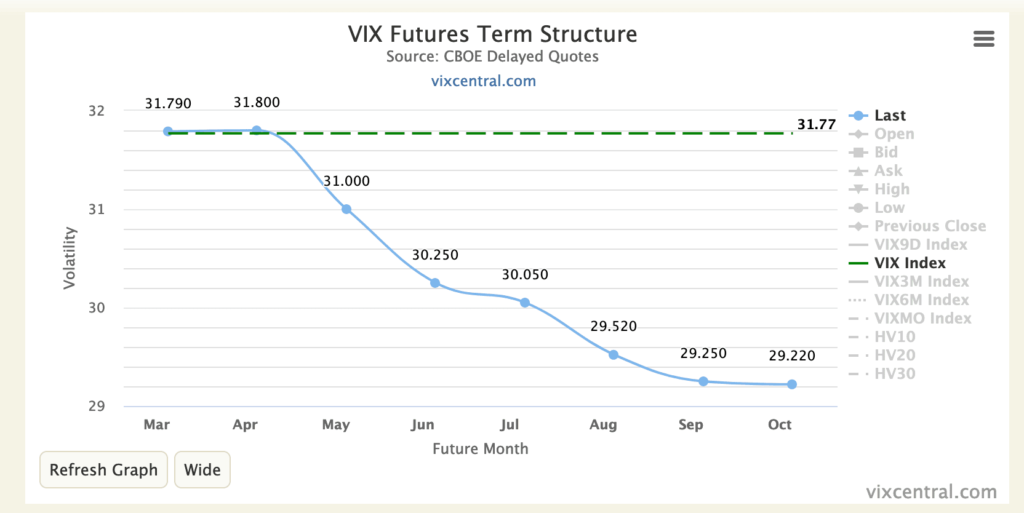

VIX Contango Example

When the VIX futures are in contango, we get an upward-sloping curve, indicating that longer-term contracts are more expensive than shorter-term contracts:

VIX Backwardation Example

When the VIX futures are in backwardation, we get a downward-sloping curve, indicating that longer-term contracts are cheaper than near-term contracts.

The current futures curve is in backwardation as I write this in March 2022:

In the above curve, the March and April contracts are trading at the level of the VIX, but the longer-dated contracts are at lower and lower values the further out the settlement date.

During normal/low volatility market periods, the VIX futures are usually in contango. We’ll explore the intuitive understanding of why that is in a later section.

VIX Futures Contango vs. ETP Performance

The performance of VIX futures determines the performance of popular volatility exchange-traded products (ETPs).

For example, the daily performance of VXX is equal to the daily percentage changes of front-month and back-month VIX futures. Be sure to read our guide on VXX for an in-depth understanding of this product’s mechanics.

When VIX futures contango is present, short-term VIX futures contracts will bleed value with each passing day if the VIX index does not increase.

The result? Long volatility products like VXX and UVXY will experience drawdowns since their performance stems directly from daily changes in VIX futures. Short volatility products like SVXY and SVIX benefit from persistent contango.

Why Are VIX Futures Usually in Contango?

During normal market conditions, the Cboe VIX Index is typically below 20. When the VIX is below 20, it’s common for contango to be present in the VIX futures market.

An easy way to understand why is to think of a VIX futures contract as insurance. When stock market volatility increases, the VIX index and futures rise, making them popular hedging instruments for risk managers.

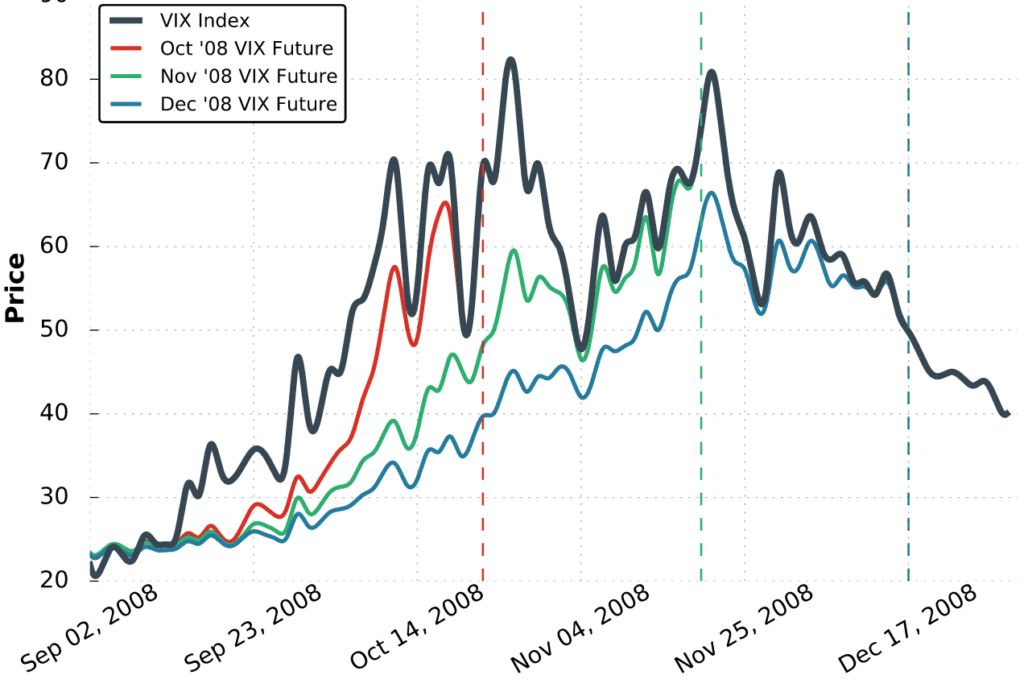

During a financial crisis, such as in 2008 or 2020, the VIX index and futures spiked as the stock market collapsed violently.

