(1)")

Implied volatility rank (IV rank) compares a stock’s current IV to its IV range over a certain time period (typically one year).

Here’s the formula for one-year IV rank:

For example, the IV rank for a 20% IV stock with a one-year IV range between 15% and 35% would be:

An IV rank of 25% means that the difference between the current IV and the low IV is only 25% of the entire IV range over the past year, which means the current IV is closer to the low end of historical volatility.

Furthermore, an IV rank of 0% indicates that the current IV is the very bottom of the one-year range, and an IV rank of 100% indicates that the current IV is at the top of the one-year range.

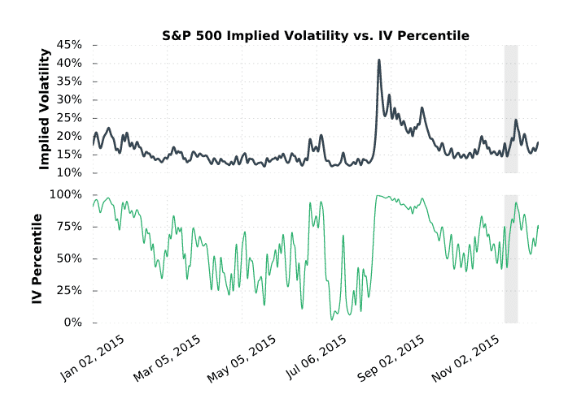

Implied volatility percentile (IV percentile) tells you the percentage of days in the past that a stock’s IV was lower than its current IV.

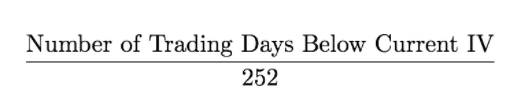

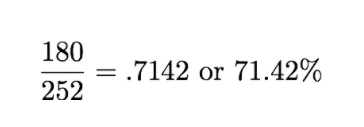

Here’s the formula for calculating a one-year IV percentile:

As an example, let’s say a stock’s current IV is 35%, and in 180 of the past 252 days, the stock’s IV has been below 35%. In this case, the stock’s 35% implied volatility represents an IV percentile equal to:

An IV percentile of 71.42% tells us that the stock’s IV has been below 35% approximately 71% of the time over the past year.