In options trading, credit spreads are strategies that are entered for a net credit, which means the options you sell are more expensive than the options you buy (you collect option premium when entering the position).

Credit spreads can be structured with all call options (a call credit spread) or all put options (a put credit spread).

➥Call credit spreads are constructed by selling a call option and buying another call option at a higher strike price (same expiration).

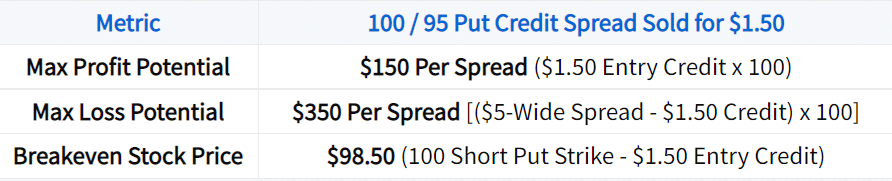

➥Put credit spreads are constructed by selling a put option and buying another put option at a lower strike price (same expiration).

In both cases, the option that is sold will be more expensive than the option that is purchased, which leads to a credit when entering the position.

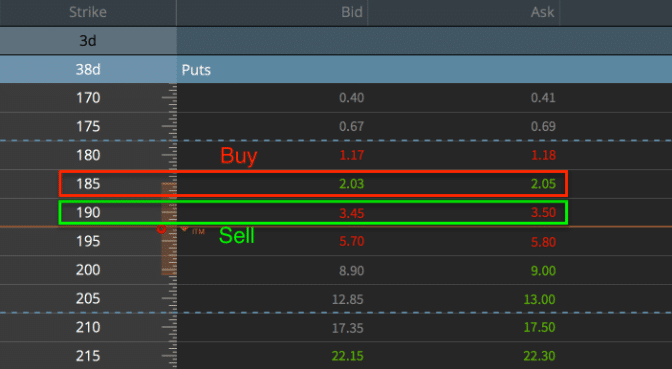

For example, in the image below, selling the 190 put for $3.45 and buying the 185 put for $2.05 would result in a net credit of $1.40 ($3.45 Collected – $2.05 Paid = $1.40 Net Credit):

Software Used: tastyworks Trading Platform

The above trade of selling a put option (shown on a tastyworks options chain) and buying another put option at a lower strike price is an example of a put credit spread, which is a bullish strategy.

Ready to go in-depth?

(1)")

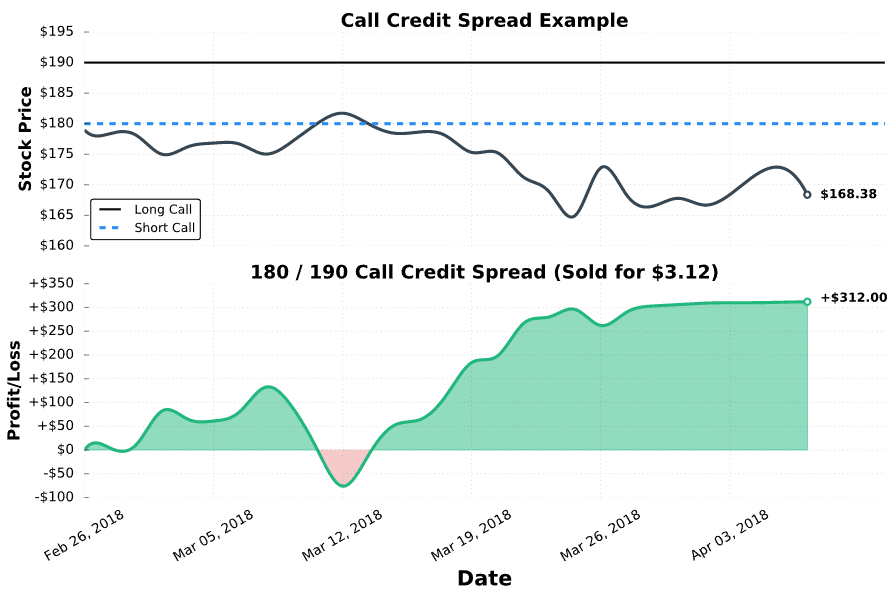

Here’s how the call spread performed relative to the stock price changes:

As we can see, the spread was profitable most of the time, as the stock price remained below the call spread’s strike prices as time went on.

