(1)")

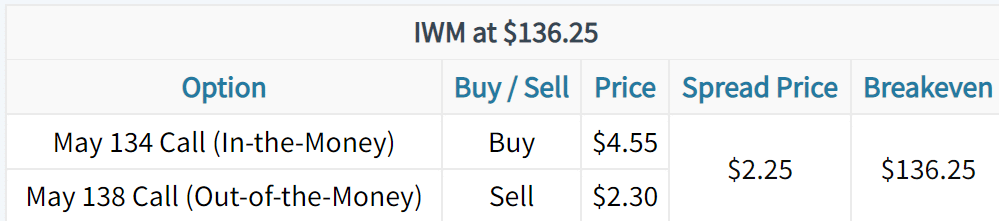

In this case, buying the 134/138 call debit spread with the IWM ETF at $136.28 gives us a breakeven price of $136.25 (Long Call Strike of $134 + Spread Entry Price of $2.25 = $136.25). So, if the stock price remains right at its current level, the call spread will break even, similar to holding the actual stock. Furthermore, the maximum loss potential is $225 ($2.25 x 100) per spread, and the maximum profit potential is $175 [($4 Spread Width – $2.25 Purchase Price) x 100] per spread. For this spread, the margin requirement would be the loss potential of $225, which means the potential return on capital is 78%.

Here’s a visualization of a call debit spread that is structured similarly to the call spread in the table above:

As we can see, the spread’s breakeven price is right near the initial stock price, and the spread doesn’t lose much value when the stock price doesn’t move too much (during the period between 82 to 45 days to expiration). This is because the in-the-money option consists of mostly intrinsic value, which does not decay. Additionally, the short call’s price decay offsets most of the decay of the long option’s extrinsic value.

In short, structuring a debit spread with an in-the-money long option and an out-of-the-money short option minimizes the exposure to losses from time decay. Additionally, the spread’s probability of profit is approximately 50% because the breakeven price is right near the stock price at the time of trade entry.

Selecting Strike Prices for Lower Risk, Higher Return Debit Spreads

The second type of debit spread setup we use is to structure a strategy with asymmetric return potential, but with less risk and a higher probability of profit than simply buying a call or put. The spread is structured by purchasing an at-the-money option and selling an out-of-the-money option against it. This setup will result in less loss potential, more profit potential, and a lower probability of success.

But how do you choose the short strike in the spread? That depends on your outlook for the stock. A logical placement for the short strike is your “best-case” scenario for the stock’s movement. In other words, the furthest you think the stock will move by the spread’s expiration.

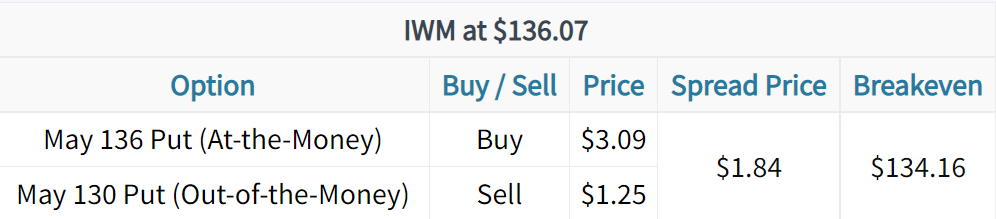

For example, the following spread uses a short strike of 130, which means the trader who buys this debit spread believes $130 is a realistic price target over the time frame of the trade:

As you’ll notice, the breakeven price of this put spread is $134.16, which is $1.91 below the current stock price. Since we need IWM to fall in order to break even at the time of this spread’s expiration date, the spread has a lower probability of profit.

In regards to potential profits and losses, this spread’s price is $1.84, which means the maximum loss potential is $184 ($1.84 x 100) per spread. Since the spread is $6 wide, its maximum potential value is $6, which means the maximum profit potential is $416 ([$6-Wide Spread – $1.84 Purchase Price] x 100) per spread.

Since the margin requirement of this spread is the maximum loss potential of $184, the potential return on capital for this trade is 226% ($416 Profit Potential / $184 Spread Purchase Price). So, by altering our strikes to structure a more directional trade with better return potential and less loss potential, the potential return on capital increased in comparison to the previous spread. However, with more return potential and less loss potential, the probability of making money on the spread decreases.

Here’s an example of a put debit spread structured similarly to the put spread from above: