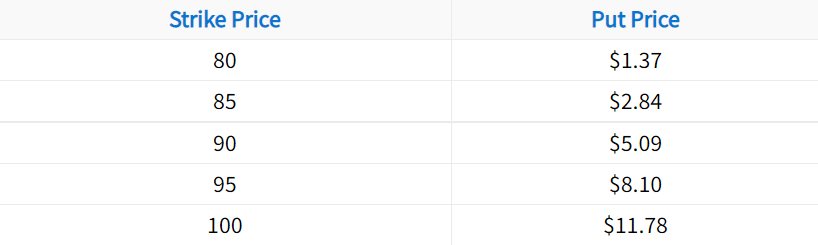

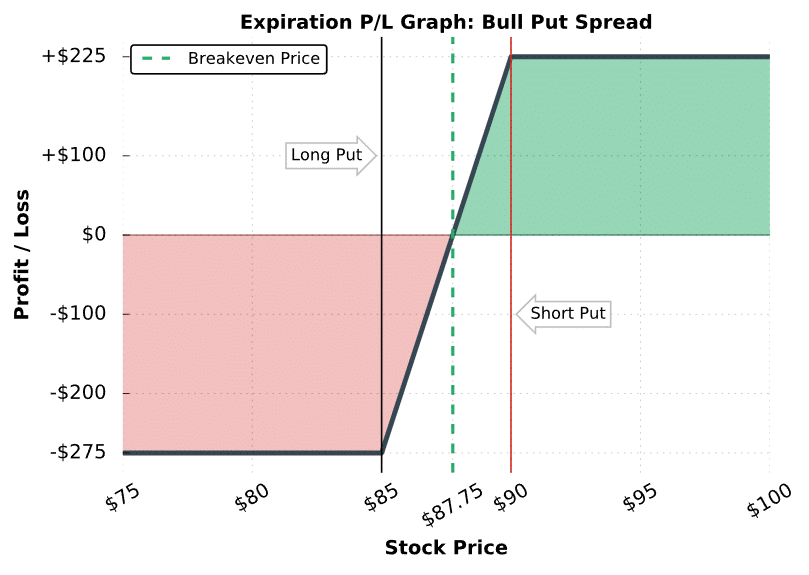

Stock Price Above the Short Put Strike ($90):

Both the 85 and 90 put expire worthless. The profit on the short 90 put is $509, but the loss on the long 85 put is $284, resulting in a net profit of $225.

Stock Price Between the Short Put Strike ($90) and the Bull Put Spread’s Breakeven Price ($87.75):

The short 90 put expires with intrinsic value, but not more than the $2.25 credit received for the short put spread. Because of this, the bull put spread trader realizes a profit, but not the maximum profit since the position expires with some value.

Stock Price Between the Bull Put Spread’s Breakeven Price ($87.75) and the Long Put Strike ($85):

The short 90 put expires with more intrinsic value than the $2.25 credit the put spread trader collected when selling the spread. Because of this, the trader realizes a loss at expiration, but not the maximum loss.

Stock Price Below the Long Put Strike ($85):

The value of the $5-wide short put spread is $5. Since the spread was sold for $2.25, the trader realizes the maximum loss of $275.