When the stock price remains below the call spread as time passes, the call options steadily lose value because the probability of them expiring in-the-money decreases. It makes sense because there’s less and less time for the stock to rise above their respective strike prices.

As the call options lose value, the spread’s price also decreases, which results in profits for the call credit spread trader.

At expiration, the stock price was at $168.38, well below the call spread strike prices of $180 and $190. Consequently, the spread expired worthless and the overall profit on the trade was $312 per spread: ($3.12 Entry Credit – $0.00 Expiration Price) x 100 = +$312.

If the stock price was above $190 at the time of expiration, the 180/190 call spread would have been worth $10, in which case the loss per spread would have been $688 ($3.12 Entry Credit – $10 Expiration Price) x 100 = -$688.

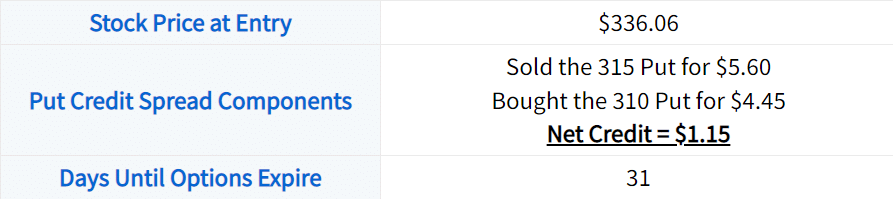

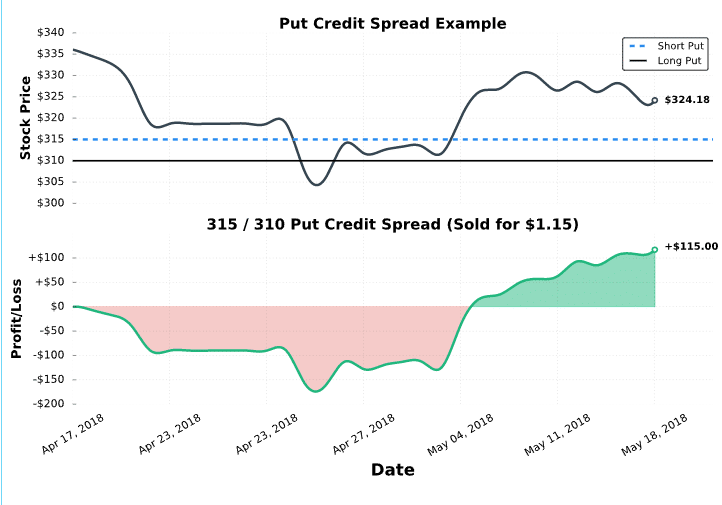

Here’s how the put spread performed relative to the stock price changes:

In this example, the trade was unprofitable for a few weeks after entering the position, as the stock price decreased notably immediately after selling the spread.

When the stock price decreases towards/through the put spread’s strike prices, the put options gain value and the price of the spread increases. When the spread price is more than what the trader initially collected, the position will have losses.

Fortunately, the stock price recovered and was above the put spread’s strike prices at expiration.

At expiration, the stock price was at $324.18, well above the put spread strike prices of $315 and $310. Consequently, the spread expired worthless and the overall profit on the trade was $115 per spread: ($1.15 Entry Credit – $0.00 Expiration Price) x 100 = +$115.

If the stock price was below $310 at the time of expiration, the 315/310 put spread would have been worth $5, in which case the loss per spread would have been $385 ($1.15 Entry Credit – $5 Expiration Price) x 100 = -$385.