Here’s how the volatility index futures reacted to the VIX spike in 2008:

If the market is in a low volatility period, risk management desks might buy VIX futures to hedge their portfolios against an increase in market volatility. As seen above, long positions in volatility index futures will gain value during market crises. The profits from these long volatility positions will offset losses in long equity positions.

Since futures contracts have expiry dates, volatility traders must decide between hedging short-term and long-term.

Generally speaking, there’s a higher probability of negative events occurring over a longer period of time (such as five years) as opposed to a shorter period of time (such as one month).

The probability of the market falling 10% is higher over a 1-year period than a 1-week period.

As a result, buying long-term VIX futures provides traders with a long duration of protection, justifying a higher price compared to buying a short-term future that provides only a small window of protection.

And so during normal market conditions, longer-term volatility futures trade at higher prices than shorter-term volatility futures, resulting in contango in the VIX futures market.

How can traders take advantage of contango in the VIX?

VIX Contango Trading Strategies

When contango is present, VIX futures and long volatility products like VXX and UVXY all predictably lose value if the VIX does not increase.

The VIX index is directly tied to the realized S&P 500 volatility.

If S&P 500 volatility increases, traders will bid up SPX option prices (which are used to calculated the VIX) as the expected movements of the S&P 500 index increase.

If S&P 500 volatility falls, the expected movements of the S&P 500 index contract. SPX option prices will fall (VIX falls).

Shorting VIX futures

Shorting VXX/UVXY shares

Buying puts on VIX/VXX/UVXY

Shorting calls on VIX/VXX/UVXY

These strategies can profit from persistently low market volatility, as the VIX futures will remain in contango and steadily lose value as they converge towards the lower VIX spot price (visualized earlier in this post).

However, traders should be cautious with short volatility trading strategies because when market volatility increases, it can do so violently.

For example, in the financial market crisis of 2020, the VIX index went from below 14 to over 80 within two months as the S&P 500 fell over 30%. Traders who were short volatility got destroyed during that time period, while traders who were long volatility experienced massive profits.

If you want to profit from contango in the VIX futures, trading strategies such as buying put options on VXX or UVXY provide traders with limited loss potential in the event of a spike in market volatility.

What Happens When VIX is in Backwardation?

The majority of this guide covers contango because it is present in the VIX market a high percentage of the time.

VIX backwardation occurs when the VIX index is above VIX futures contracts, and longer-term futures are at a discount to shorter-term futures.

Backwardation in VIX futures occurs when market volatility is elevated.

Since VIX futures always converge towards the spot VIX over time, VIX futures will appreciate over time if the spot VIX remains above these futures contracts.

For example, if it is February 1st and the VIX is at 50, and the March VIX future is at 40, the March VIX future will appreciate 10 points by its expiration date if the VIX index remains at 50.

That means long volatility ETPs like VXX and UVXY will also appreciate over that period since they track the daily percentage changes of short-term VIX futures.

But market volatility is always changing, and periods of extreme market volatility typically do not last long. Consequently, the VIX market can go from backwardation to contango quickly if the market recovers and volatility falls.

VIX Backwardation Trading Strategies

When backwardation is present, VIX futures and long volatility products like VXX and UVXY all gain value over time if the VIX does not fall drastically.

If VIX backwardation is present and traders believe S&P 500 volatility will remain unchanged or increase further, profits can be made from long volatility trading strategies, including:

- Buying VIX futures

- Buying VXX/UVXY shares

- Buying calls on VIX/VXX/UVXY

- Shorting puts on VIX/VXX/UVXY

These strategies can profit from persistently high market volatility, as the VIX futures will remain in backwardation and steadily appreciate as they converge towards the higher VIX spot price.

However, traders should be cautious with long volatility trading strategies when market volatility is already elevated, especially if it is extremely high (VIX over 50).

Extreme market volatility typically does not last long, which is precisely why long-dated VIX futures will trade at steep discounts to spot VIX during periods of significant market volatility.

Conclusion

Understanding contango and backwardation is key when trading VIX options, futures, and popular volatility products like VXX, UVXY, or SVXY.

The most critical concept to understand is that volatility products are tied to VIX futures, which converge to the VIX index over time.

During normal market conditions, contango is typically present in the VIX futures curve, leading to steady bleed in the values of volatility index futures as they drift towards the lower VIX index.

The result is losses in long volatility positions (long futures, long VIX calls/short VIX puts, long VXX/UVXY).

For traders to profit from long volatility positions when contango is present, market volatility needs to increase quickly, pulling the VIX index and futures higher.

Otherwise, traders can take advantage of the “contango bleed” and profit from short volatility positions as long as market volatility does not surge. Of course, shorting volatility is no easy trade.

At a minimum, I hope this post helped you grasp the complexities of the volatility market, helping you avoid common pitfalls and disastrous trading results that stem from a lack of awareness related to VIX trading.

Next Lesson

projectfinance Options Tutorials

About the Author

Chris Butler received his Bachelor’s degree in Finance from DePaul University and has nine years of experience in the financial markets.

Chris started the projectfinance YouTube channel in 2016, which has accumulated over 25 million views from investors globally.