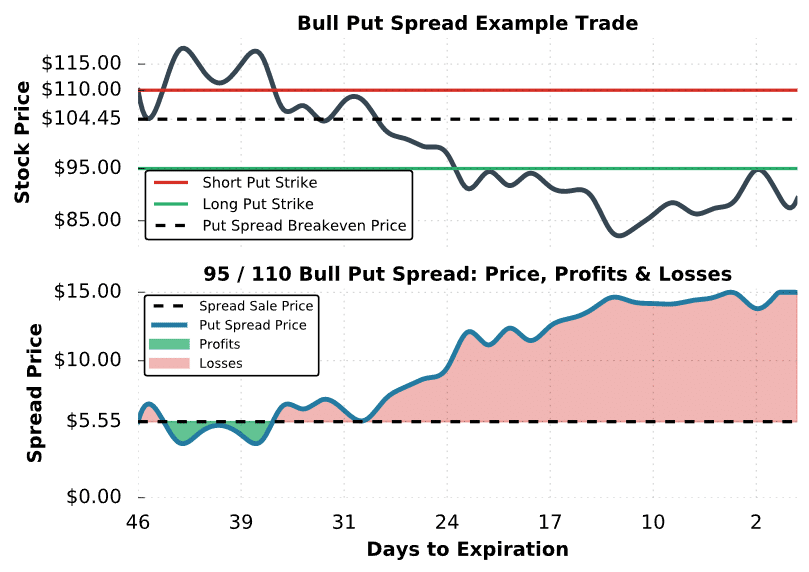

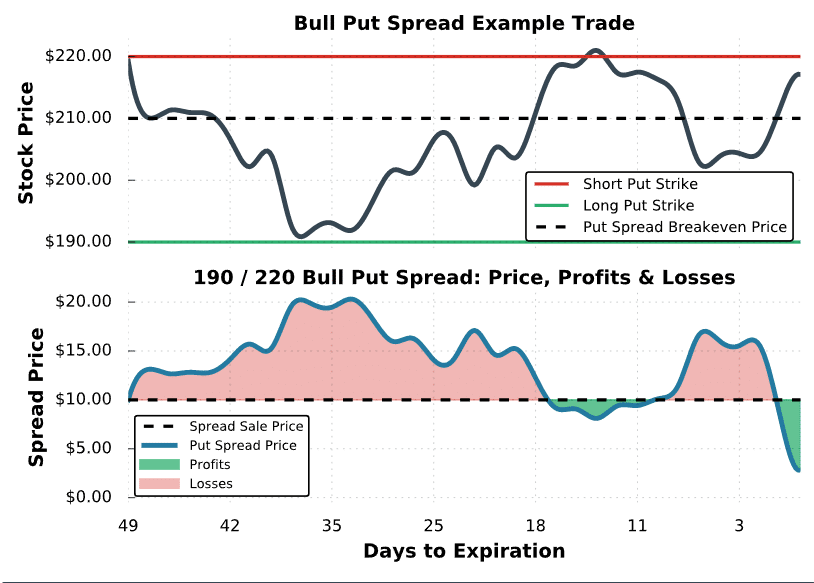

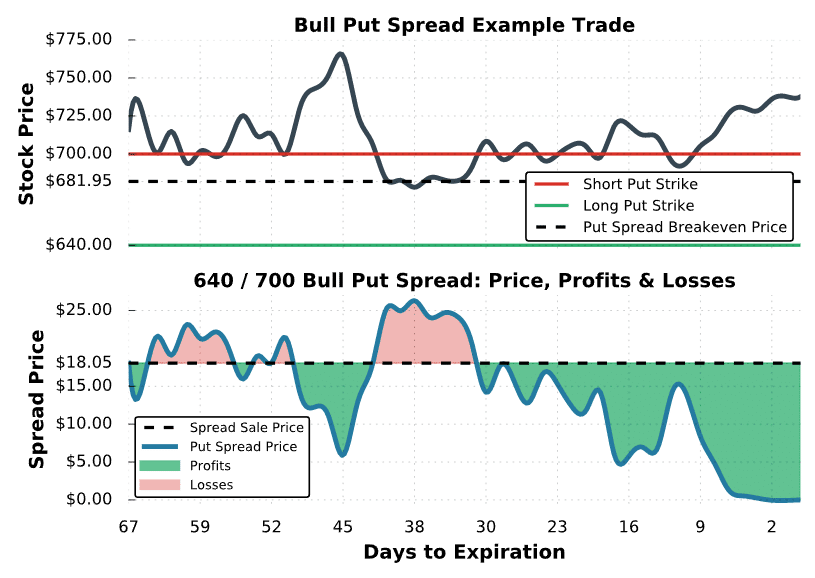

Nice! You know how to determine the potential outcomes of a short put spread at expiration, but what about before expiration? To demonstrate how short put spreads perform before expiration, we’re going to look at a few examples of positions that recently traded in the market.

(1)")