(1)")

What is “Rolling?”

In options trading, “rolling” refers to closing an existing option position and opening a similar option position with different strike prices, in a different expiration cycle, or a combination of the two.

Today, we’ll focus on “rolling down” the short call spread in a short iron condor position, which refers to buying back your current call spread and “rolling it down” by selling a new call spread at lower strike prices.

Rolling an Option

The process of closing an existing option and opening a similar option position at different strike prices, in a different expiration cycle, or a combination of the two.

When Do You Roll Down the Short Call Spread?

When trading iron condors, the most typical time to roll down the short call spread is when the stock price falls quickly towards your bull put spread.

Consider the following visual:

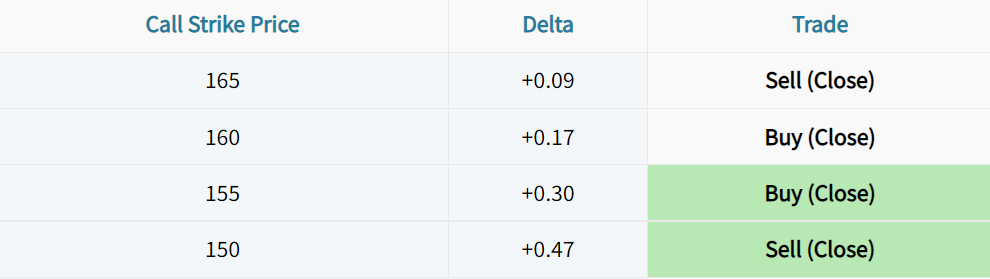

Typically, a short iron condor position will start with no directional risk exposure (position delta is near zero). However, when the stock price falls quickly towards the short put’s strike price, the position’s delta will grow positive, which means the trade has become directionally bullish.

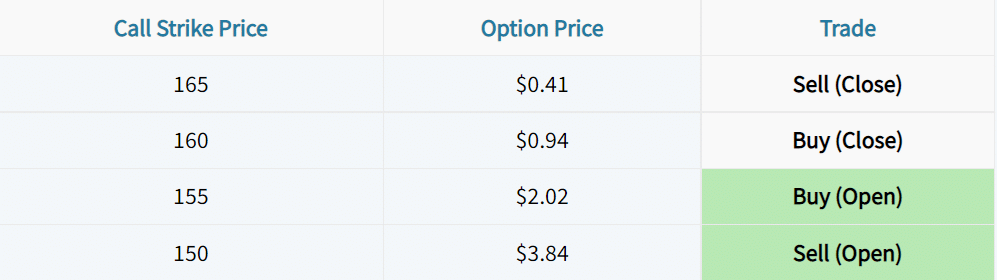

The most common iron condor adjustment to make in this scenario is to roll down the short call spread by purchasing the old call spread (closing trade), and selling a new call spread at lower strike prices (opening trade):

When adjusting an iron condor by rolling down the short call spread, what does the trader accomplish?