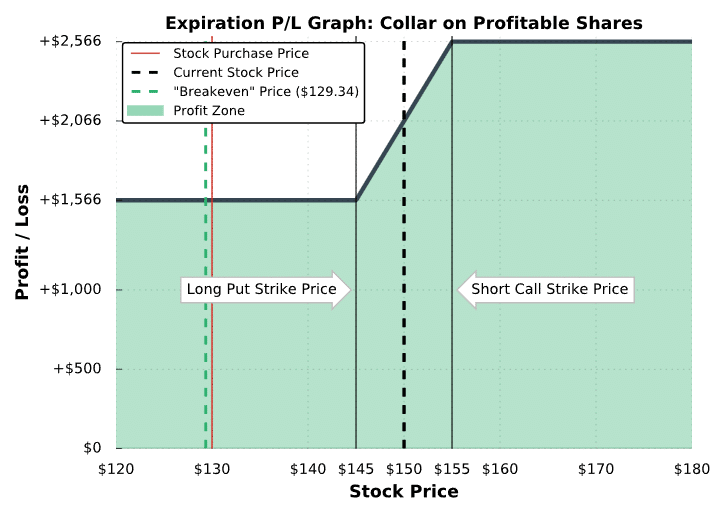

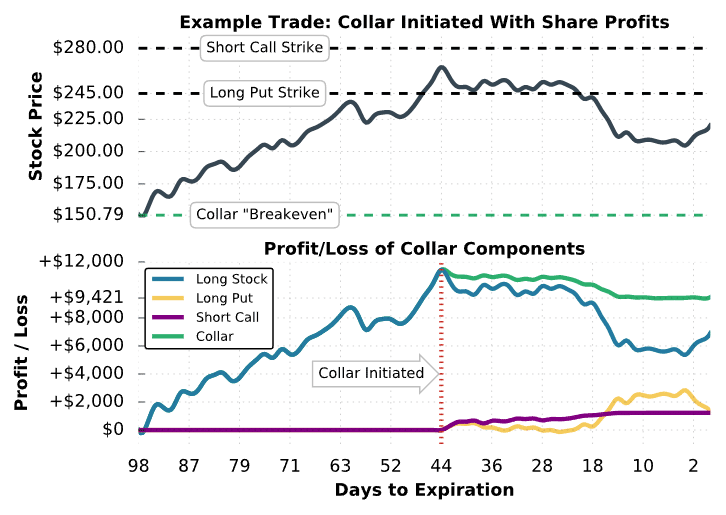

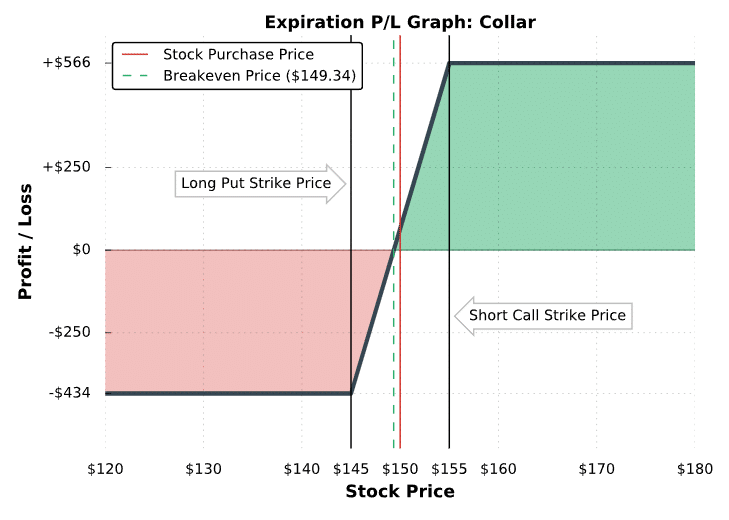

In the final example, we’ll examine how a collar position can be used to protect the profits on a long share position. Here’s the setup:

➥ Initial Share Purchase Price:$151.04

➥ Share Price When Entering Collar: $265.42

➥ Strikes and Expiration: Long 245 put; Short 280 call; Both options expiring in 44 days

➥ Premium Collected for Call: $12.30

➥ Premium Paid for Put:$12.05

➥Net Credit: $12.30 in premium collected – $12.05 in premium paid = $0.25 net credit

➥ Breakeven Price: $151.04 share purchase price – $0.25 collar credit = $150.79

➥ Maximum Profit Potential:

[($280 short call strike – $151.04 share purchase price) + $0.25 collar credit] x 100 = +$12,921

➥ Maximum Loss Potential:*

[($245 long put strike – $151.04 share purchase price) + $0.25 collar credit] x 100 = +$9,421

*In this example, we’ve altered the maximum loss calculation to result in a positive number because this particular position has no loss potential. Using the standard formula from the other examples would give us a negative maximum loss number, which represents a profit. Adjusting the formula was done to avoid confusion.

As we can see from the table above, there is no loss potential on this position because the share purchase price is well below the long put strike. Let’s see what happens over time:

(1)")