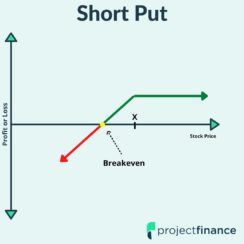

Options Trading Short Put Option Payoff Results from 41,600 Trades [Study] Read More » February 10, 2022

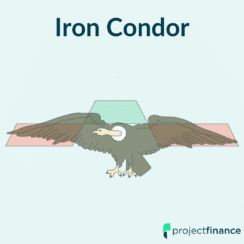

Options Trading Iron Condor Options Strategy Explained | Trade Examples & Stats Read More » February 10, 2022