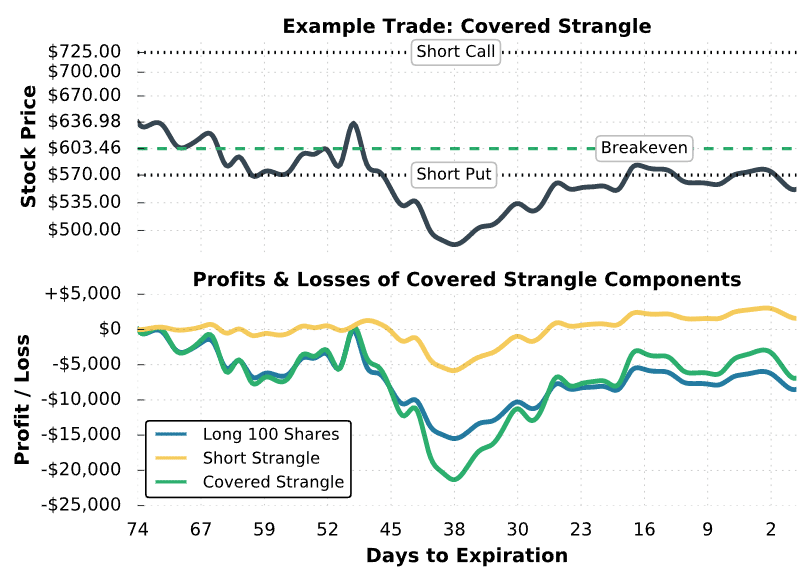

In the final example, we’ll look at a covered strangle trade that suffers significant losses due to a decrease in the stock price. Here’s the setup:

Initial Share Purchase Price: $636.98

Strangle Strikes and Expiration: Short 725 Call; Short 570 Put; Both options expiring in 74 days

Premium Collected for Strangle: $19.60 for the call + $13.92 for the put = $33.52

Breakeven Price: $636.98 share purchase price – $33.52 strangle credit = $603.46

Maximum Profit Potential: ($725 short call strike – $603.46) x 100 = $12,154

Maximum Loss Potential: [(570 Short Put Strike – $33.52 Strangle Credit) + $636.98 Share Purchase Price] x 100 = $117,346 (stock price at $0)

Let’s see what happens!

(1)")